U.S. Stocks Likely To Lose 50% Versus Treasuries (SPX)

24K-Production

Bonds outperforming US stocks over the coming years is one of my strongest conviction calls to date, with the SPX likely to lose 50% relative to 10-year US Treasuries. This may be difficult to imagine for most investors who believe that any decline in bond yields would cause stocks to rise, or that any decline in stocks would have to result from further declines in bond prices. However, we are highly likely to see simultaneous SPX weakness and UST strength over the coming years as the economic cycle turns.

Stocks have dramatically outperformed bonds over recent years and decades, and over the very long term we will almost certainly see stocks outperform. The reason being that stock prices tend to grow at the pace of nominal GDP growth over the long term, which tends to be in line with the yield on USTs, but investors also receive a dividend yield from stocks. Over the long term, the SPX has outperformed USTs by almost exactly its average dividend yield.

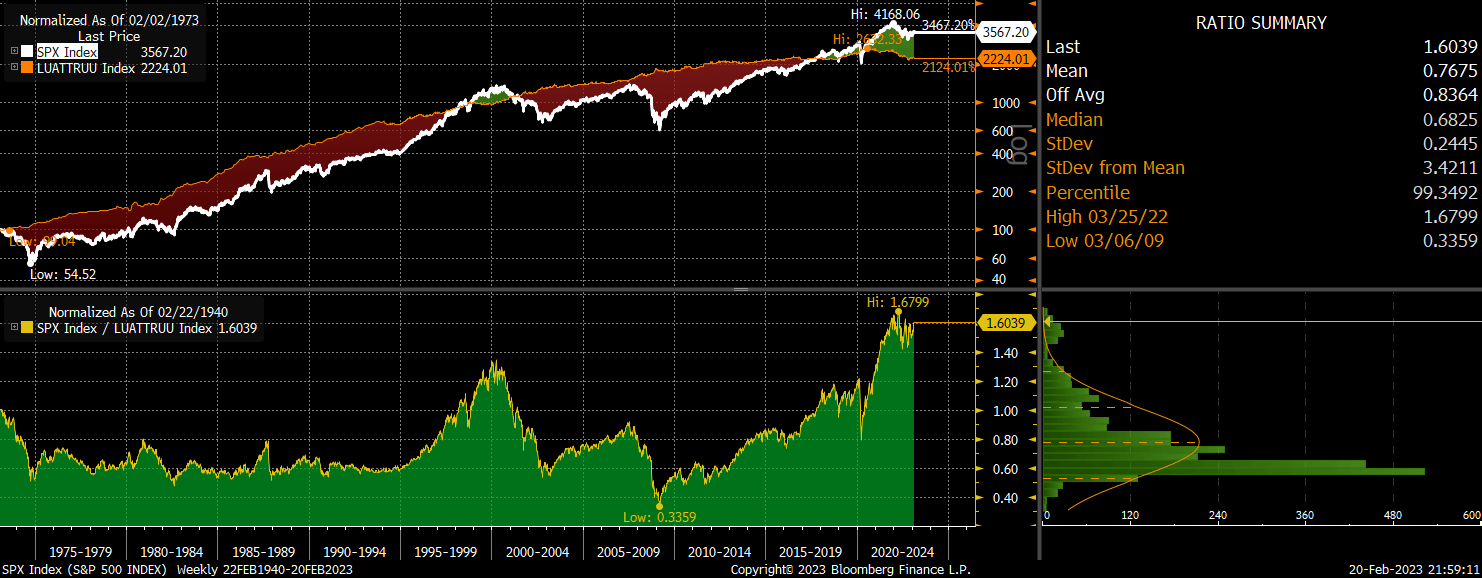

However, the coming years are likely to see significant underperformance. The following chart shows the SPX price relative to the total return performance of US 10-year Treasuries. I have compared the total return on bonds to the price return of the SPX because over time the performance of the two should converge together in line with nominal GDP.

SPX Price Vs Total Return 10-Year UST (Bloomberg)

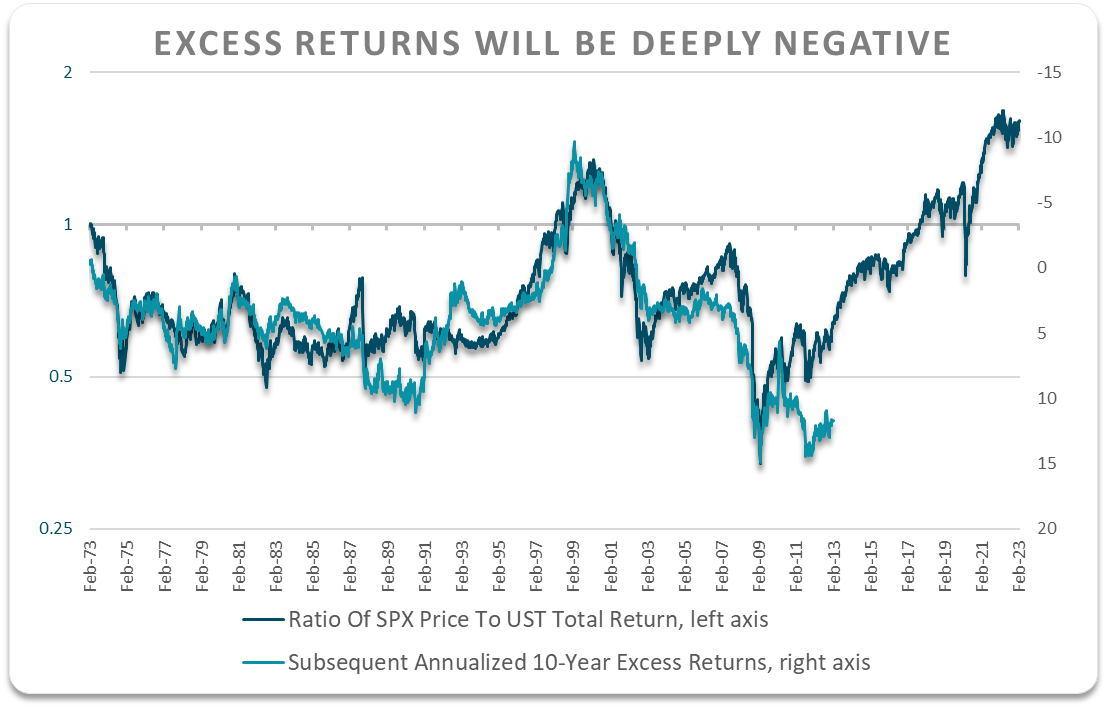

Of course, there have been long periods when stocks have outperformed, which have resulted from excessive optimism about future growth, which caused equity valuations to rise alongside falling bond prices. When optimism fades, stocks tend to underperform as valuations decline while bond prices move higher. Over the past 50 years the ratio has always reverted back to its average. The chart below shows the ratio of the SPX relative to 10-year USTs versus subsequent 10-year total excess SPX returns, which is extremely closely correlated as the theory would suggest. The current ratio is consistent with future annual returns of -10% over the next decade.

Bloomberg, Author’s calculation

This should come as no surprise as it happened twice in just over 20 years. The first such case of SPX underperformance came following the high UST yield and record equity valuations of the late-1990s. Over the three years following the 2000 peak, the SPX lost 58% of its value relative to 10-year USTs, even when reinvested dividends are taken into account. Another episode occurred from 2007-2009 when the SPX lost 61% in relative terms. On both occasions, not only did stocks fall but bonds moved significantly higher.

Current conditions are almost as attractive as they were at these two previous major equity peaks. While the yield differential between USTs and the SPX is not quite as extreme as it was in 2000 or 2007, the outlook for long-term GDP growth is also weaker than it was in those periods. Nominal GDP growth averaged 4% in the decades that followed those market peaks and based on 10-year breakeven inflation expectations of just 2.4%, real GDP growth would have to come in at 1.6% for nominal GDP to maintain its long-term pace. As I have written about many times over the past few years, real GDP is likely to average a full percentage point lower than this even in the absence of a deep recession.

For a moment let’s assume that over the next decade the SPX and USTs are expected to deliver returns in line with their long-term average. This would mean the SPX should return 5.6% (a 1.6% dividend yield growing at the pace of 4% nominal GDP), while USTs should return 4%. If it becomes clear that nominal GDP growth is likely to be 1pp lower than it has been in the past, this would cause a huge decline in the SPX and rally in USTs. In order for SPX return expectations to stay at 5.6%, the dividend yield would have to rise to 2.6%, resulting in a ~40% price decline. Meanwhile, 10-year bond prices would surge, easily causing a 50% relative decline in the SPX.