TTEC Holdings: Undervalued Despite No Significant Change In Business Fundamentals

Editor’s note: Seeking Alpha is proud to welcome Bee Spoke Investing as a new contributor. It’s easy to become a Seeking Alpha contributor and earn money for your best investment ideas. Active contributors also get free access to SA Premium. Click here to find out more »

SrdjanPav/E+ via Getty Images

Summary

YTD price action has driven TTEC Holdings (NASDAQ:TTEC) into a compelling buy opportunity. The stock has largely sold off since its 2021 COVID peak in the low $100s due to the broader tech selloff, but hasn’t enjoyed any of the gains that the mega cap tech names have benefited from in 2023. I consider TTEC to be undervalued despite no significant change in business fundamentals. Multiples are depressed from historical averages, which is unwarranted in my opinion. Further, I consider TTEC is currently positioned to do well in the coming years based on a focus on improving margins. TTEC possesses a promising business model that will benefit from advances in technology in a growing sector.

Business Overview

TTEC is a customer experience technology and services company that helps companies manage the customer experience. They offer a wide range of services, including customer care, tech support, sales, AI operations, and trust and safety. TTEC has a global presence with over 60,000 employees in over 25 countries.

TTEC operates under 2 reported segments, TTEC Digital and TTEC Engage. Here’s how the company describes these segments in its 10-K for 2022:

TTEC Digital is one of the largest pure-play CX technology service providers with expertise in CX strategy, digitization, analytics, process optimization, system integration, cloud-based technology solutions, and transformation enabled by our proprietary CX applications and technology partnerships. TTEC Digital designs, builds, and operates robust digital experiences for clients and their customers through the contextual integration and orchestration of customer relationship management (“CRM”), data, analytics, CXaaS technology, and intelligent automation to ensure high-quality, scalable CX outcomes.

TTEC Engage provides the digitally enabled CX managed services to support our clients’ end-to-end customer interaction delivery at scale. The segment delivers omnichannel customer care, technology support, order fulfillment, customer acquisition, growth, and retention services with industry specialization and distinctive CX capabilities for hypergrowth brands. TTEC Engage also delivers digitally enabled back office and industry specific specialty services including artificial intelligence (“AI”) operations, and fraud management services.

In short, the way to think about them is that these two segments are essentially both sides of the same coin. TTEC Engage provides the resources to handle phone-based transactions such as account queries, order fulfillment, and other activities. Similarly, TTEC Digital is more or less the same but is focused on the digital aspects of client experience – instead of call centers, think chatbots and self-service sections of websites, as well as a suite of consulting services. TTEC’s clients include some very large corporations across a diverse set of industries, including AT&T (T) and Bank of America (BAC) to name a few. Chances are you’ve interacted with a TTEC employee for assistance with a financial services product, video streaming, connected fitness equipment or roadside assistance, to name a few examples.

A Typical Call Center Layout (Orlando Business Journal)

Revenue and Earnings Profile

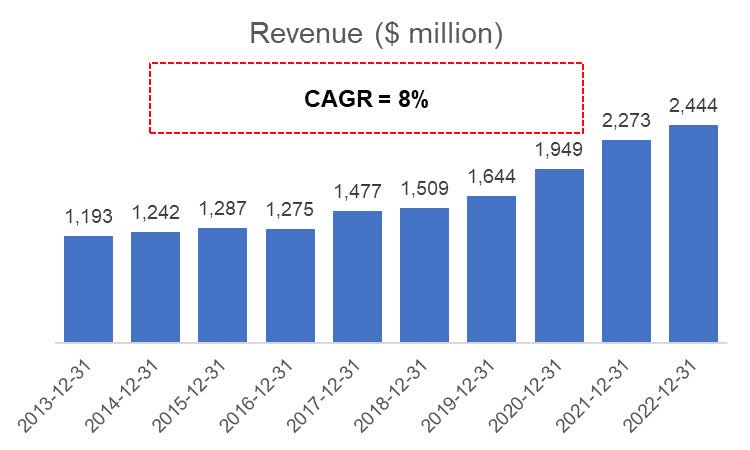

Revenues have been growing at a healthy clip over the past decade at a ~8% CAGR. Margins have historically been more volatile, with operating margin benefitting from the COVID pandemic in 2020-21, before dropping back to its normal run rate in the mid-single digits in 2022. Share count has remained fairly stable in recent years at ~47 million. My model predicts a slight uptick in diluted share counts due to incentive compensation. All in all, the trending run rate of incentive comp driven dilution is expected to continue, which isn’t a material impact in my view.

Annual TTEC Revenues (Finbox)

Op Income & Margin (Finbox)

Diluted Shares (Finbox)

1Q23 Earnings Takeaways

The company has demonstrated continued top-line revenue strength on top of strong demand. Its revenue pipe remains strong. Ken Tuchman, Chairman and CEO, stated the following during the 1Q23 earnings call.

Demand for our solutions remain strong as CX executives are caught in a balancing act between the efficiencies of digitization and the empathy of human conversations.

AI, which has been an overhyped buzzword as of 1Q23 conference calls, has been manifesting itself more into product offerings. I don’t see AI in and of itself driving massive growth in TTEC in my forecast, but it doesn’t seem to hurt since the impetus to apply this kind of technology is and will manifest itself on a broader scale. Mr. Tuchman made the following observations about AI at the earnings discussion.

We have many examples of solutions that are delivering high-value outcomes leveraging AI, including using the analytics to simplify and personalize customer journeys, bots to facilitate training, automation to augment associate efficiency and predictive models to support intelligent routing. Also, across verticals, we’re customizing these solutions to address industry-specific business challenges.

One key tailwind is the shifting of resources to lower-cost geographies, notably to India and the Philippines. Shelly Swanback, CEO, TTEC Engage and President, TTEC stated the following at the results call.

To meet demand and strengthen our profit margins, we continue to expand our cost to optimize global delivery model. This quarter, we opened our new flagship engineering center in Hyderabad, India. By midyear, 1/3 of our engineering talent will be operating out of tech hubs in India and the Philippines with more locations to come in the near future.

Financial Statements – Notable Items

TTEC tends to keep a large amount of cash on its balance, which I view as a positive. Although not the most productive assets from a growth perspective, I believe this can be opportunistically deployed to pay off high-cost debt and bolsters stability to continue paying a dividend.

Trending goodwill “up and to the right” point to the TTEC’s activeness in the M&A space. TTEC has been actively acquiring companies in recent years in an effort to expand its customer experience services portfolio and reach new markets. The company’s most recent acquisition was Faneuil, a provider of public sector citizen engagement solutions. The acquisition will allow TTEC to expand its CX services to the public sector market. I don’t view this particularly as a negative as long as it translates to profitable growth and not growth at all costs.

Here are some excerpts of Mr. Tuchman’s statements made during the earnings presentation.

M&A must ultimately create tangible value for our clients. We remain committed to M&A that helps differentiate our solutions for clients and accelerate the execution of our business strategy. Our M&A strategy will continue to be focused on both Digital and Engage acquisitions to help accelerate vertical solutions through incremental capabilities, new geographies and additional clients. In closing, I’d like to reiterate my confidence in our business. Our management team is executing. Our clients continue to rely on us as a strategic partner. Our CX engineers are developing new and relevant solutions for the market, and our frontline teams are delivering exceptional CSAT scores across the globe.

And so what I would just say to you is that although M&A is something that is absolutely going to continue to be part of our strategy, our future strategy, we think that it’s prudent for us to wait a little bit and try to see where the valuations come in on some of the targets that we’re looking at. I think that any of the M&A that we would be doing would be much more geared towards the strategic side in areas that would be benefiting more of the Digital business. But what I would just simply say to you is that we’re going to — right now, our team is very focused on execution and on organic growth.

One other pertinent detail is the amount of revenue concentration noted in recent 10Ks/Qs to an “automotive company” and a “financial services firm”, who I presume to be General Motors (GM) and Bank of America. The estimated revenue from these two clients alone is somewhere just north of 20% of consolidated revenues. Here is another excerpt from the 10-K of 2022 cited in the Business Overview section above.

The Company had one client that contributed in excess of 10% of total revenue for each of the years ended December 31, 2022, 2021 and 2020. The 2022 client operates in the automotive industry and is included in the Engage segment.

A Nice Dividend That’s Expected To Continue Paying Out

Based on 1Q23 cash levels and a run rate of ~$25 million, TTEC can afford to continue paying the dividend if the entire company decides to stop and twiddle its thumbs all day. I don’t see any material risks to the dividend being cut and the current yield at ~3-4% is fairly attractive for a name that has a solid lineup of revenue generation in the pipeline, potential for additional operating margin expansion and tech driven growth prospects.

Valuation

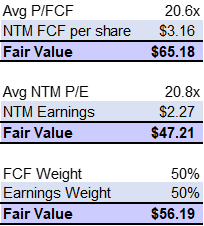

To value TTEC, I use a blended approach based on NTM earnings and NTM FCF. I typically opt to use a combination of approaches to root out any bias that may have crept up into my financial model. Overall, I think it’s the prudent thing to do to make sure that the stock’s target price isn’t extremely untethered from a reasonable valuation multiple.

TTEC is trading at ~16.6x P/E and ~16.1 x P/FCF based on trailing multiples at the time of this writing, slightly under historical averages, which gives us some additional cushion on the downside. I believe multiples will expand to their historical multiples once FY23 earnings continues to play out in TTEC’s favor. It can be argued that valuation multiples have come down across the board, and that many investors may scoff at multiples that were afforded to stocks when interest rates were lower and there were no recession fears. However, keep in mind that TTEC is trading closer to its 52-week low, while broad-based indices such as the S&P 500 and NASDAQ 100 keep grinding higher. I don’t believe this is sustainable when the yield curve is negative sloping and consumer spend starts to fade. Value is where I’d like to be positioned currently, which is how I view TTEC – a good value.

As shown below, the NTM P/FCF and P/E are averages calculated over the timeframe from 1Q19 through 1Q23.

TTEC Valuation (TIKR, Author Estimates)

I believe multiple expansion closer towards the historical average combined with continued top line growth are the catalysts to consider here. This holds even if margins don’t improve, which I assume as the base case scenario within my financial model.

Estimates vs. Consensus

My revenue estimates for FY23 and FY24 are in line with consensus. Where I diverge from the Street is everything below the top line. I’m typically conservative with my margin improvements unless management indicates they’re closer to the upper end of their guide (will keep an eye out). Despite this, the upside is clear and TTEC is undervalued based on what the fundamentals suggest.

Below is a comparison comparing my top- and bottom-line forecasts vs. Street, as well as some of the baseline assumptions used in my financial model.

Bee Spoke Ests vs. Street (TIKR, Author Ests)

TTEC Model Assumptions (TIKR, Author Estimates)

Catalysts/Risks

Some of the broader risks specific to TTEC include a poorly executed acquisition driving down franchise value, which I don’t believe is material based on TTEC’s track record, and FX risk given the broad geographic footprint of clients. A broad US driven or global economic slowdown is the most apparent risk. However, TTEC’s client base across multiple verticals should prove resilient, as there is no outsized exposure to very cyclical sectors. Finally, the revenue concentration noted in a review of financial statements could cause significant revenue declines if a portion or all of the contracts with these large clients are not renewed. It will take some time, but management is executing its M&A strategy, which will further diversify the company’s revenue streams.

Summary

To reiterate my investment thesis, I view TTEC as an undervalued investment based on extreme negative sentiment, an attractive price point relative to historical multiples and my conservative modeling estimates, as well as tailwinds shifting towards customer retention from a broader economic slowdown. Should TTEC approach mid $50s in terms of its share price, I would consider selling at those levels in order to find other undervalued opportunities.