Snapchat Gets Snapped: Fortune Favors The Brave (NYSE:SNAP)

Steve Jennings/Getty Images Entertainment

Snap (NYSE:SNAP) has been snapped. In 2021, I remember thinking to myself: why didn’t I buy SNAP in 2019 when pessimism was at its peak? The stock would have returned over 10x over that time period. After the post-earnings plunge, we are getting that opportunity yet again. The fundamentals are showing that advertisers have proven quick to reduce spending on SNAP’s platform amidst a weakening economy. Even with growth coming to a standstill and GAAP profitability still nowhere in sight, the stock is trading at distressed valuations. With plenty of cash on the balance sheet to buy valuable time, the stock is highly buyable here.

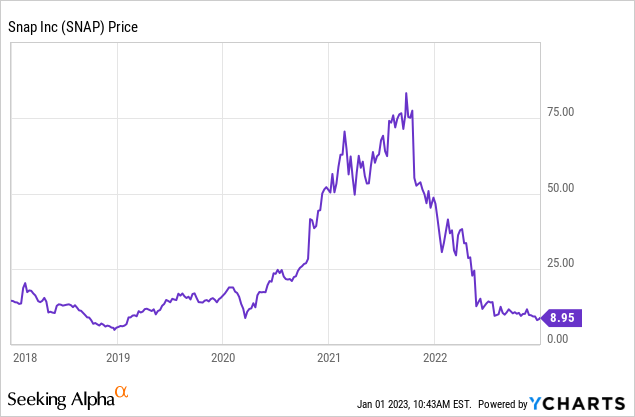

SNAP Stock Price

It wasn’t too long ago that SNAP had become a sizable social media company. The stock has nosedived over the past year.

I last covered SNAP in June and the stock has crashed around 30% since then. Even at these lower valuations, investors should continue to expect high volatility.

SNAP Stock Key Metrics

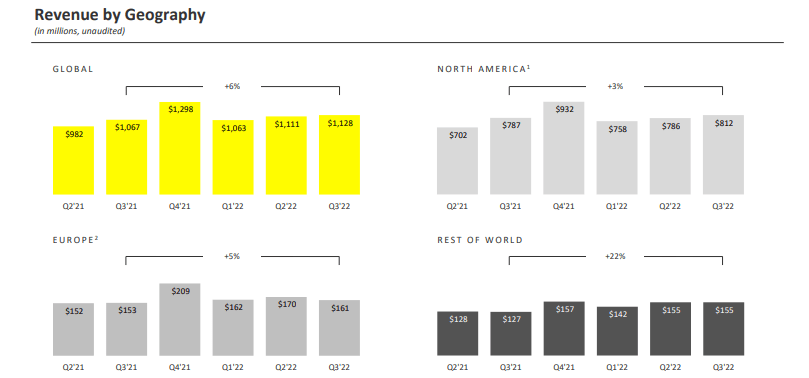

SNAP has previously guided towards minimal growth and that proved to be the case, with revenues growing by only 6%. The strong 22% growth in “rest of world” was not nearly enough to offset the growth slowdown in North America and Europe.

2022 Q3 Presentation

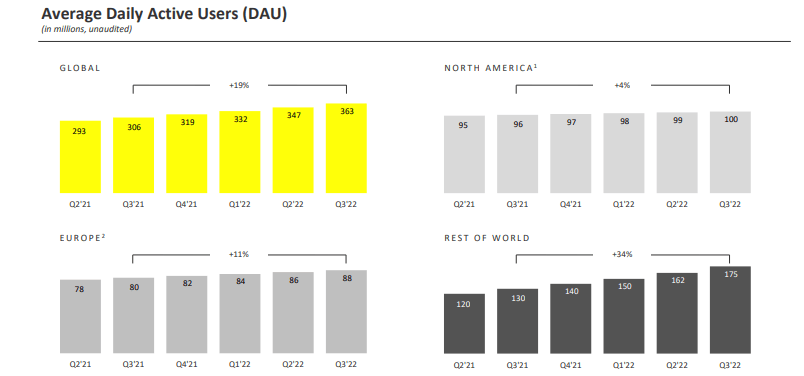

A lone (but important) bright spot was the 19% growth in daily active users (‘DAUs’). Snapchat continues to resonate with its demographic base. Strength in DAUs growth is a core reason why I remain bullish.

2022 Q3 Presentation

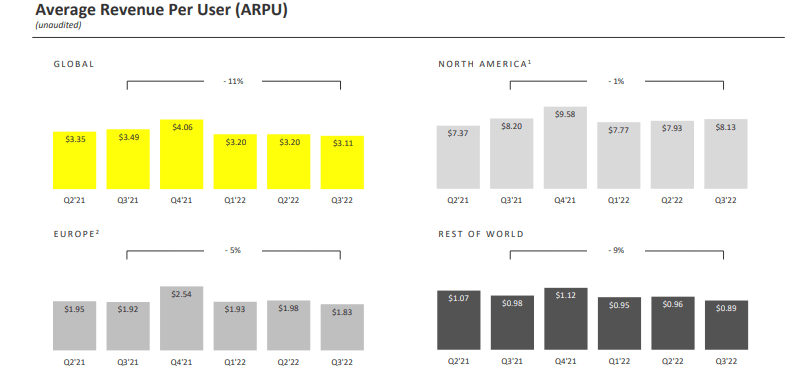

A growth slowdown is one thing, but the decline in average revenue per user (‘ARPU’) may have been the last straw for many. In spite of having a low ARPU, SNAP saw ARPU decline 11% YOY. Rest of World led those declines with a 9% decline – perhaps that explains why revenue growth was strong there.

2022 Q3 Presentation

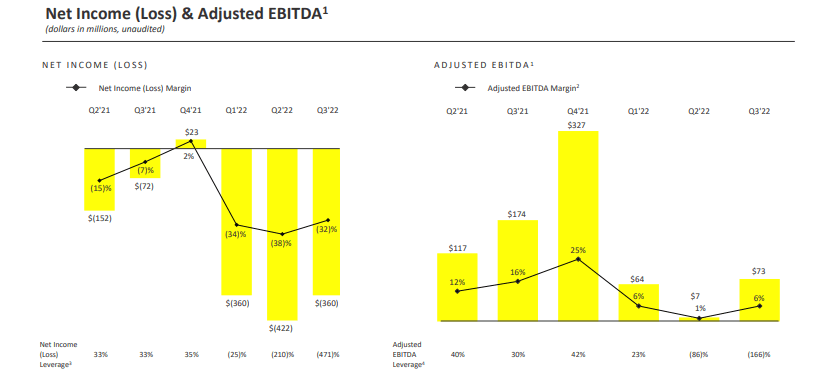

SNAP is still not profitable on a GAAP basis and saw adjusted EBITDA margins contract sharply.

2022 Q3 Presentation

The company did complete its $500 million share repurchase program and announced a new $500 million program. That was enough to make a dent in shares outstanding even inclusive of ongoing share-based compensation.

2022 Q3 Presentation

SNAP ended the quarter with $4.4 billion of cash versus $3.7 billion of debt.

The pain is not expected to end soon. Management did not provide guidance for the fourth quarter but on the conference call noted that growth was around 9% thus far and expected to end up flat.

Management noted:

Even flattish year-over-year revenue growth is about a 15% step-up on a quarter-over-quarter basis. So, we are expecting revenue to grow seasonally at a pretty good clip. So, the issue that we’re seeing here is that if you look back to a year ago, we grew at over 40% year-over-year in the prior year. And many of the really significant macro impacts that we’ve seen over the course of this year weren’t impacting the business nearly as much as they were a year ago.

Is SNAP Stock A Buy, Sell, or Hold?

In this pessimistic environment, it is worth reminding ourselves of the original thesis. SNAP remains a niche social networking company reaching over 70% of 13 to 34 year-olds.

2022 Q3 Presentation

This isn’t just a silly video company anymore (at least that’s how I thought about it before). SNAP has made great strides in augmented reality, and many users now use the app to assist in AR shopping.

2022 Q3 Presentation

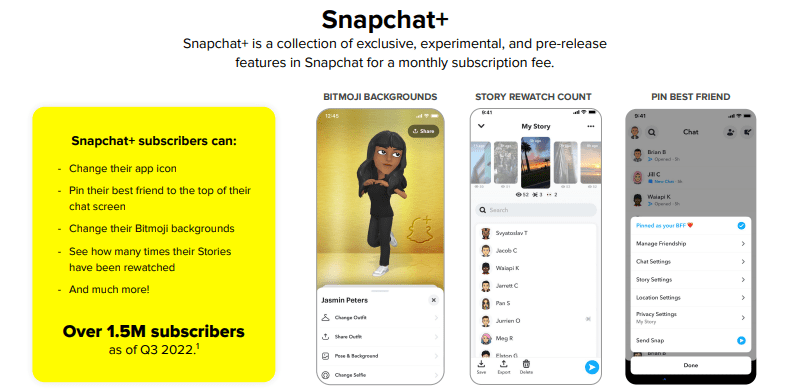

SNAP has also unveiled a premium subscription offering with over 1.5 million subscribers.

2022 Q3 Presentation

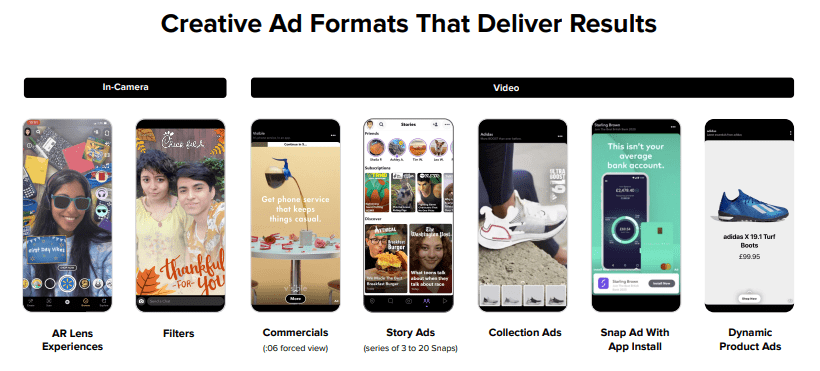

SNAP has expanded its ad format offerings – important considering that it was only servers years ago that investors questioned if advertisements were possible in the first place.

2022 Q3 Presentation

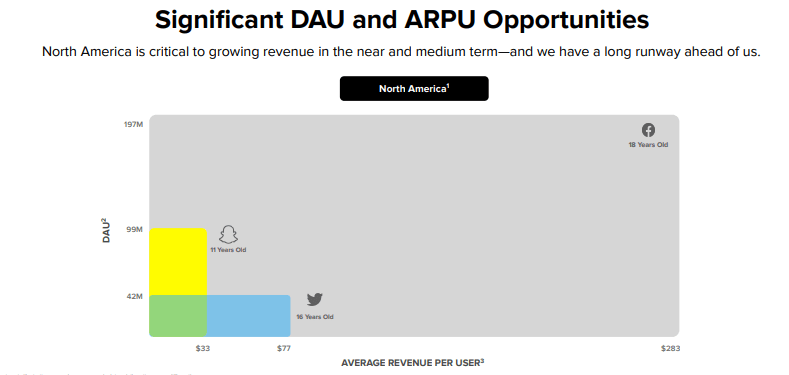

While ARPU did decline in the latest quarter, the long term thesis remains the potential for SNAP to catch up to the ARPU seen at larger peers.

2022 Q3 Presentation

How is management reacting to the difficult climate?

So, we made the decision to reprioritize and focus our investments on our three strategic priorities: growing our community and their engagement; reaccelerating and diversifying our revenue; and investing in augmented reality. And these changes should allow us to drive continued growth in our community while delivering free cash flow even with low levels of revenue growth.

I don’t expect the stock to get out of this rut until management delivers on promises for accelerating revenue growth. Consensus estimates are quite pessimistic – while they incorporate a rebound in growth, the projections fall short of the 40%-60% growth of just several quarters ago.

Seeking Alpha

Yet with the stock trading just around 3x sales, there’s enough upside potential to warrant a bullish stance. If growth returns to even the 20% range, then I could see the stock delivering tremendous returns. Based on a 1.5x price to earnings growth ratio and 30% long term net margin assumption, I could see the stock trading at around 9x sales, implying nearly 200% upside. Given that DAUs continue to grow rapidly, a true recovery may end up being in excess of 20% and offering even more potential upside.

It is worth noting that co-founders Evan Spiegel and Robert Murphy still own sizable stakes in the business.

2022 DEF14A

CEO Spiegel does get not paid a salary by the company but does receive over $3 million in security costs which is placed under “other compensation” as seen below. I am unsure what it is about social networking CEOs needing so much security but I digress.

2022 DEF14A

The risks are numerous. Intuition states that it’s easier to count on decelerating growth than accelerating growth. The valuation is not too demanding even at a low 10% top-line growth rate, but that kind of growth won’t be enough to drive the operating leverage needed to work towards GAAP profitability. It isn’t just a weak economy that’s pressuring the stock. SNAP faces competition from close competitor TikTok as well as the giant in the room Meta Platforms (META). It still isn’t clear if SNAP will recover from the iOS data privacy changes which negatively impacted perceived advertiser ROI on the platform. I view these risks as being priced in, but they cannot be ignored. I have discussed with Best of Breed Growth Stocks subscribers that a diversified basket of beaten-down tech stocks can perform strongly from here. SNAP fits right in with such a basket as a high risk – high reward play.