QID And SQQQ ETFs: Possible Gains, But Rather Muted, Beware Of The Risks (NYSEARCA:QID)

naphtalina/iStock via Getty Images

The fight against inflation is proving to be less challenging than initially expected, as per the latest FOMC Meeting statement on Wednesday, February 1. Well, this is the message that investors seemed to be weighing more than the words of caution of the U.S. Federal Reserve’s Chairman about the possibility of interest rates continuing to be raised.

Even, before that, investors have been bullish on tech stocks, as seen by the one-month performance of the Invesco QQQ Trust (NASDAQ:QQQ) which has appreciated by nearly 17% (deep blue chart below). Conversely, the ProShares UltraPro Short QQQ ETF (NASDAQ:SQQQ) and the ProShares UltraShort QQQ ETF (NYSEARCA:QID) have suffered by 39% and 27.5%, respectively.

Therefore, all those who have been shorting tech through these two exchange-traded funds (“ETFs”) have been crushed, and as this thesis will show, this is likely to be the case in 2023 despite monetary conditions being tightened at such a frantic pace only seen in the 1980s. Amid this long-term bullishness for tech, this publication will also highlight the trading opportunities with both QID and SQQQ in view of tech’s earnings results for the December 2022 quarter.

I start with the recent action by the U.S. central bank to provide investors with some perspective.

The Fed’s Move

First, an increase limited to 25bp for the Fed Funds rates, which was almost certain before the FOMC (Federal Open Market Committee) meeting given the progress made in slowing the rise in prices was confirmed. This is its highest level since October 2007 and represents the eighth time the Fed has tightened since March 2022.

More importantly, and against the wishes of many who had been hoping for a pause early this year, rate hikes should continue, with no precise indication of the end of monetary tightening, as the committee wants to achieve a sufficiently tight monetary policy stance to bring inflation down to 2%. Moreover, the central bank acknowledges that inflation is starting to decelerate but remains high and that the process of disinflation has begun while specifying that it is premature to declare victory.

In these circumstances, while core price inflation is falling, wage growth is slowing, and there are signs that the economy is on the verge of a recession, the Fed could still raise by 25 basis points at the March FOMC meeting before pausing, but, even that is not entirely guaranteed given how fast the data is moving.

On the other hand, what is relevant for this thesis – and which also concurs with my previous one concerning the right ETF for a low growth environment – Powell expects “positive growth,” but at a subdued pace this year. This cautiously implies that a recession can be avoided and, noteworthily, economists at Goldman Sachs (GS) are also of the same opinion.

This is a positive for equities in general, but for tech in particular.

Long-Term Tailwinds for Tech Implies Pains for Shorts

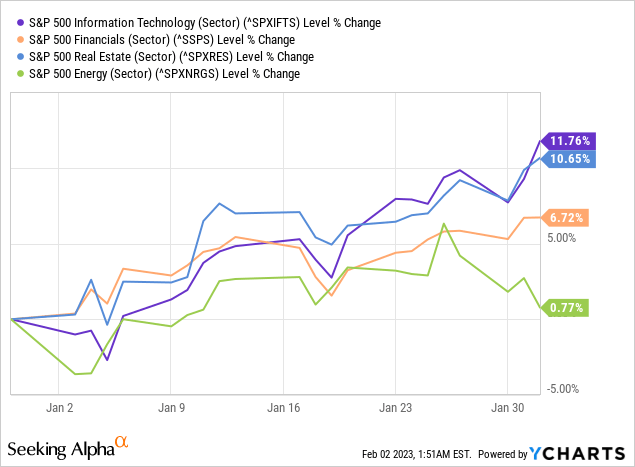

The reason is mostly due to tech being less cyclical than other classical sectors of the economy like financials, real estate, and energy. It is already benefiting from the secular digital transformation trend, which got a boost from the Covid-led working-from-home and migration of IT workloads to the cloud.

I back this statement firstly through the better year-to-date performance of the S&P 500 Information Technology sector, as shown in the deep blue chart below, compared to those from real estate, financials, and energy.

Secondly, the Quant ratings for both of these two ETFs point to a “Strong Sell.”

Third, there is a survey by Gartner, the analyst firm, which has cut its growth projections for IT growth by more than two times for 2023, from 5.1% during its October forecast to 2.4% in January. Nevertheless, this still represents growth and is confirmed by Forrester’s forecast published in January 2023 on the U.S. Tech Market which sees IT spending growing at 5.4% or a fall of 7.4% growth from last year.

All these signify growth in tech, in turn implying longer-term pains for ETFs that short IT stocks, like QID and SQQQ.

The Risks involved in Trading SQQQ and QID

Worst, there are additional downside risks due to both of these ETFs being highly leveraged. In this respect, according to my own experience trading these types of ETFs for the last two years, it is advisable not to trade them over longer periods of time, with the risks also flagged by Seeking Alpha. These revolve around the possibility of suffering from value erosion of your portfolio by holding on to these highly leveraged ETFs, in the hope that just like for buy-and-hold investments, they will offer prospects for turnarounds.

Furthermore, due to their high fees of 0.95% and compounding-related losses, they face a phenomenon called ETF decay, meaning approaching zero dollars in value. Avoiding a buy-and-hold investment strategy for these ETFs is also recommended by the Securities and Exchange Commission, as well as ProShares themselves which highlight losses due to the compounding effect as pictured below.

Important Considerations for SQQQ and QID (www.proshares.com)

On the other hand, as pictured above, Proshares states that one common use of inverse exposure is to seek profits from a market decline. In this respect, both SQQQ and QID could benefit from a temporary decline in the Nasdaq composite.

Profiting from Tech’s Brief decline to Trade QID and SQQQ

First, QID, as a short ETF, seeks a return that is -2x the return of the Nasdaq-100 Index. As such, with 49.8% of exposure to IT, this index is highly concentrated in big techs with names like Microsoft (NASDAQ:MSFT), Apple (NASDAQ:AAPL), Amazon (NASDAQ:AMZN) Alphabet (NASDAQ:GOOG), Nvidia (NASDAQ:NVDA), Tesla (NASDAQ:TSLA), etc., as shown below.

Nasdaq-100 holdings (www.proshares.com)

Second, SQQQ also provides inverse exposure to the Nasdaq-100’s list of holdings (above), but at an accelerated pace of three times (-3x).

However, the earnings for the quarter ending in December 2022 have been disappointing for the likes of Apple, Amazon, and Google. The problem varies from supply chain issues for the iPhone company, lower demand for the world’s largest online retailer while the search giant faces lower advertising spending by online advertisers, etc. However, investors have not dumped their stocks, as they seem to be paying more attention to the companies’ ability to improve profitability through job cuts in the longer term.

However, others may not have the same chance when they report earnings next week, especially chips stocks because of market cyclicality, with overall semiconductor sales for November having decreased by 9.2% year-over-year in November. This could impact electronics manufacturing companies and, combined with inflation and consumer credit data coming next week, there could be a decline in the value of the Nasdaq composite, thereby undoing the one-month 17% upside seen by QQQ.

Conversely, both SQQQ and QID could see gains. In this respect, just a 10% appreciation could result in SQQQ reaching $36.3 (33 x 1.1) based on its current share price of $33. For QID, I have a $20.7 (18.8 x 1.1) target based on its share price of $18.8.

Comparison with Peers (www.seekingalpha.com)

Noteworthily, the comparison table above indicates that despite QID being incepted four years before SQQQ, its asset under management is still $426.8 million or less than six times its peer. The same can be noticed for the average traded daily share volume. All these show that the two-time short ETF is much less popular than SQQQ as a trading tool.

This means that traders have a preference for SQQQ, as it delivers more gains than QID each time the Nasdaq suffers. However, again clinging to my cautionary stance, this higher performance is due to its use of a higher degree of leverage, which means higher volatility as well. This volatility in turn means that the returns one expects will be significantly different from those actually obtained, especially when holding for periods of greater than one day, and one should monitor their trade at least on a daily basis.

Conclusion

Therefore, this thesis has made the case for trading opportunities provided by both of these bearish ProShares ETFs, but, at the same time, the risks involved when trading these leveraged ETFs over long periods, or more than one day, have been thoroughly amplified.

To further justify my cautionary instance and focusing on the top holding or Microsoft, the software giant can rely on its huge cloud platform called Azure as a disinflationary tool, or one which companies can migrate their IT workloads, and subsequently benefit from the Opex charging model, instead of investing heavily in capital-intensive hardware infrastructure to support their core businesses. Thus, according to research by Forrester, software-related expenses which include SaaS, or Software as a Service, will be a major contributor (34%) to tech spend 2023 as corporations actively look for cost savings in a business environment where inflation and high borrowing costs have raised the cost of doing business.

Furthermore, big tech has already demonstrated an ability to use AI artificial intelligence to bring innovations along their value chain, in such a way that increases productivity. Now software and AI can both drive demand for hardware and semiconductors for data centers as hyperscalers themselves invest in infrastructure to provide SaaS to companies wanting to adopt a cloud-driven Opex cost model. Against such a backdrop, it is not advisable to bet against tech for the long term and, instead, it is better to place a trade shorting the Nasdaq after its 17% rise in the last month.

Finally, the non-farm payrolls increased by 517K on Friday, which was well above the consensus. Thus, despite big tech cutting jobs, the service sector remains strong, which can drive up core inflation and result in the Federal Reserve continuing its hawkish stance. Now, higher interest rates are not good for equities, but bode well for shorting tools like QID and SQQQ.