Linde: A Stellar Company For The Long Run (NYSE:LIN)

audioundwerbung/iStock via Getty Images

Linde (NYSE:LIN) is a great company serving diverse customers across multiple industries. The company has always been a star performer in its sector, and investors have highly valued it. But, strong inflation and labor market continue to be a problem for the Federal Reserve looking to get inflation down to its 2% target. U.S. consumers and businesses are under increasing stress as the Federal Reserve raises interest rates. Given these headwinds facing the economy, the U.S. could enter a recession, and the markets could take a beating. The Linde stock is overvalued at this time.

Exceptional profit margins

The company saw a decline of 4.8% in y/y quarterly revenue growth in the December quarter, but the company’s gross margins improved to 43% compared to the September 2022 quarter. Volume was down about 1% in the December quarter compared to the same quarter in 2021. The y/y price increase of 8% helped the company sustain its revenues. The CFO, Mark White, warned about the uncertain economic conditions heading into 2023, which could affect revenue and profitability. But, the company signs long-term supply contracts with its customers, which should offer some protection against an economic downturn.

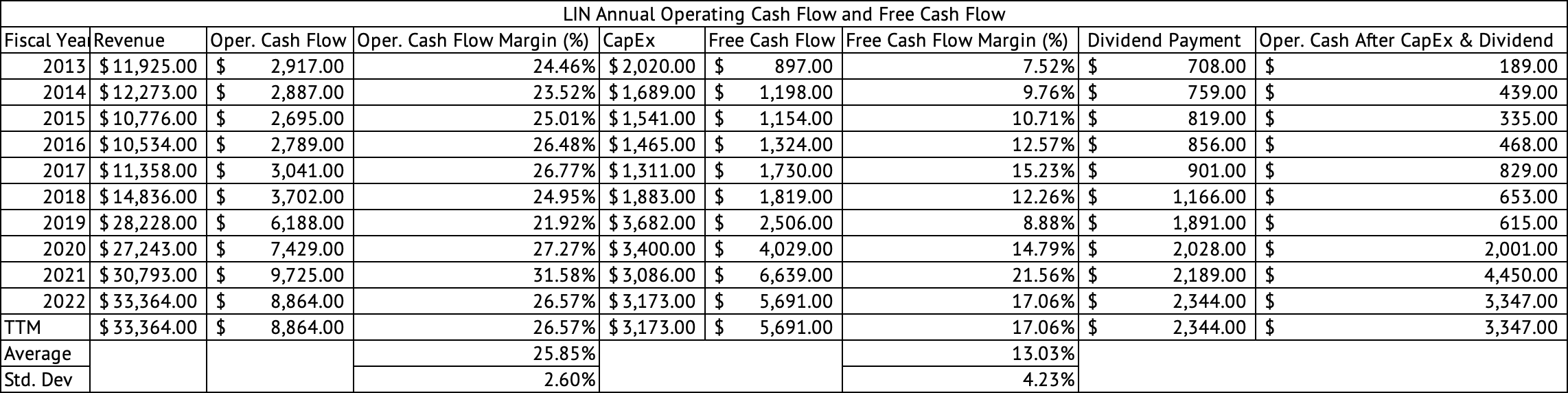

UBS estimates that Linde is one company that has good operating cash flows, which should protect its earnings. The company has excellent margins overall. Its EBITDA margin is over 30%. The company’s free cash flow has averaged 13% annually over the past decade (Exhibit 1). The company’s free cash flow margins have averaged 18.5% since June 2020 (Exhibit 2). The quarterly free cash flow margin was 14.6% for December 2022.

Exhibit 1:

Linde Annual Operating Cash Flow and Free Cash Flow (Seeking Alpha, Author Compilation)

Exhibit 2:

Linde Quarterly Operating Cash Flow and Free Cash Flow (Seeking Alpha, Author Compilation)

Tax subsidies in the U.S. and Europe drive hydrogen investments

The company has signed a long-term agreement to supply clean hydrogen to OCI’s blue ammonia plant in Texas. Linde is investing $1.8 billion in this hydrogen project. The inflation reduction act has improved the returns on clean hydrogen investments. There are $85 per ton tax credits for carbon capture and sequestration and $3/kg for producing green hydrogen (Exhibit 3). The company is eyeing nearly $30 billion in carbon capture and hydrogen production investments in the U.S. (Exhibit 4).

Exhibit 3:

Hydrogen and Carbon Capture Tax Credits Offered by the U.S. Federal Government (Linde Investor Presentation)

Exhibit 4:

Linde’s Decarbonization Investment Opportunities (Linde Investor Presentation)

Several materials companies have jumped on the hydrogen, EV, and decarbonization bandwagon spurred on by the massive tax subsidies offered by the U.S Federal and state governments. Darling Ingredients (DAR) has invested in renewable diesel, and Eastman Chemical is investing in renewable plastics and hydrogen. The California Air Resources Board subsidizes the Tesla Semi. The California Air Resources Board is an obscure California government entity that may be one of the most potent environmental agencies in the country. This entity is fully funded by the cap-and-trade system that California implemented. The cap-and-trade auctions in California generated $19.2 billion in Greenhouse Gas Reduction Funds [GGRF] at the end of 2022. Those funds are used for various environmental and conservation efforts around the state.

Massive share repurchases have helped grow EPS

Between 2013 and 2022, the company spent $17.9 billion in share repurchases while issuing $922 million in shares. Since 2013, the company has generated $50.2 billion in operating cash flow and $26.9 billion in free cash flow (operating cash flow – CapEx). The company generated $13.3 billion in operating cash after accounting for CapEx and dividends.

In short, the company has used debt financing to complete some of its buybacks. Share repurchases benefit management more than shareholders. Earnings per share get a boost from share repurchases even when the company’s revenue and profits have not changed. The earnings per share boost received from repurchases make valuation metrics such as price-to-earnings look cheap. The company’s share buybacks have reduced the share count from 529.1 million in June 2020 to 497.9 million in December 2022, a reduction of 5.8% (Exhibit 5).

Exhibit 5:

Linde Quarterly Share Repurchase, Shares Issued, and Diluted Share Count (Seeking Alpha, Author Compilation)

The company offers a meager dividend yield of 1.46%. The U.S. 2-Year Treasury yields 3x more than Linde. The company’s GAAP payout ratio is 56%, and the company paid $586 million in dividends for the December 2022 quarter and $2.3 billion over the past four quarters.

Linde’s pricey valuation

Linde looks overvalued based on almost every metric. Its forward GAAP PE is 27.9x. The forward PE seems cheap compared to its five-year average of 33.5x. But, interest rates have increased substantially over the past year, decreasing the value of future earnings and increasing the cost of capital. The company carried total debt of $17.9 billion and net debt (after cash) of $12.4 billion. The company generated EBITDA (Operating Income + Depreciation & Amortization) of $10.8 billion, giving it a Debt-to-EBITDA ratio of 1.65.

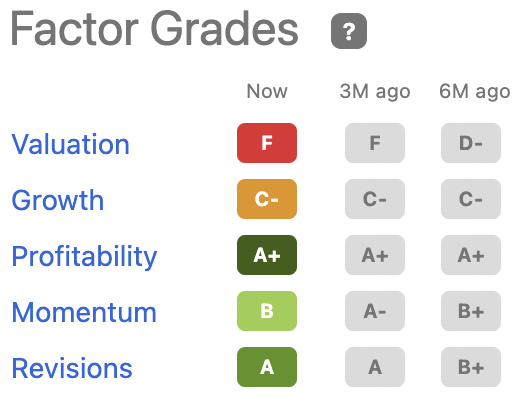

The company has excellent profit margins and generates much cash, but its current valuation is a cause for concern. The Seeking Alpha factor grade gives the company an “F” for its valuation (Exhibit 6).

Exhibit 6:

Linde’s Seeking Alpha Factor Grades (Seeking Alpha)

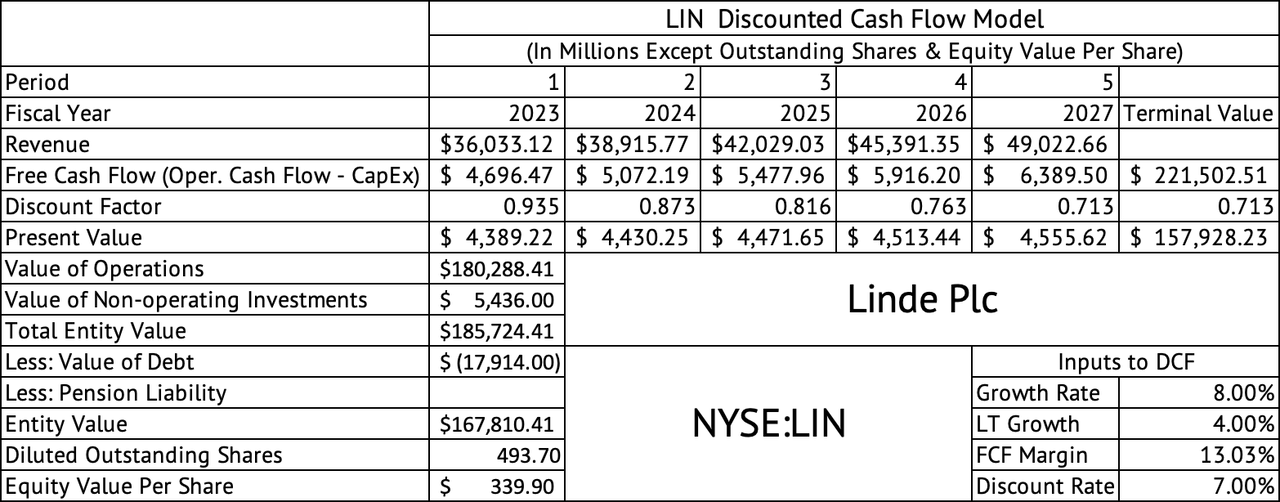

A discounted cash flow model estimates an equity value of $339.90 (Exhibit 7). The stock is trading at $321. This model makes some optimistic assumptions for the company’s growth rate and cost of capital. It assumes a short-term growth rate of 8% until 2027 and a long-term growth rate of 4% for the terminal value calculation. The company’s cost of capital is assumed to be 7%, a liberal assumption given that the risk-free 2-year U.S. Treasury yields 4.6%.

Exhibit 7:

Linde Discounted Cash Flow Model (Seeking Alpha, Author Calculations)

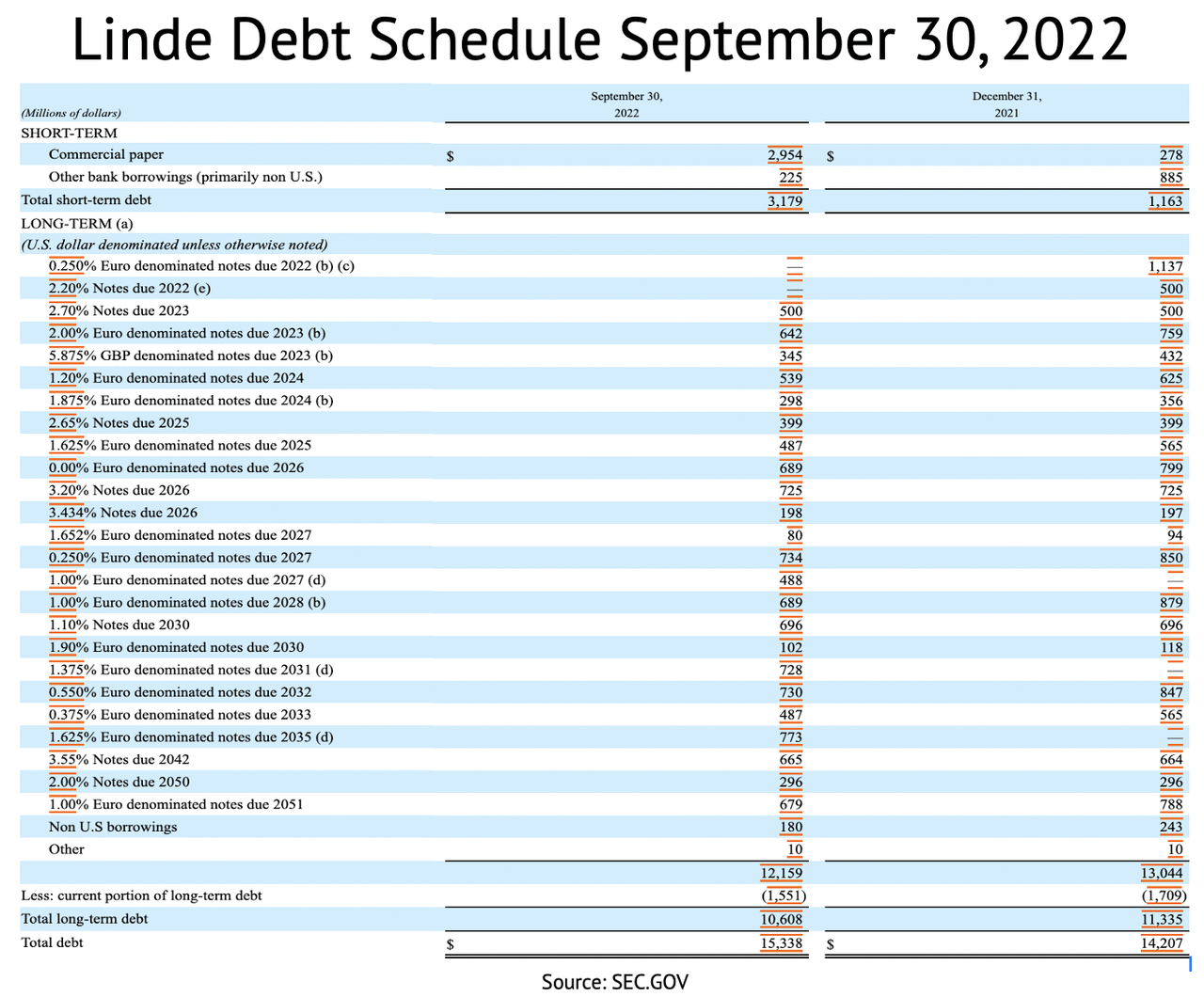

During the zero Fed Funds rate era, many companies have locked in ultra-low interest rates on their debt. Linde’s capital cost is much lower than the U.S. 2-year Treasury yield. The company’s debt schedule shows that the highest interest rate paid is 5.875% on a $345 million GBP-denominated note due in 2023 (Exhibit 8). The company’s cash flows can quickly pay off this debt.

Exhibit 8:

Linde Debt Schedule (SEC.GOV)

The uncertain economy may yet affect Linde

There are very few companies on par with Linde, but it may be worth waiting for a pullback. There is much uncertainty in the direction of inflation and interest rates. The Producer Price Index [PPI] data released on February 16 showed that inflation continues to be a challenge, with the PPI for final demand goods and services increasing by 6% Y/Y. Investors may be beginning to realize that inflation needs to fall faster for the U.S. Federal Reserve to pause hiking interest rates. Further interest rate hikes may reduce economic growth or push the U.S. economy into recession.

It is still being determined how much the economy will have to slow to reduce labor demand, thus reducing demand for products and services and thus reducing inflation. At this point, the Fed’s 2% inflation target looks a long way away. Unemployment has been low, with labor force participation rates declining during the pandemic. The Russia-Ukraine war rages on with no end, with both sides seemingly deadlocked. The war could yet throw a wrench in the best-laid economic plans. The debt ceiling issue may cause market turbulence over the summer months. In short, quite a few known uncertainties could cause an increase in volatility and a drop in the markets.

Linde has tremendous long-term growth prospects and profit margins. It generates excellent cash flows and has deftly used it to buy back shares and bolster earnings per share. The company is overvalued and may suffer a downturn in revenue and profits if the U.S. economy enters a recession. The company’s dividend yield is too low for the current environment. It is best to wait for a drop in the share price before buying Linde.