Lessons From The Collapse Of NOPE (NYSEARCA:NOPE)

marchmeena29/iStock via Getty Images

Author’s note: This article was released to CEF/ETF Income Laboratory members on January 30th.

I first heard of the Noble Absolute Return ETF (NYSEARCA:NOPE), a relatively young, actively-managed leveraged long-short equity fund, in late 2022. NOPE’s strategy is quite aggressive, and so returns are strongly dependent on management investment decisions and executions. At the time, NOPE’s performance track-record was quite short, so thought it prudent to wait a couple of months before tackling the fund.

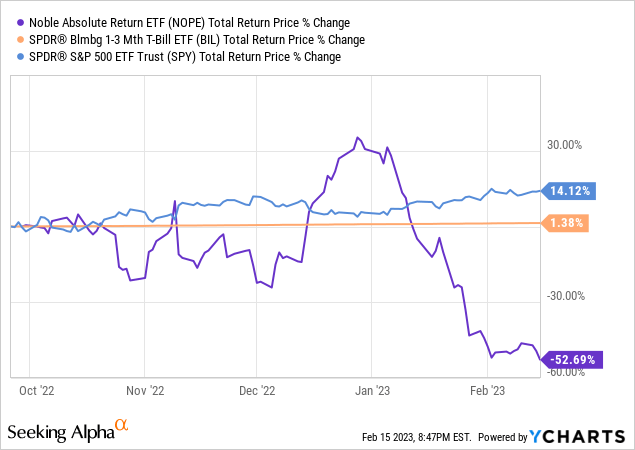

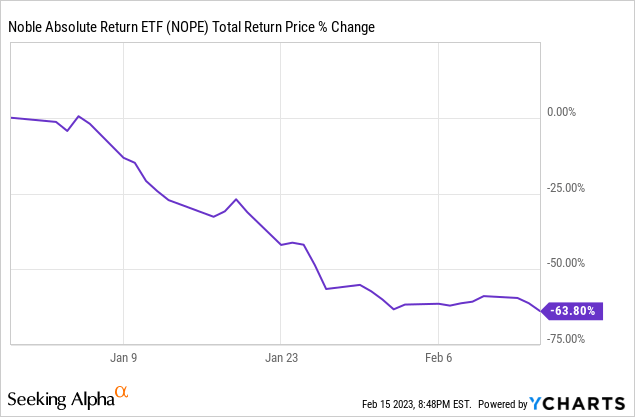

A few months have passed, and NOPE has been one of the worst-performing ETFs since, with the fund down over 60% YTD. Results were disastrous, so thought an article looking at the causes, and possible lessons, from the fund’s performance was in order.

NOPE underperformed due to bad investments and trades, excessive concentration and leverage, and ineffective, conservative long positions. Excessive concentration and leverage were key, as these amplified losses to unacceptably high levels. A more conservative fund, with more diversification and less leverage, would almost certainly have performed much better than NOPE, even with comparable asset allocations and investments.

As of today, the fund is significantly less concentrated and leveraged than before. As such, and in my opinion, the fund should perform much better moving forward. Nevertheless, considering NOPE’s disastrous performance track-record and lack of clear positives, I would not be investing in the fund at the present time.

NOPE – Overview

NOPE is an actively-managed leveraged long-short equity fund.

NOPE goes long equities and equity ETFs which management believes are likely to outperform moving forward, short those which management believes are likely to underperform. NOPE considers both fundamental and price factors when making these determinations / decisions. NOPE invests in equities across regions and industries.

NOPE is a leveraged fund. Leverage varies, but the fund is generally around 150% long, 100% short.

NOPE’s strategy is such that fund returns are strongly dependent on management decisions. Pick the right industries and stocks, and returns could be sky-high. Pick the wrong ones, and returns could plummet. Execution matters too. Proper positioning can limit the damage from any underperforming investment, while excessive leverage can turn manageable losses into a catastrophe.

Right now, and since inception, the fund has been short frothy growth / tech names, including Tesla (TSLA) and the ARK Innovation ETF (ARKK), almost certainly on valuation grounds. Right now, the fund is mostly long SPDR Bloomberg Barclays 1-3 Month T-Bill ETF (BIL). Right now, and since inception, the fund has been long commodities and other undervalued sectors and assets.

In general terms, the fund’s overall investment strategy and outlook seems clear enough. NOPE is broadly bearish, especially on frothy tech. NOPE is positioned to take advantage of the (possible) coming market crash with short positions in the most overvalued stocks, and long positions in short-term assets like T-bills. In NOPE’s manager’s own words:

People ask what should I buy? The answer is you should be in cash,” in order to prepare for “much, much, much lower levels ahead.”

That’s management’s view, and the fund reflects that.

Although I’m much more bullish than NOPE’s managers, the overall outlook seems reasonable enough. Lots of tech and growth companies look overvalued. The Fed might be forced to engineer a recession to combat inflation. T-bills offer +4.5% yields. Perhaps going all-in on T-bills is the right call. It was the right call in 2022 at least.

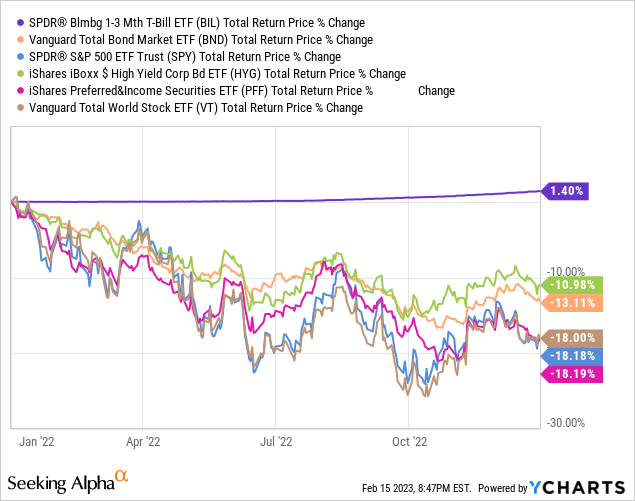

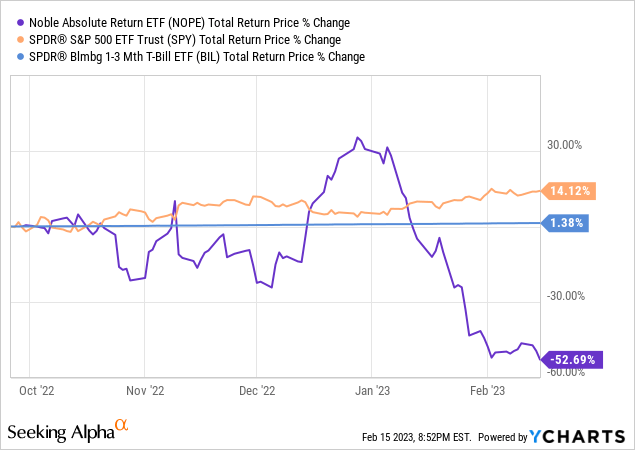

Notwithstanding the above, NOPE’s actual performance track-record is disastrous, with the fund down over 50% since inception, significantly underperforming all asset classes, including T-bills.

Disastrous results. Let’s have a look at their causes.

NOPE – Underperformance Explained

NOPE – Bad Investments and Trades

NOPE’s losses are almost entirely concentrated in 2023:

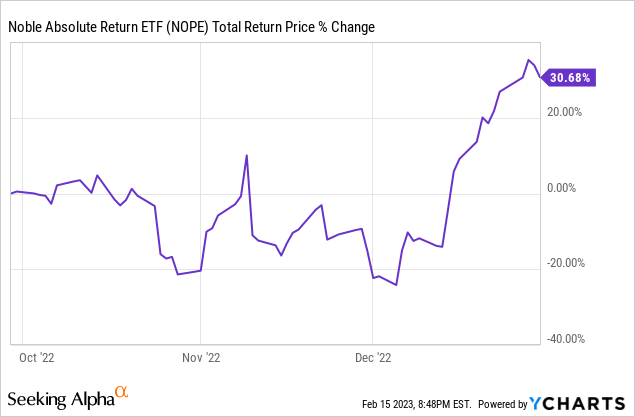

With the fund performing exceedingly well before / in 2022:

NOPE has suffered significant losses YTD due to a series of bad investments and trades. The fund entered the year with a massive 70% short position in Tesla. Tesla’s share price is up for the year, and by a lot, so said position has led to significant losses for the fund and its shareholders so far.

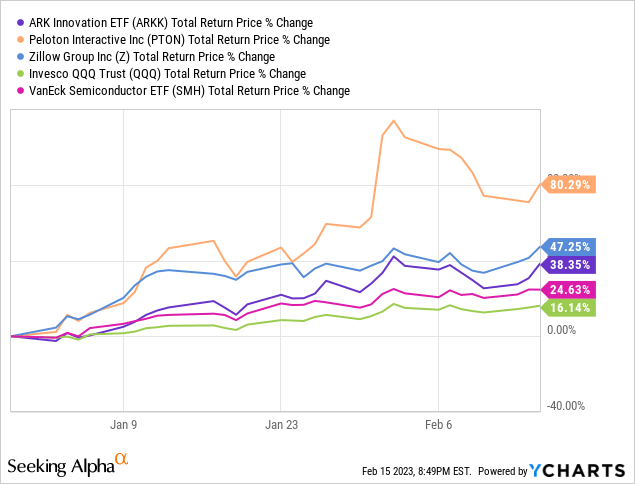

Some of NOPE’s other short positions have been unprofitable too, including ARKK, Peloton (PTON), Zillow (Z), as well as those focusing on the broader tech industry.

NOPE is short growth tech. Growth tech is up YTD, so NOPE is down YTD. Seems simple enough.

NOPE – Excessively Concentrated, Overleveraged Positions

As other commentators have noted, NOPE makes excessively concentrated trades. The fund’s short Tesla position oscillated between 70% – 80% of its NAV in prior months. Short ARKK was another 30% – 40%. Several other short positions had double-digit weights. NOPE invested in leveraged ETFs, although allocations to these were small.

These were excessively aggressive, concentrated bets. Something goes wrong and the fund suffers significant, perhaps irrecoverable, losses, and something always goes wrong, sooner or later.

In this particular case, the fund’s largest short position, Tesla, is up over 95% since its bottom in late December:

A more conservative fund, with single-digit short positions would have seen some losses, but nothing disastrous, from a short Tesla position. NOPE, with a massive 70% – 80% short position in Tesla, suffered significant, effectively irrecoverable losses.

Leverage magnifies the issues above. Leverage means more assets (or larger short positions). More assets, or larger short positions, means more losses when these are unprofitable, as has been the case in 2022.

Leveraged funds are sometimes forced to sell assets at fire-sale prices, for regulatory reasons. Unclear if this was the case for NOPE, but it is generally the case for funds that suffer significant losses like NOPE.

On a more positive note, the fund seems to have significantly reduced the size of some of their larger position these past few days. As an example, the short position in Tesla has been reduced to around 33%. Still quite large, but much lower than the 70% – 80% in the past. There is, however, no guarantee that position sizes will remain at these levels moving forward.

NOPE – Ineffective, Conservative Long Positions

NOPE is currently long T-bills. Although these are incredibly safe securities with good yields equities have much stronger long-term expected returns. Equities have outperformed T-bills since the fund’s inception, so going long T-bills has been the wrong call so far.

Long equities is preferable to long T-bills for reasons of portfolio construction too. Some context first.

Stocks mostly go up, so shorting stocks is a difficult, generally unprofitable business. Chanos, one of the most successful short sellers in history, loses money shorting stocks, with average annual returns of -0.7% for his short positions. Importantly, Chanos actually generates significant alpha, or outperformance, in his shorts. The average stock sees returns in the 8% – 12% range per year, so Chanos is definitely picking subpar, below-average stocks, just not terrible enough to generate positive returns.

So, shorting does not work as a means to generate positive returns. At least not easily, consistently so.

Shorting can work as a hedge in a leveraged, net long portfolio.

A fund might, for instance, decide to go 200% long SPY, 100% short Tesla, for a net 100% long equity exposure (200% SPY – 100% Tesla = 100% long equity).

Long-term expected returns are strong, as the fund is net long equities, and equities mostly go up.

The leveraged SPY position would see significant, perhaps irrecoverable, losses during a bear market, but the short Tesla position should help hedge said losses.

The short Tesla position has negative long-term expected returns, stocks mostly go up, including Tesla, but the leveraged long SPY position should more than make up for this.

With a solid strategy and execution, a leveraged long / short equity fund like the one above can deliver outstanding returns, as Chanos has done for decades. It is much more difficult for a long T-bill / short equity fund to do so, as T-bill returns are much, much lower, and might not necessarily cover short position losses. Remember, equities have outperformed T-bills since NOPE’s inception, so fund performance would have been much stronger if the fund’s managers had followed Chanos’s overall strategy.

Conclusion

NOPE has significantly underperformed YTD due to bad investments and trades, excessive concentration and leverage, and ineffective, conservative long positions. Although the fund has taken steps to ameliorate these issues, the fund remains excessively risky, and with a disastrous performance track-record. As such, I would not be investing in the fund at the present time.