KLAC Will Benefit From CHIPS Act And The Infrastructure Supercycle

Editor’s note: Seeking Alpha is proud to welcome Michael Del Monte as a new contributor. It’s easy to become a Seeking Alpha contributor and earn money for your best investment ideas. Active contributors also get free access to SA Premium. Click here to find out more »

PhonlamaiPhoto

“Semiconductors form the foundation of the technologies that drive America’s economy, national security, and critical infrastructure.” – Bob Bruggeworth, president and CEO of Qorvo, and 2021 SIA board chair.

The semiconductor equipment manufacturing subsector is set up for incredible growth. There is currently $52.7b in government funds sitting on the sidelines waiting to be allocated to the development of new U.S. foundries. With the ongoing trade war with China, it has never been more pertinent that we secure our semiconductor supply chain and advance the manufacturing process domestically. Between Intel (INTC), Taiwan Semiconductor (TSM), Samsung (OTCPK:SSNLF), and Texas Instruments (TXN), around $70b will be invested in the development of new domestic foundries. Given their economical and advanced technological approach, I believe KLA Corporation (NASDAQ:KLAC) is the most well-positioned semiconductor equipment manufacturer to take advantage of this advancement in the domestication of the semiconductor supply chain.

According to McKinsey, the semiconductor industry will grow to $1T by the end of the decade. Allied Market Research projects the semiconductor manufacturing equipment market to expand from $87b in 2021 to $210b by 2031. The U.S. Department of Commerce suggests that $250b of economic growth has been lost due to the semiconductor shortage in 2021. In accordance with the CHIPS act, $50b will be allocated over the next five years for the development of semiconductor manufacturing in the U.S. – $11b allocated to R&D and $39b allocated to domestic chip production. To boost 5G technology, $2b will be allocated to the DoD for microelectronic research, fabrication, and workforce training. On top of this, a 25% tax credit will be allocated to those developing this process control technology.

KLAC’s machines might not be seen by the average consumer, but the products they develop are very much at the forefront. From the smartwatch, smartphone, smart refrigerator, and thermostat to the most sophisticated high-performance computer, they all utilize chips that are manufactured and tested using KLAC and the like’s products. Many of the chips produced by their machines include advanced logic, DRAM, 3DNAND, power devices, MEMS, and legacy design node chips, among others.

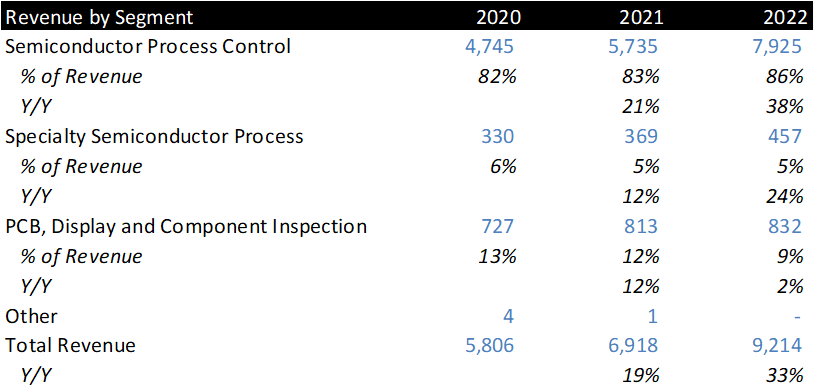

The specialty semiconductor process, which is comprised of etching and deposition solutions for advanced packaging and specialty semiconductor market, was “driven by advances in the IC packaging technology roadmap and growth in demand for automotive power, RF filters, and MEMS devices.”

Management has been adamant in pushing further into the automotive industry and, given the current state of things, they might be coming in at just the right time. The automotive industry has experienced a very sluggish recovery since 2020 given lower production rates, despite heightened demand. One major cause to the supply constraint has been the ability to source analog chips. KLAC’s biggest growth driver in this space is the paradigm shift of auto manufacturers bringing the design in house and working hand in hand with KLAC. Given the direct tie to design, KLAC might have an advantage in the upswing in auto manufacturing.

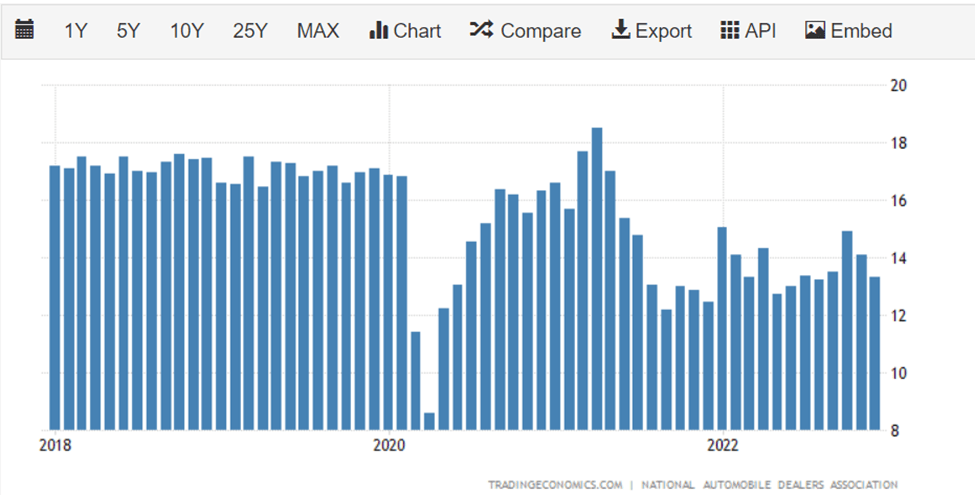

TradingEconomics

KLAC’s business is dependent on the capital expenditures of semiconductor-related and electronic device manufacturers. Growing adoption of higher computational power and connectivity for markets in artificial intelligence, 5G technologies, electric vehicles, IoT, PC, mobile devices, and intelligence in autos will drive more leading-edge design node technology investments and capacity expansions.

There have been some major drawbacks uncovered for memory chips. Global shipments for PCs fell 29% for 2022 and aren’t expected to recover until 2024. Micron Technology (MU) warned of a huge memory chip production drop off, cutting production by 20%. Analog Devices (ADI) also warned of a slowdown in consumer chips in the double digits. Samsung sounded the alarms, expecting a 69% drop in profits for the next quarter, coming off a backdrop of revenue declining 8.6% in their recently reported quarter. Lastly, Taiwan Semiconductor, one of the largest chip foundries, is expecting revenue to drop by 5% for the next quarter.

That said, that’s just for 2023. Long-term mega-trends still exist for the semiconductor space. There are huge technological innovations happening both behind the scenes and in the public eye. One of the major rollouts includes 5G technology. One of the major factors for 5G is the necessity for densification on the radio towers for optimal connectivity, meaning there will need to be more than 10x the base stations for 5G than there were for 4G. This means a higher requirement for RF switches (radio frequency), logic, and applications-specific integrated circuits. Ericsson (ERIC), one of the leading providers of 5G networking equipment, suggested that we’re only in the second inning of a major 5G rollout. Despite the excitement for 5G technology, older wavelengths aren’t necessarily going to be rolled off. For 4G technology alone, Allied Market Research projects the global 4G equipment market to expand from $40b in 2018 to $185b by 2026. Allied Market Research also projected 5G equipment to increase from $5.13b in 2020 to $798b by 2030.

Our nation also has the initiative to electrify the grid, requiring more power management tools. This is especially important given the intermittence of renewable energy sources that don’t necessarily function on a grid that demands a constant power supply. It has become apparent that there are two sides to this coin. This increasing rate environment has made financing wind farms very expensive and might lead to projects being cut.

Given how much more sophisticated semiconductors will become throughout this renaissance of innovation, testing and packaging of chips will become all the more relevant. According to The Wall Street Journal, China currently controls 46% of the testing and packaging market. Given how specialized this process is – especially as 5nm and 3nm chips become more prominent in the market – newer technologies such as optical and EUV testing technology will be a necessity, along with KLAC’s newest plasma dicing technology for cutting wafers for the packaging process. Allied Market Research expects this market to grow from $27b in 2020 to $60b by 2030.

In short, the near-term horizon seems very dismal. However, considering the long-term trajectory of technology, there’s a huge market opportunity to be had, especially if geopolitical tensions persist and China is carved out of the mix.

So, let’s review some of the business and financial aspects of KLAC. CEO Rick Wallace’s top priority before innovation is economics – i.e., his No. 1 goal is to create the most cost effective approach to help clients reach their production goals. This doesn’t necessarily mean creating a cheaper product, but, rather, developing the technology to create chips at the same pace as those developing and manufacturing the chips themselves. An example of this is moving from optical reticle to EUV. KLAC has emphasized that optical isn’t going to be phased out as EUV is transitioned in, but, rather, used simultaneously.

Reviewing their financial statements, the flow-through from revenue all the way down to free cash flow is significantly superior to their competition. KLAC boasts a 61% gross margin and a 44% EBITDA margin, as compared to ASML Holding (ASML) coming in second at 51% GM and 34% EBITDA margin. Shareholders have absolutely rewarded KLAC for their performance. Their one-year total return sits right at 1.8%, while LAM Research (LRCX) is down 30%, Applied Materials (AMAT) is down 27%, and ASML is down 7%. To help you gauge this, the Nasdaq returned -33% for FY22.

KLAC 10-k

One of the biggest challenges for semiconductor equipment manufacturers is going to be geography. With the recent ban on chip and related equipment sales to China, competitors with large concentrations in China will severely underperform. As of FY22, 28% of AMAT’s business is in China. This can potentially affect $2.5b in revenue for AMAT. 31% of LRCX’s revenue is derived from China as well as 15% of ASML’s business. KLAC has exposure of nearly 30% in China. Bear in mind that the ban primarily focuses on leading-edge technology, and not so much legacy business. The majority of KLAC’s business in China is legacy chip-related. Management has suggested roughly $100mm in revenue is going to be affected by the ban with no effect to margins.

By no stretch is KLAC the largest producer of equipment; however, size isn’t everything – clearly. Smaller producers can typically be nimble and more intimate with their clients. On a performance basis, it’s clear KLAC has a stronger execution without hindering the economics of capacity.

On a comps basis, KLAC trades relatively in line with its peers; however, the share price should outperform given the company’s growth trajectory.

VLSI

Automotive is going to be a major push for KLAC’s performance. As supply chains are brought closer to home, auto chips are no exception. KLAC is working directly with auto manufacturers in designing the next generation of chips to go into the vehicles. New automobiles require somewhere between 6,000 and 10,000 chips to make the vehicle run. This includes 100 connected electronic units (ECUs), flat panel displays, circuit boards, specialty semiconductors, and packaging components. In addition, testing these chips will become even more vital to performance to ensure car accidents aren’t a result of faulty chips in the vehicle.

I also believe testing and packaging will become a bigger piece of KLAC’s revenue stream. Though display and component inspection only accounts for 9% of total revenue, I believe there’s a huge growth driver that isn’t being discussed. Keep in mind that 46% of inspection is done in China (2% in the U.S.). Inspection and packaging is the final step to developing a chip and could be the most vital piece to the puzzle. To fully secure the process from end to end, inspection and packaging must be built out domestically to reduce geopolitical risk, especially if tensions escalate between China and Taiwan. At this point, management expects a 24% CAGR through 2026 for their packaging business. This might be mindful of geopolitical risk as well as newer technology releases, such as plasma cutting for more advanced chips.

To add a little pizazz to their revenue stream, a major part of KLAC’s business is their services component, which is primarily sold on a SaaS basis. Leadership boasts that utilization of KLAC’s services allows better optimization in chip production, faster upgrades, and better servicing of their equipment. It’s almost as if management took a page out of Jeff Bezos’s book in prioritizing the customer experience. Though not directly broken out on their reported financials, 22% of total revenue is accounted for in services across all segments. 75% of this revenue is generated on a subscription basis with a three-year subscription period, growing at a 4.5x clip compared to their installed base. Much of the support is done remotely with the utilization of AR/VR technology, which allows KLAC to cut down on travel expense, and offer faster support, and the ability to utilize the top expert from anywhere around the world.

KLAC 10-k

The biggest risk leadership has voiced in this current economic climate is the specialty semiconductor segment for logic chips. Logic chips are expected to see a pullback of 22% in the near term; however, scaling should return to 23% from there on out.

My final rationale for an investment in KLAC resides back to the drive to bring supply chains closer to home. In March 2021, Intel announced the development of two new foundries with the estimated investment clocking in at $20b. Samsung did much the same, announcing a $17b fab due in early 2023. TSM will also be developing a fab in Arizona 5nm and 4nm chips with the expectation to be up and running by Q1 2024. Texas Instruments is planning to build two new foundries with the first online in 2025 with a total investment of $30b.

There’s a ton of money that’s going to be pumped into the development of the industry over the next five years, let alone the next decade, to keep up with the expansion of how we utilize chips in our daily lives. I believe KLAC’s product line is set up for success in this process.

Let’s Talk Catalysts

Positive

- The adoption of more advanced packaging technologies such as plasma for more accurate wafer cutting;

- a total ban on chips and associated technologies to China along with strengthening geopolitical tensions with Taiwan;

- a strong comeback in the automotive industry driving the utilization of more advanced chips; and

- electrification of the grid, further 5G development, and greater adoption of smart devices.

Negative

- The chip glut persists, and fab expansions are pushed out;

- challenges in PC sales can lead to suppressed demand for leading-edge chips and potentially lower investment in expansionary projects;

- trade with China returns to business as usual, impeding the necessity to drastically expand fabs domestically;

- a more severe economic recession causes the automotive industry to produce and sell less vehicles, leading to lower chip volume demand;

- consumer credit becoming very extended with dwindling savings that can lead to reduced purchases of vehicles, smart appliances, and smart phones; and

- much of the U.S. is in a drought and foundries require anywhere between 2 and 4mm gallons of water per day to function, which can lead to lower yields and require less equipment and services.

Conclusion

I believe KLAC will make a great addition to fulfill a portion of someone’s tech leg of their portfolio. I’m personally a shareholder of KLAC. Management has made it a priority to return value to shareholders through their $6b share buybacks and their consistent dividend growth. With their drive to expand margins and flow more cashflow, KLAC has a huge potential to outperform the market. At this time, I value KLAC at $471 based on my 2025 FCF estimate.