DON: Higher Exposure To Financial And Real Estate Sectors Make It Vulnerable In 2023

mphillips007

ETF Overview

Some may wonder whether to invest in large-cap, mid-cap or small-cap dividend funds. In this article, we will analyze WisdomTree MidCap Dividend ETF (NYSEARCA:DON) to see if it is a good investment choice among the three types of dividend funds. As the title of the ETF suggests, DON invests in mid-cap dividend stocks in the United States. The fund has generally performed better than its small-cap peer but inferior to its large-cap peer in the long run. In the near term, its higher exposure to financial and real estate sectors may make it more vulnerable in an elevated rate environment. Therefore, we think investors may want to seek other large-cap dividend funds instead.

YCharts

Fund Analysis

DON underperformed against its large-cap peer since 2022 and in the long run

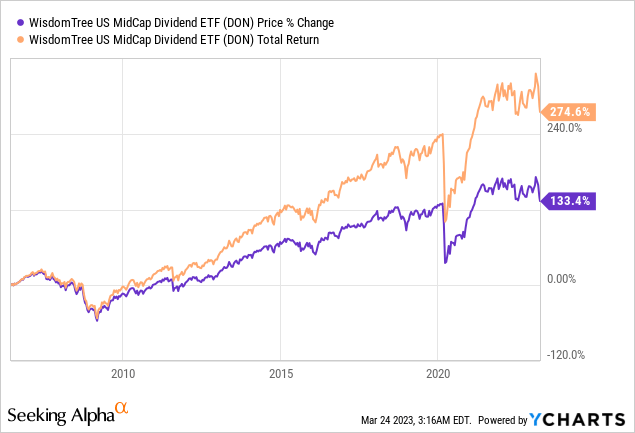

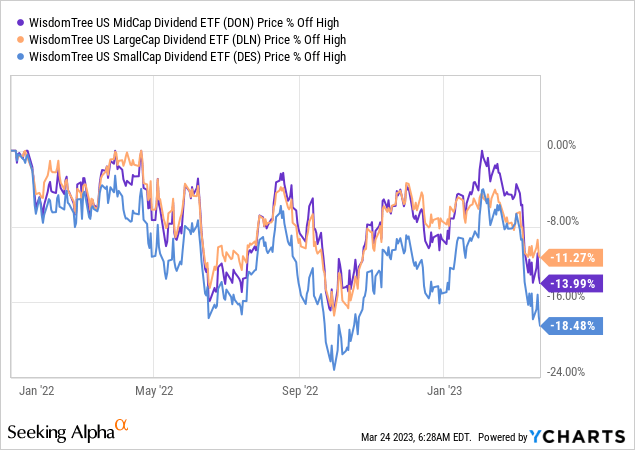

Last year was a terrible year for equities in general. DON was not without an exception. As can be seen from the chart below, the fund has lost nearly 14% of its value since the beginning of 2022. This was better than its small-cap peer, WisdomTree SmallCap Dividend ETF (DES), but inferior than its large-cap peer, WisdomTree LargeCap Dividend ETF (DLN). This was understandable as small-cap stocks usually do not have strong balance sheets than large-cap stocks, and in a rapidly rising interest rate environment such as last year, many small-cap stocks are ill-equipped to combat the headwind. In contrast, large-cap stocks are generally much more established. They tend to have stronger balance sheets and more robust business models.

YCharts

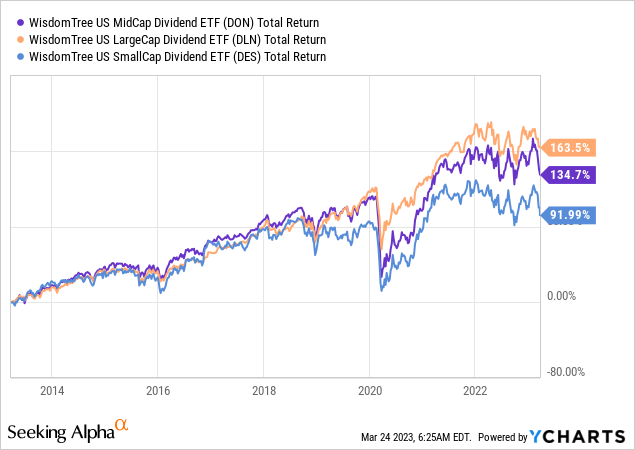

This better performance in large-cap funds over mid-cap and small-cap funds is also evident in the long run. As can be seen from the chart below, DON’s total return of 134.7% in the past 10 years was much better than its small-cap peer DES’s 91.99%. However, DON’s performance was inferior than its large-cap peer DLN’s 163.5%. Not only because large-cap stocks have better balance sheets than their mid-cap and small-cap peers, they tend to have long runways of growth as well. As we know, not all small-cap stocks become large-cap stocks. Even if some of them with good growth potential become mid-cap stocks or large-cap stocks, they will be removed from DES’s portfolio as DES only includes small-cap dividend stocks. Therefore, DES do not reap the benefit of the growth potential of some of its small-cap stocks in its portfolio over a lengthy period. The same also applies to mid-cap as not all mid-cap stocks can grow become large-cap stocks. Even if they do become large-cap stocks, they will be quickly removed from their portfolio.

YCharts

Lower exposure to technology sector is another reason why DON underperformed DLN

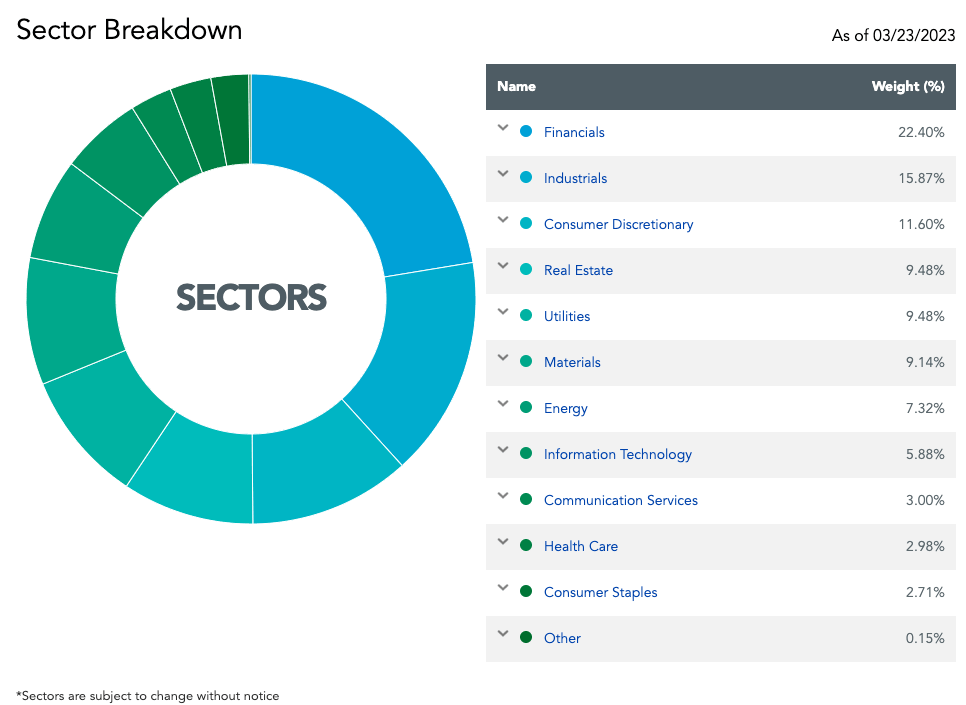

Another reason why DON has not performed well is that it does not have a high exposure to strong growth sectors such as technology sector. As the pie chart below shows, technology sector only represents 5.88% of DON’s portfolio. In contrast, technology sector represents over 18% of DLN’s total portfolio. No wonder DON’s growth is inferior than DLN in the long run.

WisdomTree Website

The fund has higher downside risk than DLN

Not only will DON underperform its large-cap peer DLN, the fund is likely going to have higher risk than DLN. As the pie chart above shows, DON has a high exposure to financials sector which accounts for 22.4% of the total portfolio. Real estate sectors also account for about 9.5% of the total portfolio. In contrast, DLN’s exposure to financial and real estate sectors are only 12.5% and 4.5% respectively. As we know, last year’s aggressive rate hike has caused tremendous stress to the financial system and caused some crisis in several regional banks just the past month. In addition, real estate sector is also under heavy pressure as the rate have risen rapidly and will remain elevated throughout 2023. Therefore, we think DON will have higher downside risk than DLN.

Our base case is a mild recession in H2 2023

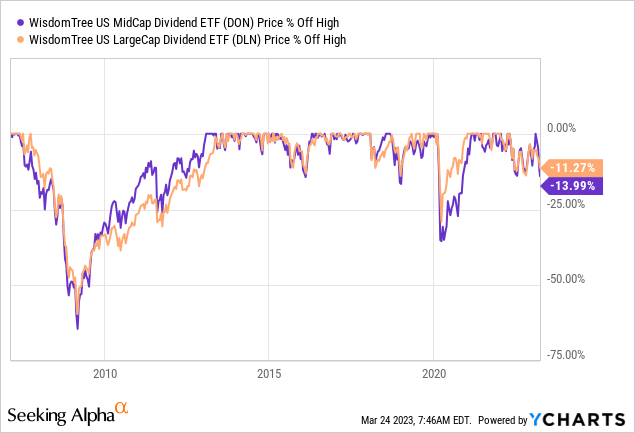

Given that the Federal Reserve is likely going to keep the rate elevated beyond 2023, we think a mild recession will likely be the outcome in the second half of this year. In a recessionary environment, DLN will likely outperform as it has lower exposure to cyclical sectors such as financials and real estates than DON. In addition, we observed that DON has higher downside risk in the previous two recessionary environments. As can be seen from the chart below, DON suffered higher losses than DLN in the Great Recession in 2008/2009 and the 2020 recession.

YCharts

Investor Takeaway

We do not think owning DON is a necessity in this uncertain macroeconomic environment. As we have analyzed, DLN appears to be a better choice in both the near-term and in the long run. Therefore, we think investors should probably invest in its large-cap peer DLN instead.

Additional Disclosure: This is not financial advice and that all financial investments carry risks. Investors are expected to seek financial advice from professionals before making any investment.