BRP Stock Scores When It Counts For Its Seasonal Industry (TSX:DOO:CA)

Eric Panades Bosch/iStock via Getty Images

BRP Inc. (TSX:DOO:CA)(NASDAQ:DOOO) is approaching its next earnings, and we think that the signal given from the last earnings report demonstrates the excellent choices of management that we started reporting on from three quarters ago, and should help deliver an excellent Q4. Inventory management practices were good considering the situation, and Juarez-3 capacity growth begun in 2021 came into play to support building dealership inventories which were excessively low over 2022 due to supply chain issues. Otherwise, the resolution of supply chain issues, admittedly out of their control, and the end coming to retrofit sales, should mean improvement in unit economics and a swing for the fences with seasonal products. DOO’s stockholders know it and have been buying up. With an extending price, we feel we should sit it out though.

Key Dynamics

We’ve been covering DOO for over a year, and this article brings a lot of it together. Inventory buildup has become possible at dealerships, dealing with the pent-up demand issue. Cancellation rates have thankfully been low, and despite inventory buildup the next quarter’s inventory is already 40% pre-ordered.

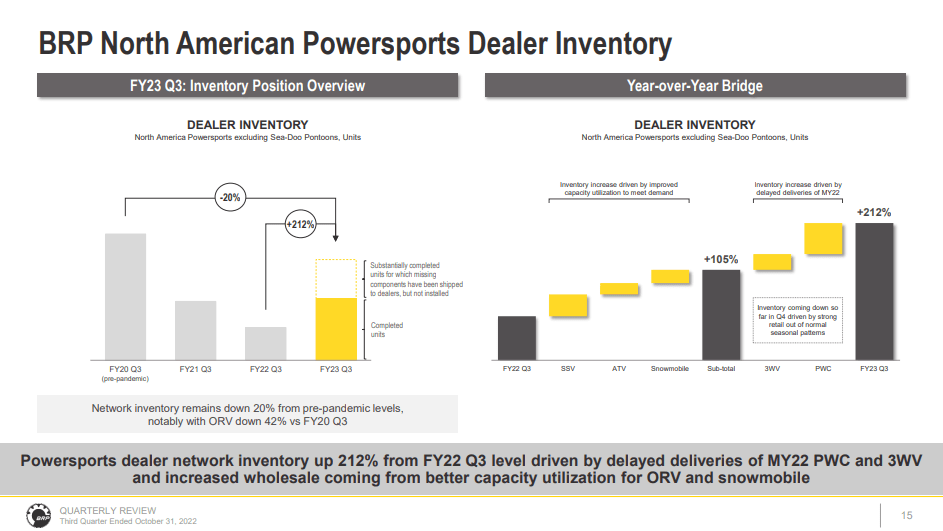

Inventory Buildup (Q3 2022 Pres)

Inventories have tripled, and this has come from two place accounting more or less equally for the growth:

- It grew capacity substantially with projects initiated in mid-2021 at its Juarez facilities, completed at the beginning of 2022, and the greater capacity has been helping the year-round products ship. They are focusing on growth markets like side-by-side to take on the new capacity and ship, where ATVs have been less prioritized since they’re less of a growth area and the category has been hit over the years by bad publicity over safety.

- Supply chain issues have started to resolve, and this matters for the seasonal products which had started to come online in Q3, but will be even more vigorous in Q4 which is full season for snowmobiles in particular, that have been shipping with YoY growth already as of Q3.

There’s also the Sea-Doo pontoon launch which has added organically to the baseline season products revenue.

The evolution in supply chain issues is key. Firstly, dealer inventories needed to build to keep up sales velocity into what appears to be a bottomless market, growing despite credit conditions and consumer sentiment. But the other reason is to do with the fact that they won’t have to do retrofit sales.

Retrofit Sales

Retrofit selling has been an essential dynamic to understand for BRP over the last three quarters. It means taking cash for an unfinished product and shipping it to customers for their ‘early-access’ benefit, then retrofitting them with final elements and recognizing at that point the sale as revenue. They needed to do this to not keep people waiting too long, and it was a good decision to keep up volumes and free manufacturing capacity, but it also hurt the unit economics.

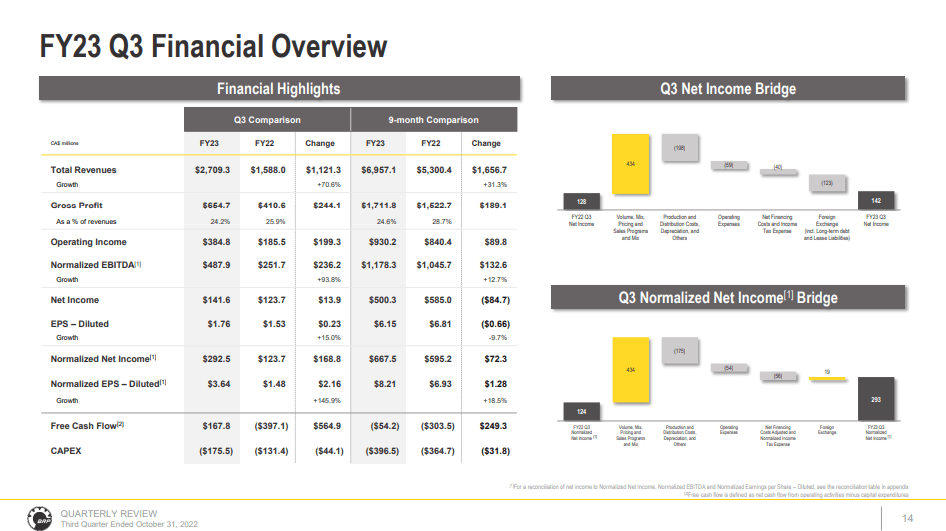

Gross profits have been growing slower than sales for a while now thanks in part to retrofitting, but also of course to generally higher procurement costs.

Financial Highlights (Q3 2022 Pres)

Retrofitting was only necessary because of supply chain issues. Once they come to an end BRP Inc. will see GM improvement.

Bottom Line

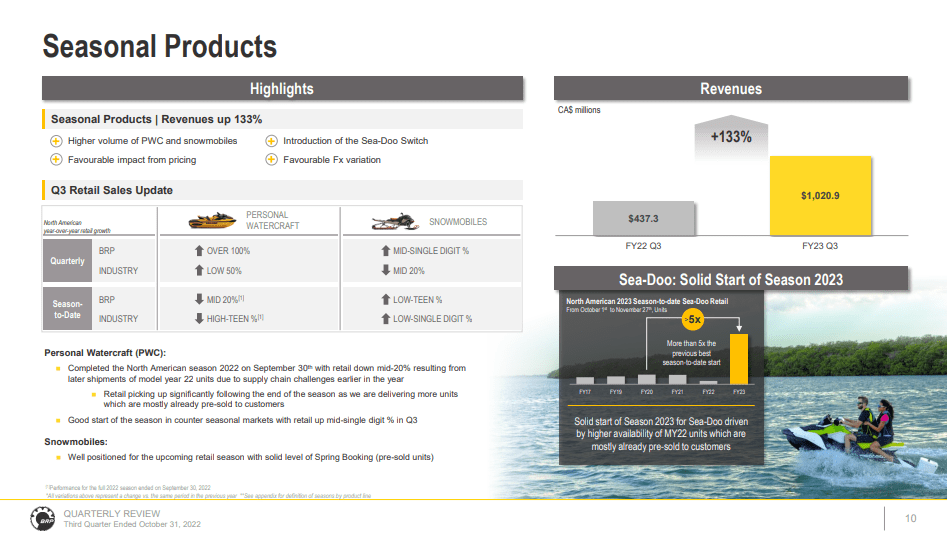

Sales are growing, and not only do resolving supply chain issues and falling logistic costs help keep sales and unit economics improving, but the company specifically early-hoarded inventory for seasonal production like that of snowmobiles to be able to totally outcompete the industry in terms of volumes. They mentioned this some quarters ago.

Seasonal (Q3 2022 Pres)

Profits are rising without issue already thanks to scale, up about 20% in net income for the Q3. Logistics costs are dissipating a bit. Things look good.

The issue is the price is already extended trading back around highs. While the prospects are good and this level is justified – indeed, the multiple isn’t even that high at around 12x PE – we think there are still more beaten down things that can be scouted in the current market, which still has a while till a more certain and vigorous recovery, given macroeconomic factors.