Atmos Energy: EPS Growth Ahead, Bullish Chart Make It A Buy

zorazhuang

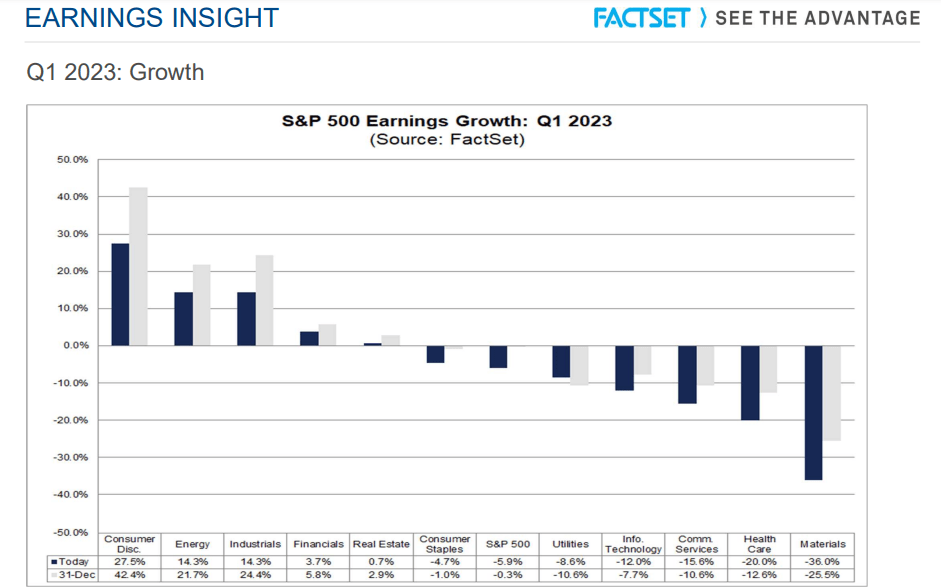

Fourth quarter earnings season is wrapping up. It will be the worst period for S&P 500 EPS growth since Q3 2020. Looking ahead, we may be staring at an earnings recession as the current consensus, per FactSet, is for two more YoY drops in per-share profits for the market.

Q1 earnings growth should be best for Consumer Discretionary and Energy while Health Care and Materials are seen as having the most negative earnings dips. Utilities, meanwhile, are in the middle, but earnings estimates have actually increased since December 31.

I see better earnings growth compared to the sector and market for Atmos Energy, and that’s baked into a valuation premium on the Texas gas name. I see shares as fairly valued today.

Q1 2023 Earnings Growth Rates By Sector

FactSet

According to Bank of America Global Research, Atmos Energy Corporation (NYSE:ATO) is a natural gas transmission and distribution company headquartered in Dallas, Texas. Operations are divided between two segments: Natural Gas Distribution and Regulated Transmission & Storage. The Distribution segment distributes gas to approximately 3mn customers in 8 states located in the South, Southeast, and Midwest.

The Dallas-based $16.1 billion market cap Gas Utilities industry company within the Utilities sector trades at a high 19.8 trailing 12-month GAAP price-to-earnings ratio and pays an above-market 2.6% dividend yield, according to The Wall Street Journal.

ATO has a solid balance sheet with very little in the way of floating-rate debt, but a key risk is a pending resolution in the Texas energy market following the 2021 Winter Storm Uri. But longer-term fundamentals are decent with its financing position in the gas LDC industry. Regulatory developments are a key variable for the stock in the future while a decline in interest rates would benefit the firm. Unfavorable rate case outcomes and increased equity needs are primary risks. The firm increased its dividend last November.

On valuation, analysts at BofA see earnings continuing a robust and steady trajectory through next year. Per-share profits are expected to grow about 7% this year, above the inflation rate, before an acceleration takes place in 2024. The Bloomberg consensus forecast is not far from what BofA projects. Dividends, meanwhile, are seen as climbing steadily with earnings growth. Both the operating and GAAP P/Es still appear stretched here, however.

The latest forward non-GAAP earnings multiple per Seeking Alpha is 18.7, a slight premium to the overall market. I think a fair P/E is closer to 17 on a somewhat stable gas utility, so an intrinsic value of around $110 is right in my eye. Also take a look at the high EV/EBITDA ratio buttressing that case. I acknowledge that the forward operating PEG is below the industry average and ATO’s 5-year average, so risks are to the upside on my valuation.

Atmos: Earnings, Valuation, Dividend Yield Forecasts

BofA Global Research

Looking ahead, corporate event data provided by Wall Street Horizon show an unconfirmed Q2 2023 earnings date of Wednesday, May 3 AMC. Before that, a dividend pay date hits on Monday, March 6.

Corporate Event Risk Calendar

Wall Street Horizon

An early peek into the earnings situation reveals that $2.47 of EPS is the forecast which would be a solid 4.2% advance from $2.37 earned in the same period a year ago. Consider that the broad market’s first-quarter earnings growth rate is seen at –5.9% while the Utes could post a YoY EPS drop of 8.6% per FactSet. So, Atmos has some relative earnings strength at the moment.

Option Research & Technology Services (ORATS) show that ATO has beat on earnings in 11 of the 12 quarters, but missed in its most recent report. The actual earnings-related stock price move has been small, ranging between –3% and +2% in the last two years, so don’t expect major volatility with this name.

ATO: Muted Earnings-Related Volatility

ORATS

The Technical Take

With shares not far from what I deem fair value, the chart is bullish. Notice in the graph below that shares are consolidating right under the all-time high in the low $120s. A rally above, say, $125 would yield a measured move price objective to near $160 based on the basing pattern down to $85. But that could take a bit longer to play out as the RSI momentum indicator shows bearish divergence on a recent rally attempt to the high. There is an uptrend support line that comes into play below the flat 200-day moving average just above $100.

Overall, I like the chart above $125 and would also be a buyer about 10% lower from here with a stop a few dollars under the Q4 2022 low of $98.

ATO: Bullish Consolidation Below All-Time Highs

Stockcharts.com

The Bottom Line

I am a buy on Atmos. The valuation is fair while the growth outlook is solid. The chart is also leaning bullish, so I’m fine deeming it a buy here when putting all the factors together.