Altria: Going On The Offensive (NYSE:MO)

krblokhin

Altria Group (NYSE:MO) announced yesterday that it was making a strategic purchase of NJOY Holdings, an e-vapor company, for a consideration of $2.75B in cash. The acquisition strengthens Altria’s alternative products portfolio and generates a new source of revenue growth. The deal comes only days after Altria said that it ended a deal with e-cigarette maker Juul Labs and swapped its equity investment in the company for a licensing deal. The announcement of the NJOY strategic acquisition also comes about one and a half months after the tobacco company announced a $1 billion share buyback to support the company’s stock price. Shares of Altria currently pay an 8% dividend yield and the stock is still trading cheaply!

Altria is ending its Juul Labs investment and buying e-vapor company NJOY

Altria invested $12.8B in e-cigarette maker Juul Labs in 2018 in exchange for a 35% stake. Altria purchased Juul Labs in a bid to grow its alternative products category which promised growth in a market that suffered from a decline in smokers and shifting consumer preferences. Due to legal challenges the tobacco company was forced to write down the value of its investment to just $250M at the end of FY 2022, in part because the Food and Drug administration threatened to ban Juul Labs’ e-cigarettes from the US market. For this reason, Altria wrote down the value of its equity investment by $1.5B in FY 2022.

Source: Altria

Days ago, Altria announced that it is ending its deal with Juul Labs and that it will exchange its equity stake in the e-cigarette company for a “non-exclusive, irrevocable global license to certain of JUUL’s heated tobacco intellectual property”. By doing this, Altria effectively closes the chapter on its investment in the e-cigarette maker which caused the tobacco company to lose billions of dollars without much to show for it. Altria wrote down the total value of its $12.8B Juul Labs investment by 98%.

On March 6, 2023, Altria announced the acquisition of NJOY, an e-vapor company, which secured approval for its pod-based vaping device, the ACE Pod, from the Food and Drug Administration last year. According to the definitive agreement signed by Altria, the tobacco company is going to pay $2.75B in cash for NJOY which will strengthen Altria’s alternative product portfolio.

Shifting consumer preferences and a long term decline in the share of smokers are forcing companies like Altria to invest more heavily in product innovations, such as nicotine pouches or vapor products, or acquire companies that have built their own product portfolios in niche segments. With adoption of vapor products growing, companies like Altria can harness new sources of revenue growth. This is especially important because tobacco companies continue to experience top line pressure as less people smoke. Altria is expected to see only 1-2% revenue growth in each of the next two years.

Source: Seeking Alpha

With growth in the traditional tobacco market challenged, e-vapor offers an opportunity for growth. The e-vapor market in the US is growing rapidly due to strong customer adoption, especially of the younger demographic. According to Altria, there are 13.7M adult tobacco customers that are using vape products also. Retail sales are growing and reached $7B in FY 2023. Altria faces a clear growth and penetration opportunity in the US vapor market and it could result in shares revaluing higher in the longer term.

Source: Altria

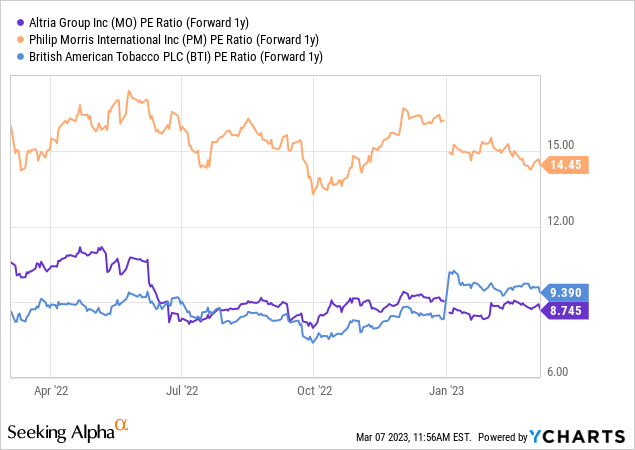

Altria’s valuation vs. rivals

A top reason to buy Altria’s shares is that the company’s earnings potential is still very cheap. Altria’s shares are currently selling for 8.7 X forward earnings which compares to a forward earnings multiplier factor of 9.4 X for British American Tobacco (BTI) which I also like. Philip Morris International (PM) is trading at a P/E ratio of 14.4 X and is too expensive for me to consider.

Altria’s dividend yield of 8% is also covered by adjusted earnings, which I indicated in my last work on the tobacco company, and I estimate that management will raise the dividend by $0.02-0.04 per-share in the third-quarter.

Risks with Altria

Altria’s risks, as they relate to NJOY, are very limited, in my opinion. NJOY’s core product, ACE Pods, has already been approved by the FDA and is already selling in the market. Additionally, Altria can afford to pay $2.75B for a new source of growth since Altria had $4.0B in cash on its balance sheet at the end of FY 2022. The biggest commercial risk for Altria, in my mind, is that the regulatory landscape will continue to tighten. Litigation, advertising restrictions and a continual decline in the share of smokers are risks as well.

Final thoughts

Altria is going on the offensive again. Ending the deal with Juul Labs and acquiring NJOY allows Altria to close an unfortunate chapter in its history and move forward boldly… with a newly acquired alternative product portfolio that can help Altria reinvigorate its revenue growth. The e-vapor market is growing and represents an attractive growth opportunity for the tobacco company. I believe Altria’s low valuation based off of earnings, 8% dividend yield, $1.0B stock buyback and the new NJOY acquisition are strong reasons to buy MO.