AltaGas Series B And H Preferred: Potential To Deliver Outsized Returns (TSX:ALA.PRB:CA)

deepblue4you

***All figures in CAD as that is the company’s reporting currency unless otherwise noted.

Introduction

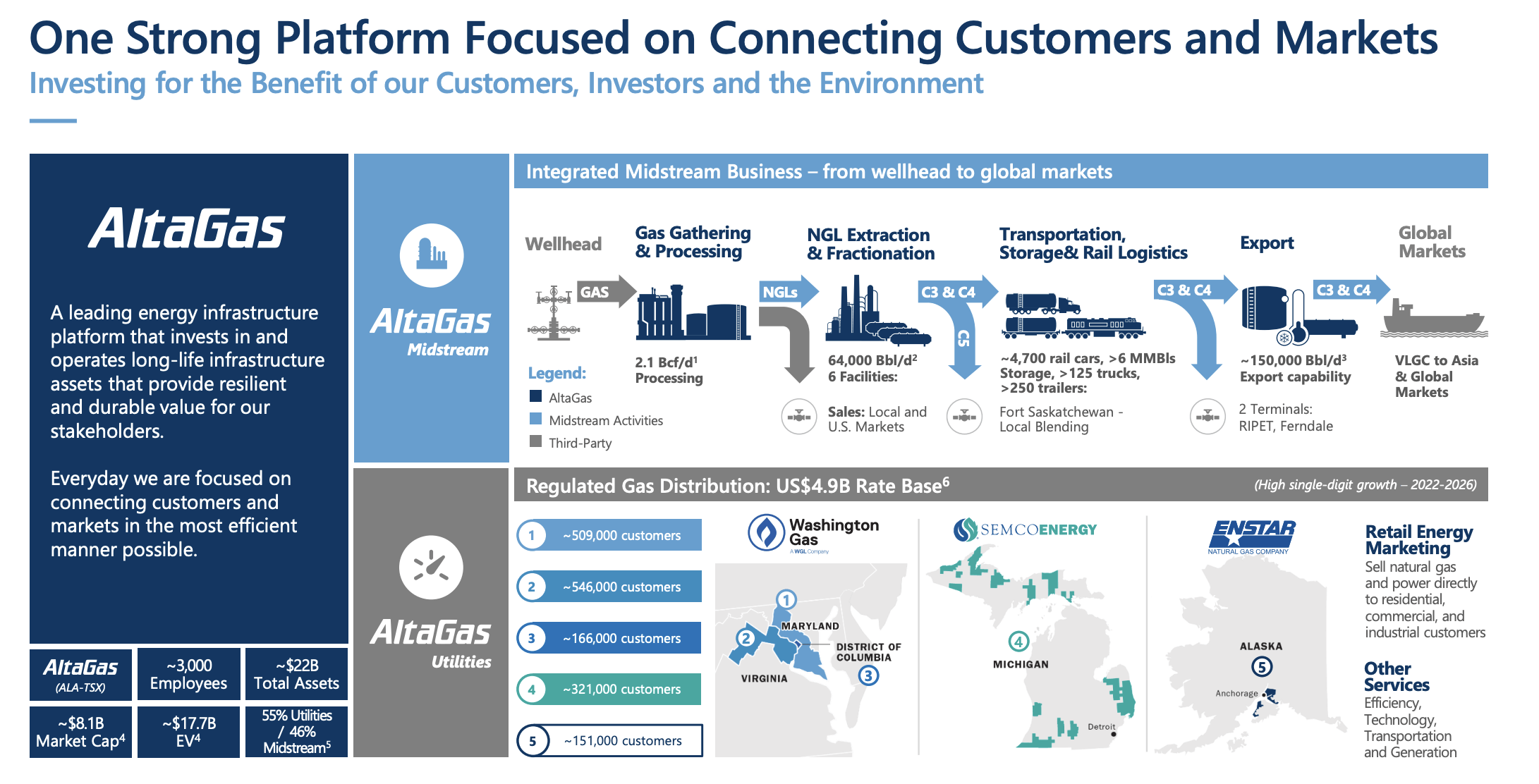

AltaGas (TSX:ALA:CA) is a leading North American energy infrastructure company that connects natural gas and natural gas liquids (NGLs) to domestic and global markets. ALA’s owns utility and midstream assets in Canada and the USA.

ALA’s utilities segment owns and operates franchised, cost-of-service, rate-regulated natural gas distribution and storage utilities. There are four utility operations, two of which are pending sale and operate across five major U.S. jurisdictions.

The operations include:

- Washington Gas, which is the Company’s largest operating utility operation, that serves approximately 1.2 Million customers across Maryland, Virginia, and the District of Columbia.

- SEMCO Energy, which delivers essential energy to approximately 321,000 customers in Southern Michigan and Michigan’s Upper Peninsula.

- ENSTAR, which is pending sale, is the largest gas utility in Alaska and delivers energy to approximately 151,000 customers in Greater Anchorage and the surrounding Cook Inlet region.

- Cook Inlet Natural Gas Storage Alaska (CINGSA), which is pending sale, is a regulated storage utility that provides reliable access to natural gas.

ALA’s Midstream segment is heavily focused on the Montney resource play in Northeastern B.C. and focuses on global exports, which is where they believe the market is headed for resource development over the long-term. ALA also operates midstream infrastructure assets across the Western Canadian Sedimentary Basin (WCSB) and some regions in the U.S.

These operations include:

- Global Exports, which includes AltaGas’ two LPG export terminals where ALA has capacity to export up to 150,000 Bbl/d of propane and butane to key markets in Asia.

- Natural Gas Gathering and Extraction, which includes 1.2 Bcf/d of extraction processing capacity and approximately 1.2 Bcf/d of raw field gas processing capacity, which is heavily focused on the Montney.

- Fractionation and Liquids Handling platform, which includes 65 MBbl/d of fractionation capacity and a sizable liquids handling footprint that operates under the AltaGas and Petrogas banners.

September 2022 Investor Presentation (AltaGas)

55% of EBITDA is generated from the utilities segment and 46% is from the midstream segment. Approximately 70% of their EBITDA is generated from utilities or take-or-pay contracts and 96% of EBITDA is generated from utility and investment grade counter parties which provides tremendous cash flow stability.

September 2022 Investor Presentation (AltaGas)

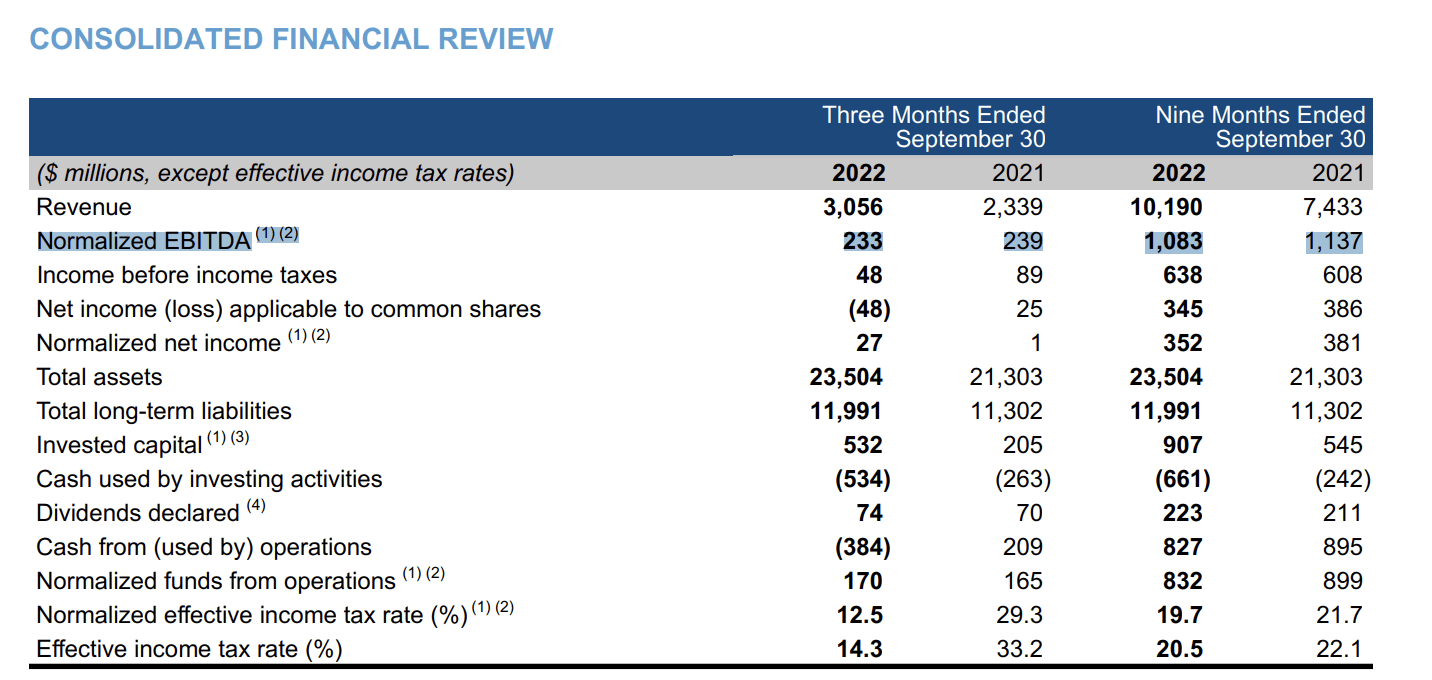

Q3 2022 Results and Outlook

Normalized EBITDA for the first nine months of 2022 was $1,083 Million, compared to $1,137 Million for the same period in 2021, so results were consistent YoY. EBITDA was driven by asset optimization activities at Washington Gas, strong gas margins in WGL’s Retail Marketing business, continued ongoing capital investments that AltaGas has made across the network through Accelerated Replacement Programs (ARPs), and favorable foreign exchange movements. ALA has continued to upgrade critical infrastructure with the deployment of $234 Million, $123 Million of which on the various ARPs and is up 84% from the previous year. The strong utilities performance has not been able to offset the lagging midstream segment, however. Although liquids volumes were strong, this was more than offset by lower realized Asian-to Canadian butane spreads, high commodity price volatility, and higher rail and ocean freight costs (including fuel surcharges). Revenue was also impacted by the sale of ALA’s interest in the Aitken Creek processing facilities in the second quarter of 2022. For fiscal 2022, AltaGas expects to achieve annual consolidated normalized EBITDA of approximately $1.50 to $1.55 Billion compared to normalized EBITDA of $1.49 Billion in 2021.

Q3 2022 MD&A (AltaGas)

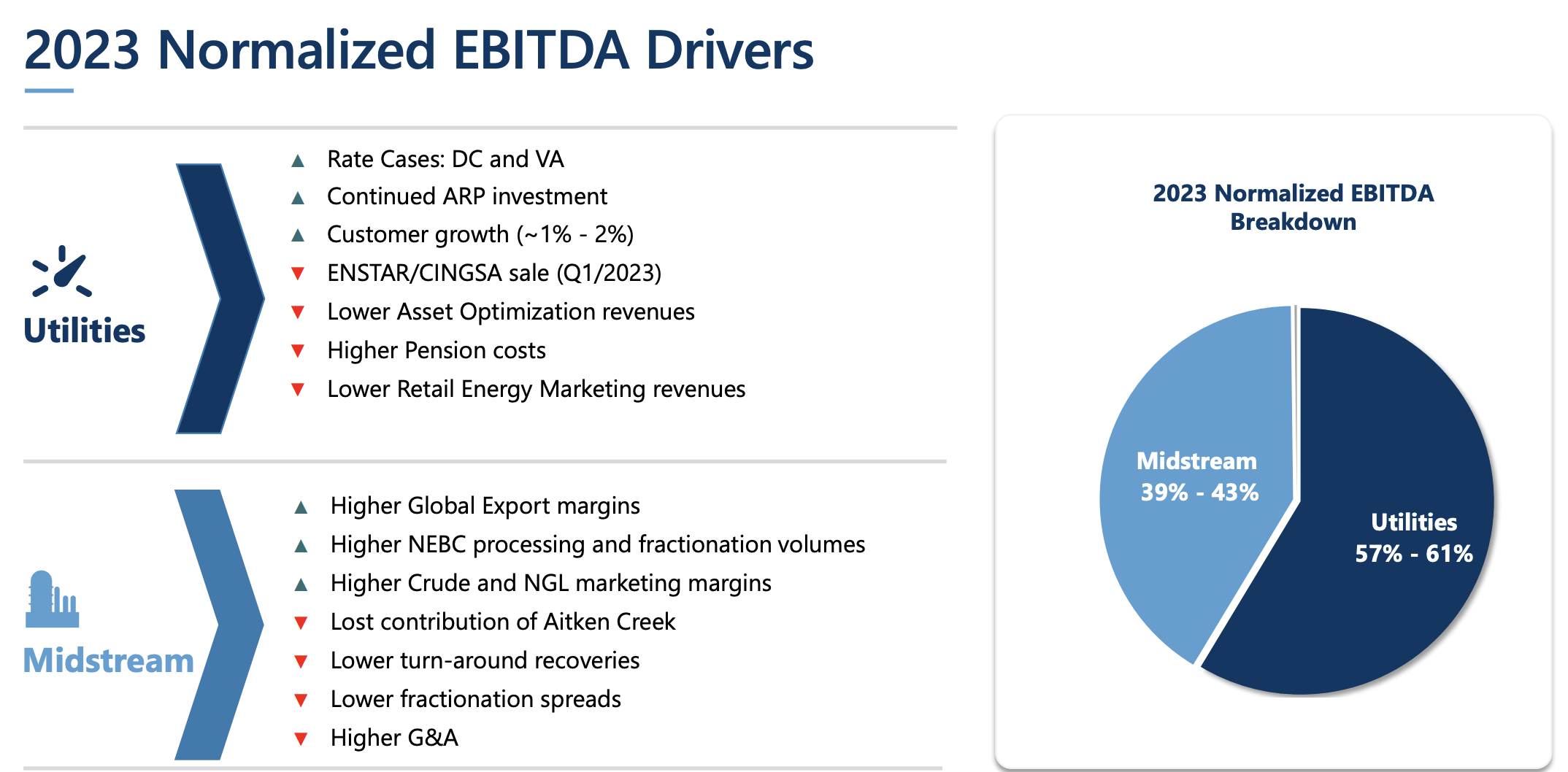

For 2022 and 2023 the utilities segment is expected to contribute up to 60% of EBITDA, with growth driven primarily from revenue from rate cases settled in 2021, increased spending on accelerated capital programs, ongoing commodity and cost optimization activities, improved retail margins and the discontinuation of COVID-19 related moratoriums implemented in 2022. Normalized EBITDA for 2023 in the midstream segment is expected to benefit from the efforts to mitigate and reduce contingent liabilities acquired in the Petrogas acquisition which was fully acquired in July 2022. The acquisition of Petrogas provides ALA the ability to further optimize their west coast LPG export platform and improves their position as a leading provider of North American Liquified Petroleum Gas from the west coast.

2023 Financial Outlook and Guidance (AltaGas)

2023 Financial Outlook and Guidance (AltaGas)

The company has traded at a lower valuation than most of its utility/midstream peers as it has had a tendency to run leverage a little high as even now it’s at 6.14x Net Debt to EBITDA. The sale of the Alaskan Utilities segment will to TriSummit Utilities Inc. that was announced on May 26, 2022, for US$800 Million (approximately CAD$1.1 Billion) will deleverage them to 5.6x which will allow them to reach their target of 4.5-5x by 2023 FYE. AltaGas continues its progress to gain all State and Federal approvals to close the divestiture and expects the transaction to close during the first quarter of 2023.

Investment Thesis

I am still bullish on the prospects of the common shares of ALA as they have even announced a 6% increase to the quarterly dividend which will be $1.12/share annualized and will work out to a ~4.7% dividend yield. This yield is well covered by cash flows.

Given the extreme market uncertainty we are facing and with $2.7 Million in debt coming due before 2026 in a rising interest rate environment why settle for a riskier ~4.7% yield when you can get a less risky 6% or even 9% yield with exposure to ALA.

2023 Financial Outlook and Guidance (AltaGas)

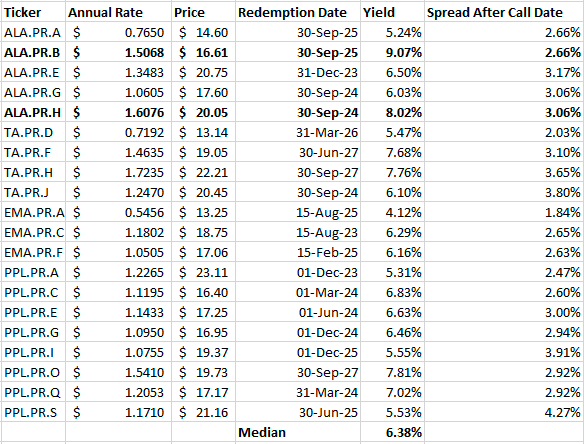

ALA has 5 sets of preferred shares the Series A, B (TSX:ALA.PRB:CA), E, G (ALA.PRG:CA), and H. All issues are cumulative and redeemable every five years at par value of $25/share. If the company chooses not to redeem the rate resets to a new fixed rate at the prevailing 5-year Canada Bond Rate plus a spread outlined in the prospectus.

Q3 2022 MD&A (AltaGas)

The Series B and H have the highest current yields at 9.07% and 8.02% respectively and trade at a price of $16.61/share and $20.05/share, respectively. The Series B is not redeemable until September 2025 and the Series H is not redeemable until September 2024. Both issues have 20%+ Yields to Call, with the Series H more likely to get called given its high spread at 3.06% which would mean ALA would have to payout at least 6.5% interest if today’s rates persist. The rates of these two issues reset every quarters, but given the hawkishness of the BoC the yield is only likely to go up in coming quarters. It is perplexing that the Series H issue has a 294 bps spread over the Series G considering it has the same call date and the Series B has a 383 bps spread over the Series A as those two issues have the same call date as well. Be rest assured that the Series G does have a convertible option to convert to Series H and the Series A is convertible into Series B.

I have expanded the analysis to include utility/midstream peers with similar credit ratings to that of ALA. The preferred shares I have included are from utility and midstream operators like ALA whose debt is rated at either lower investment grade or upper speculative so essentially within one notch of ALA’s ratings. I have only analyzed cumulative redeemable fixed rate preferred shares of the peers and who have similar rate reset features.

| Company | Ticker | Ratings Agency | |||

|---|---|---|---|---|---|

| S&P | Fitch | Moody’s | DBRS | ||

| AltaGas | (ALA:CA) | BBB- (stable) | BBB-(stable) | ||

| TransAlta | (TA:CA) | BB+ | Ba1 | BBB (stable) | |

| Emera Incorporated | (EMA:CA) | BBB (stable) | BBB (stable) | Baa3 (stable) | |

| Pembina Pipeline | (PPL:CA) | BBB (stable) | BBB (stable) |

As we can see below the Series B still has the highest yield of all preferred shares in the sample and the Series h has the second highest. What is perplexing is that S&P and Moody’s don’t even consider TA’s debt investment grade and all of their preferred share issuances have yields below ALA.PR.H and ALA.PR.B. The only other option that comes close to these two in its attractiveness is the PPL.PR.O with a 7.81% yield and has five years to its next call date as it was recently reset at a higher than usual Bank of Canada rate. ALA.PR.H also has the third highest spread at the next reset of all of these preferred share issuances. The two preferred share issuances with the highest spread resets don’t reset until well into 2025, however.

Preferred Share Yields (Author’s Table)

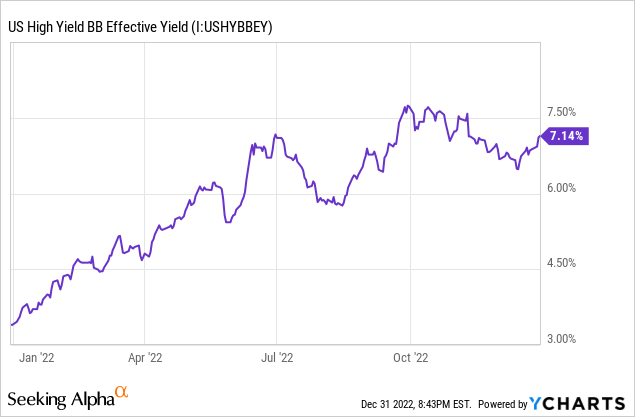

For perspective, the US High Yield BB Effective Yield is 7.14% and is 76 bps above the median in the sample. Assuming even a one notch downgrade from BBB to BB is fair for the preferred shares of ALA would imply a fair value of at least par for the Series H and $21/share for the Series B.

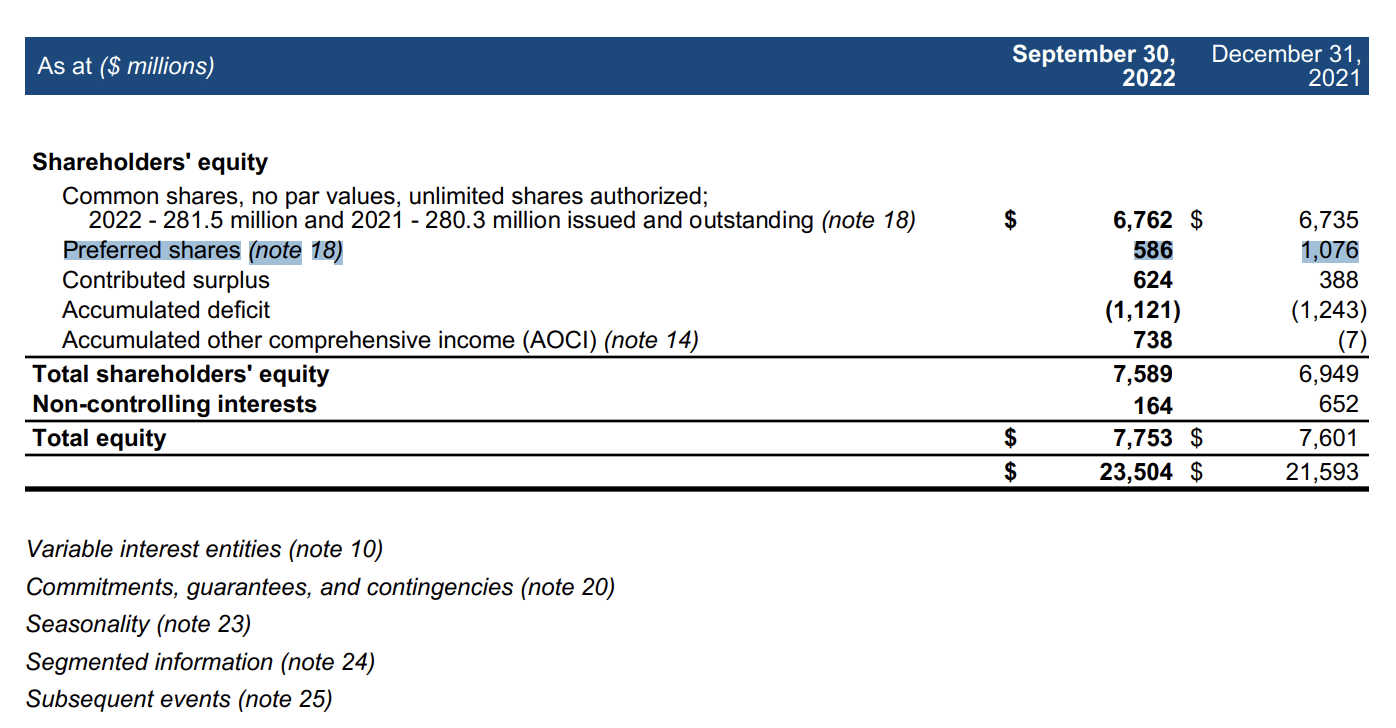

Looking at the Q3 2022 Balance Sheet below, preferred equity only accounts for 7.7% of total equity. Preferred dividends payments only accounted for $40 Million in fiscal 2021 so will be well covered by $1.5 Million in EBITDA for fiscal 2022 and 2023.

Q3 2022 Financial Report (AltaGas)

Conclusion

As we can see the market is not always efficient and has presented an opportunity to generate outsized returns on the Series B and H preferred shares of ALA as these are quite undervalued relative to the fixed rate preferred issues of ALA and all preferred share issuances of EMA, PPL, and TA.

I expect upside of at least 20% on these issues while an 8-9% yield can be pocketed.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.