Wharf Real Estate Investment Company Limited: Buy The Rebound (OTCMKTS:WHREY)

Serjio74

Wharf Real Estate Investment Company Limited (OTCPK:WHREY) is an investment holding company based in Hong Kong. It owns and operates several high-quality retail, offices, a hotel, and the Star Ferry in Hong Kong, along with 2 prime retail shopping centers in Singapore. WHREY is one of the largest real estate companies in Hong Kong.

Hong Kong has been battered by Covid restrictions for the last 3 years. The Hong Kong government is looking to revitalize the city and bring tourists back. I believe this is a catalyst for growth at WHREY and its stock price will end on a higher price.

Singapore’s Tourism is Rebounding/Hong Kong’s Tourism is a Work in Progress

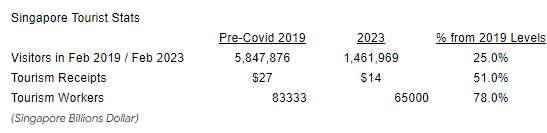

In Singapore, the tourism industry is still recovering. The end of 2022 showed tourism is still a fraction of what it was in 2019:

Singapore Tourism Data (Singapore Tourism Data)

However, recent tourism levels in Singapore have already surpassed initial projections. The retail rents in Singapore’s prime shopping belt had seen a 7.4% year over year increase to $39.20 (the largest increase in 2022). These are signs Singapore’s tourism is on a clear path to recovery and a recent report, by the Singapore Tourism Board, expects tourism to return to pre-pandemic levels by 2024.

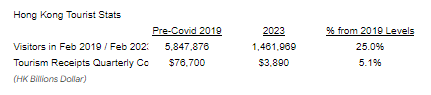

The Hong Kong tourism industry is a different story. It was only few months ago when Hong Kong dropped its social distancing measures and lifted restrictions for new travelers to the city. Tourists only started returning to the city early this year. Compared to Singapore, Hong Kong tourism still has some ways to go before it can return to pre-pandemic levels:

Hong Kong Tourism Data (Hong Kong Tourism Board)

To boost new tourists to the city, the Hong Kong government had launched a $255 million HKD tourism campaign. Some of the incentives include 500,000 free plane tickets to the city, and Gift vouchers for tourists.

There are signs tourism is rebounding in Hong Kong. In February 2023, it was reported that the number of new tourists coming into the city had finally surpassed more than a million for the first time since the pandemic.

WHREY’s Property Portfolio is Skewed Towards Retail and Tourism

WHREY owns a number of Class A retail, commercial, a hotel and various other assets in Hong Kong. Along with 2 retail complexes in Singapore:

WHREY Property Profile (WHREY Property Description)

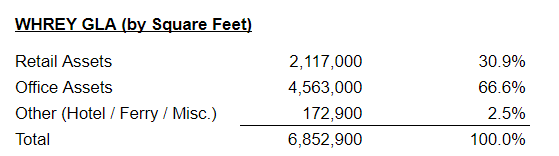

On a portfolio square footage basis, most of gross leasable area is predominantly office:

WHREY Portfolio GLA (WHREY Website)

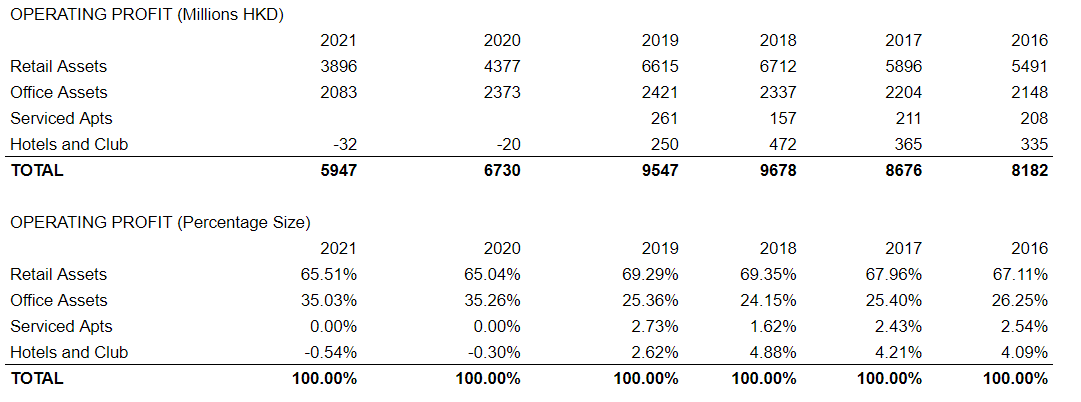

In looking at the operating profit, most of its bottom line is driven retail assets:

WHREY Operating Profit (WHREY Financials)

Before the pandemic, retail profits made up almost 70% of WHREY’s profits and serviced apartments, hotels, and clubs made up approximately 5%. The pandemic and the loss of tourism deeply impacted WHREY’s bottom line as almost half of the retail profits were wiped out in year ending 2021 compared to 2019 ($3,896 million in 2021 vs $6,615 million in 2019).

One bright area is despite work from home procedures in Hong Kong and some offices were forced to shut down, commercial profits continued to be resilient all through the pandemic. Commercial profits trended around $2,000 million HKD in the last 5 years.

In summary, commercial square footage makes up a large piece of WHREY’s portfolio but it is retail that is the main profit driver. Therefore, tourism and a retail rebound is a big factor to WHREY’s profitability. As long as tourism levels return to pre-pandemic levels in Hong Kong and Singapore then WHREY’s stock price will likely rebound as well.

WHREY Has A Healthy Balance Sheet Despite the Drop in Earnings

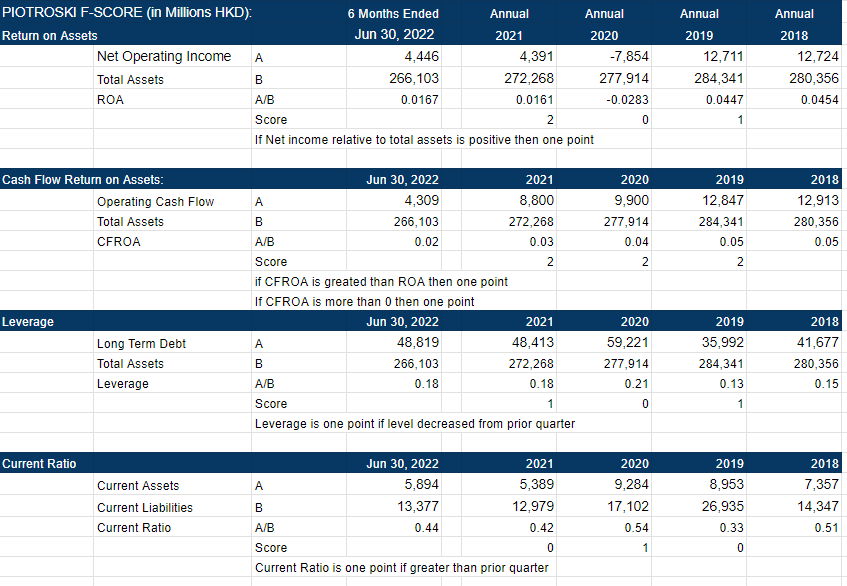

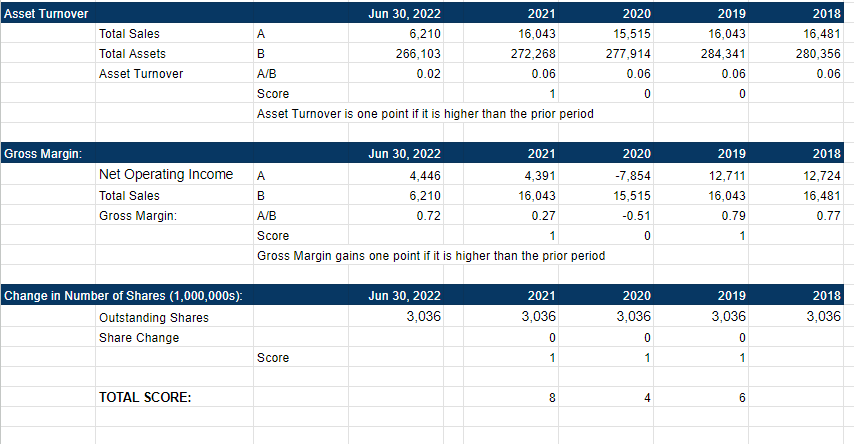

WHREY’s balance sheet has been healthy with little debt. Its F-Score in year ending 2021 was an 8. The F-Score measures the company’s financial health. A score of 9 conveys the company is financially strong and a score of 0 shows the company is financially weak:

WHREY F Score (WHREY Website) WHREY F Score (WHREY Website)

WHREY’s debt to equity ratio remains below 0.2 and its current liabilities has been in the 0.45 to 0.55 range. From a cash position stand point, WHREY didn’t have a need to raise debt during the pandemic. Its profitability metrics may have fallen (gross margin was down and return on assets was negative), but its 6 months ending June 2022 shows some of these profit indicators have rebounded. Its gross margin was 0.72.

WHREY has the capital to weather any storm. So I’m confident WHREY has the time to wait this out if it needs to.

It should be noted that since 2022 year end financials are not released yet, it is hard to determine whether the balance sheet and income statements have improved from June 30, 2022.

Conclusion: Bullish on WHREY

WHREY has a lot of potential in 2023. The tourists are returning to both cities, Hong Kong and Singapore. Even if the tourist numbers take a while to normalize, WHREY has the balance sheet and cash to weather further shocks to its company.

Retail revenue has fluctuated a lot in the past few years, which leads me to believe some of the leases signed with retail tenants must be based on percentage of sales. That means WHREY collects some of its rent based on how much sales its retail tenant does in a particular month. A good sales month means a better bottom line for WHREY. This is why WHREY needs the tourists to come back to Hong Kong and Singapore.

The good news is tourists came back in droves in Hong Kong for the month of Feb 2023. I anticipate tourist numbers to continue to increase for the remaining year. The bad news is economic uncertainty appears to be high. There has been speculation that recession is just around the corner. This could dampen consumer’s appetite to travel.

Nevertheless, WHREY is in a good position today, and I’m willing to make a bet WHREY will perform well this year. I’m bullish on WHREY.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.