WDI CEF: Discount Attractive, Distribution Covered With More Bumps

Darren415

Written by Nick Ackerman, co-produced by Stanford Chemist. A version of this article was originally published to members of the CEF/ETF Income Laboratory on March 13th, 2023.

Despite all the commotion going on lately with bank failures, there are still some places investors can put capital to work. Risk-free ways to earn money have become relatively more attractive in the last year, but there are still some options for investors that can handle more volatility and risk. That includes Western Asset Diversified Income Fund (NYSE:WDI). I believe WDI presents an attractive distribution yield that’s been fully covered, and it looks set to continue to be fully covered. The discount has narrowed a bit but remains attractive as well.

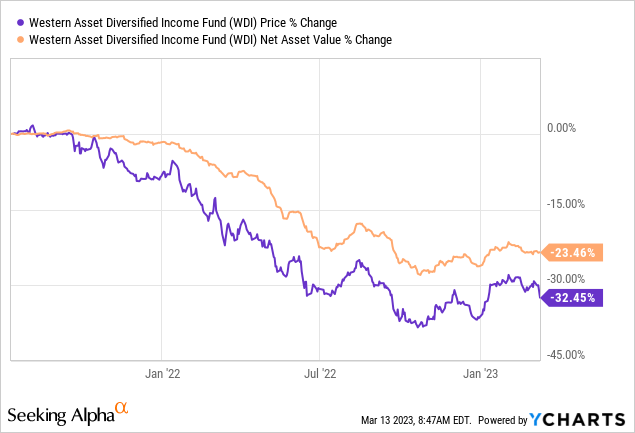

With strong distribution coverage, we’ve seen another increase in their distribution. The last time we touched on this fund, they had increased their distribution around that time as well. In fact, they’ve bumped it up by a small amount twice since then. The performance has been doing well since our last update, and the fund still produced positive total returns, but the latest volatility has sent the share price lower.

WDI Performance Since Prior Update (Seeking Alpha)

The Basics

- 1-Year Z-score: 0.04

- Discount: 11.70%

- Distribution Yield: 11.37%

- Expense Ratio: 1.48%

- Leverage: 30.55%

- Managed Assets: $1.17 billion

- Structure: Term (anticipated liquidation date, June 24th, 2033)

WDI’s objective is “to seek high current income. As a secondary investment objective, the fund will seek capital appreciation.” They will bring a “flexible and dynamic” approach. They anticipate doing this by rotating sectors and securities in response to market conditions, focusing on what we believe are undervalued securities with attractive fundamentals.

For greater flexibility, they have no restrictions on investing in investment-grade or below investment grade. Meaning that they will span the credit quality spectrum, leading to a truly multi-sector bond fund with limited constraints. This can be a positive if they can successfully manage it. It leaves investors a bit more in the dark and more reliant on the management team to operate the fund.

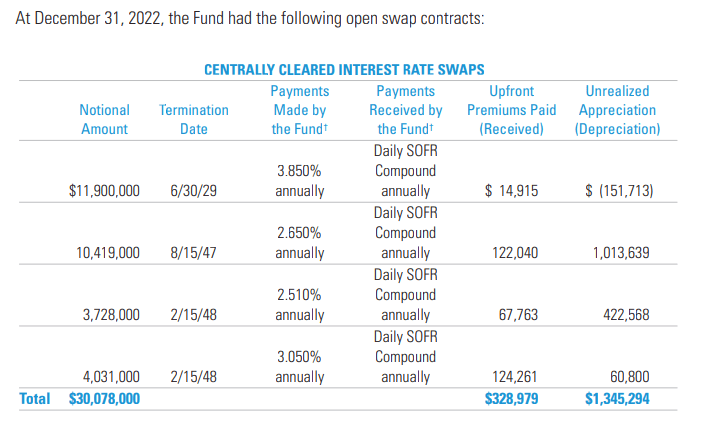

The fund’s total expense ratio goes up to 1.82% when including interest rate expenses. With rising interest rates, they’ve also been hit with higher leverage costs on their borrowings, plus reverse repurchase agreements are getting more expensive. However, WDI has hedged some of its interest rate risks through interest rate swaps.

WDI Interest Rate Swaps (Western Asset)

Though notably, this is only a portion that’s being covered through these swaps, not their entire leverage. That’s where the fund’s floating rate debt exposure can also help negate the negatives of higher interest rates.

Performance – Ugly Chart, Attractive Discount

Similar to most fixed-income funds, their price charts have become quite ugly, but that, for the most part, hasn’t impacted the income generation of the funds. With leverage, we have additional risks of amplifying results to the downside when things start going lower. Results since the fund’s inception have made this risk pretty evident.

WDI Annualized Performance (Western Asset)

That also means deleveraging can take place, which impacts the portfolio’s income generation. WDI has avoided deleveraging. While loans outstanding have come down, they’ve replaced that with reverse repurchase agreements to fill the gap.

YCharts

Still, that can be little comfort for investors as the fund’s share price and NAV have only gone in one direction since its inception. Of course, it depends on when you bought the fund; if you invested since the beginning, your results would be about as bad as they can be. If you were buying last fall or even in the summer of 2022, your results are much different. Given the decline in the fund’s share price has outpaced the NAV, some of this has come simply from the discount widening to an attractive level.

A discount can always get wider, but the risk of further downside due to discount expansion becomes more minimal at a certain point. As a newer fund, we don’t really have a range that can be observed yet. This is particularly true when we are in a volatile period, which has basically been the case since the fund’s launch. We’ve gone through a bear market and now looking at bank failures. This fund hasn’t experienced trading in any sort of “normal” market.

Distributions – Fully Covered

The latest distribution of $0.13 per month works out to a distribution yield of 12.03%. On a NAV basis, it works out to 10.46%. A double-digit yield on the NAV previously would be considered a red flag. However, with higher interest rates, this has become much more normal for junk fixed-income funds.

WDI Distribution History (CEFConnect)

The fund initially started with an $0.117 monthly distribution. So the raises here haven’t been massive, but as the fund has been ramped up and invested, it has been heading higher. Some of this is due to the fund’s floating rate exposure.

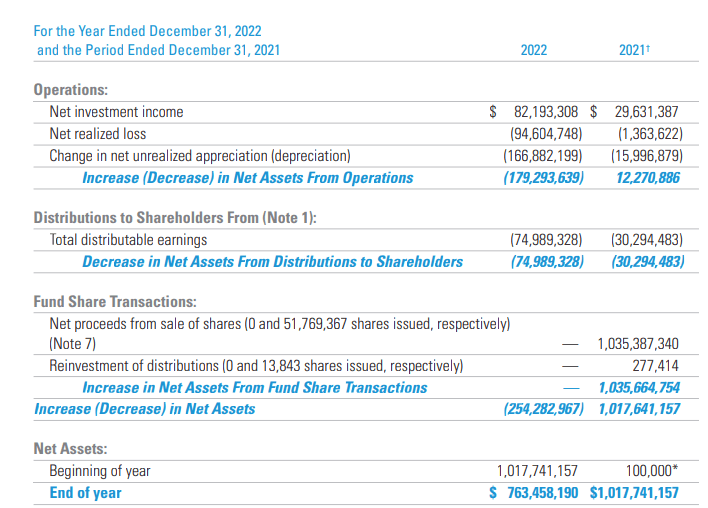

Last year’s net investment income coverage was 109.6%. 2022 was the fund’s first full year, as it launched on June 24th, 2021.

WDI Annual Report (Western Asset)

On a per-share basis, it worked out to $1.59. That should bode well for the distribution going forward. The annualized distribution currently works out to $1.56 with the latest increase. Thus, it appears NII coverage would be around 102% going forward.

For tax purposes, WDI’s distributions were classified as ordinary income in both 2022 and 2021. Since it’s a fixed-income fund, this is naturally the case, and it would suggest holding in a tax-sheltered account would be the most appropriate.

WDI Distribution Tax Classifications (Western Asset)

WDI’s Portfolio

WDI’s portfolio is fairly diversified. They hold 298 positions, but that is much fewer than its benchmark at 2044 holdings. One way to limit risk in below-investment-grade funds is to generally just invest in a highly diversified portfolio. I think that can be achieved through nearly 300 holdings, even if it isn’t thousands of holdings.

While the fund carries some investment-grade debt, it isn’t too material to the portfolio. The portfolio hasn’t shifted its credit weighting to any significant degree since our last update. The CCC rated and below debt continues to be an area that we should focus on, especially as we see signs that the Fed is starting to break things. Leveraged below-investment-grade exposure during uncertain times is why this makes it a more aggressive fund, not for a risk-averse investor.

WDI Credit Quality (Western Asset)

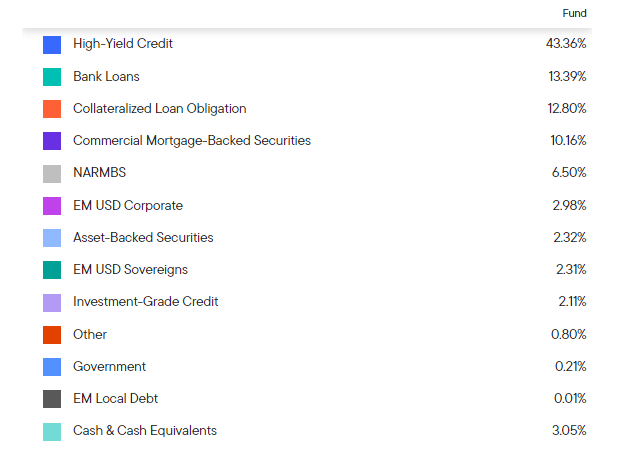

They use the Bloomberg U.S. Corporate High Yield as a benchmark. However, that doesn’t tell us the whole story of WDI’s portfolio since a material amount is invested outside of high-yield bonds alone. That includes bank loans and collateralized loan obligations, which are floating-rate debt investments. Again, despite the 42% portfolio turnover they reported, nothing here is drastically different than the previous allocations when we looked at the fund previously.

WDI Sector Exposure (Western Asset)

It’s those sorts of weightings that help bring the fund’s effective duration down to 4.32 years. Meaning that with every 1% increase in interest rates, we could anticipate around a 4.32% decline in the underlying portfolio.

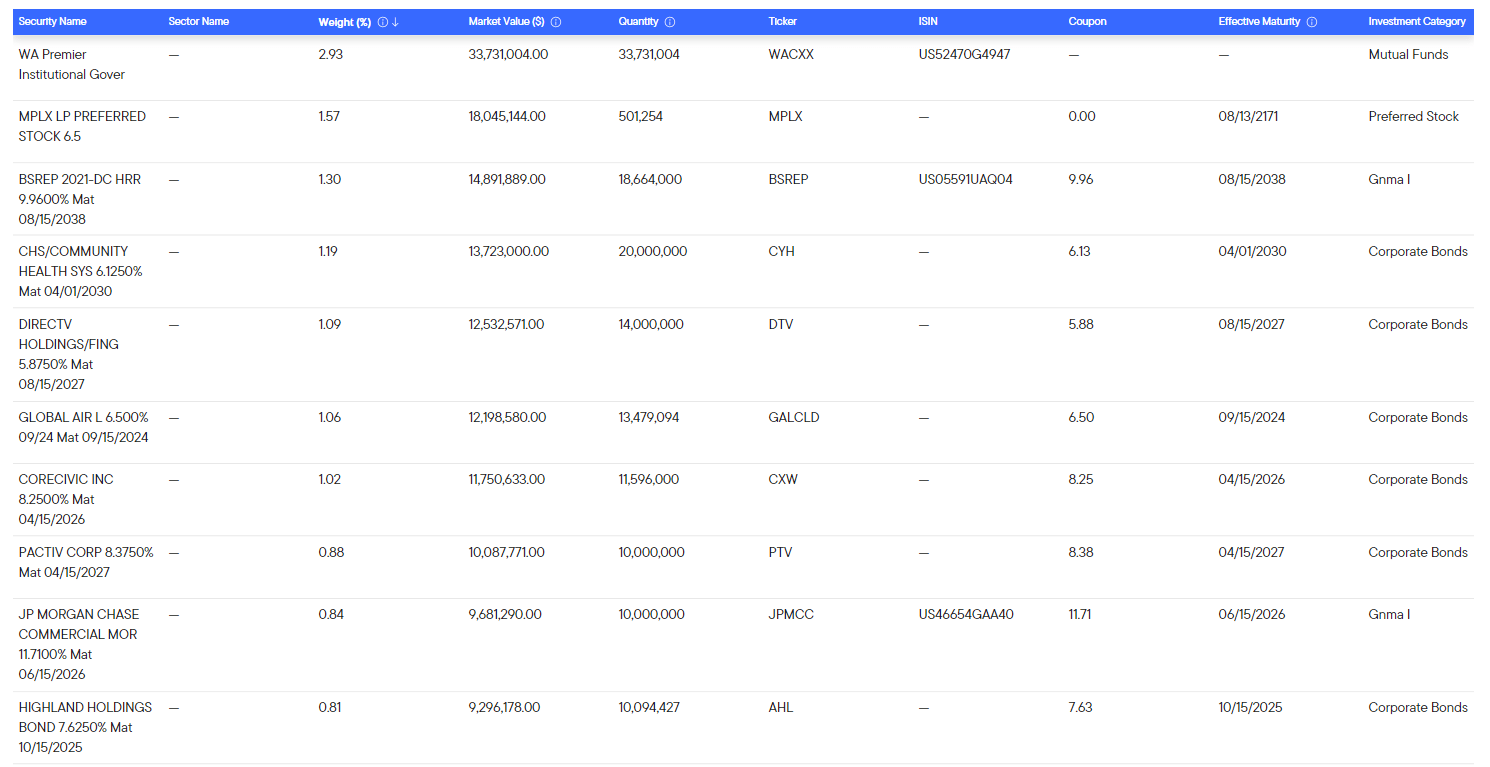

The diversification of the fund is continued and reflected through the holdings; not only do they hold around 300 holdings, but they are actually divided up amongst the holdings. The largest holding is nearly 3%, but that’s a money market fund (WACXX). After that, the position weighting of each holding is fairly minimal, with no single position making an outsized weighting for the fund.

WDI Top Holdings (Western Asset)

While WACXX is essentially a cash position, with a current yield of 4.52% and limited risk, it isn’t necessarily a dead position that cash would have been previously. The MPLX (MPLX) preferred remains their largest position outside of WACXX, which was also previously the case.

Conclusion

WDI’s share price might not be rewarding shareholders since its inception, but they’ve been able to increase its distribution to shareholders despite rising interest rates. In fact, thanks to that floating rate exposure in the fund, it could be seen as a benefit and why we are getting higher distributions. As a leveraged below-investment-grade fund in times of uncertainty, there are clearly risks to consider. However, the larger discount and covered distribution appeal to those who can handle some volatility.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.