Valero Energy Q4 2022 Earnings: Market Outlook And Financial Performance (NYSE:VLO)

Justin Sullivan/Getty Images News

In the past six months, Valero Energy (NYSE:VLO) stock price increased by more than 25% as the company’s cost of sales in the refining segment decreased and its total throughput volumes increased. However, the market outlook for Valero Energy is not as strong as it was in 2022. Due to falling gasoline and diesel fuel prices, I expect VLO’s refining margin to decrease in the first half of 2023. On the other hand, in 2022, the company has been able to improve its leverage ratios. Also, its capital and cash structures show that Valero is financially healthy and even with the current market outlook, can remain profitable, reward its shareholders, and meet its obligations. Last, we covered VLO in October 2022.

Quarterly results

In its 4Q 2022 financial result, VLO reported revenues of $41.7 billion, compared with 3Q 2022 revenues of $44.5 billion. The company’s total cost of sales decreased from $40.4 billion in 3Q 2022 to $37.1 billion in 4Q 2022, driven by the lower cost of materials. VLO reported a 4Q 2022 net income (attributable to Valero Energy stockholders) of $3.1 billion, compared with $2.8 billion in 3Q 2022. The company’s diluted EPS increased from $7.19 in the third quarter of 2022 to $8.15 in the fourth quarter of the year. Valero Energy’s total throughput volumes increased from 3005 thousand barrels per day in 3Q 2021 to 3042 thousand barrels per day in 4Q 2022, driven by higher heavy sour crude oil and sweet crude oil throughput volumes, partially offset by lower medium/light sour crude oil throughput volumes.

Valero Energy’s refining revenues account for more than 90% of the company’s total revenues. VLO’s refining revenues decreased from $42.3 billion in 3Q 2022 to $39.6 billion in 4Q 2022. On the other hand, its cost of sales in the refining segment decreased from $38.5 billion in 3Q 2022 to $35.2 billion in 4Q 2022. VLO’s operating income in the refining segment increased from $3.8 billion in 3Q 2022 to $4.3 billion in 4Q 2022. The company’s total operating income increased from $3.8 billion in 3Q 2022 to $4.3 billion in 4Q 2022. “Our refineries operated at a 97 percent capacity utilization rate in the fourth quarter, which is the highest utilization rate for our system since 2018,” the CEO commented.

The market outlook

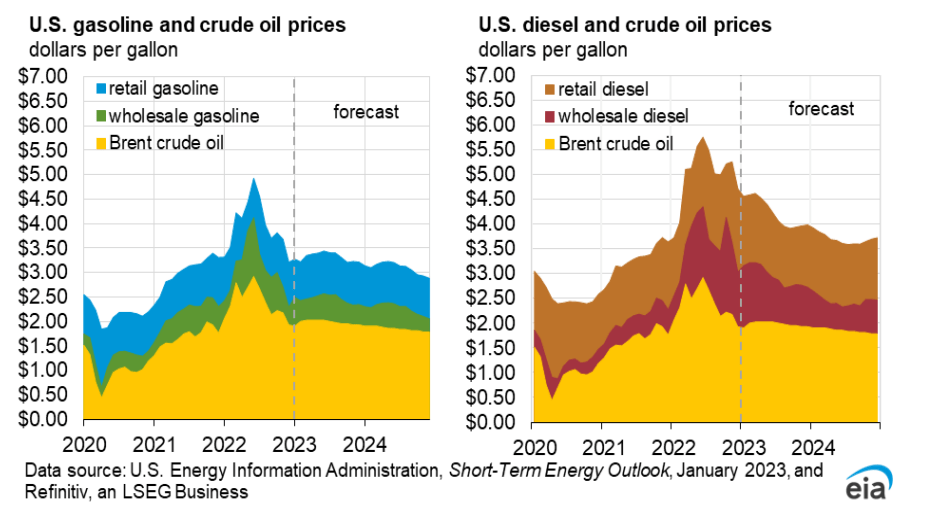

According to EIA’s recent short-term energy outlook, U.S. refining margins for diesel will fall by 20% in 2023 and by 38% in 2024. Diesel fuel price in the fourth quarter of 2022 was $276 per barrel (see Figure 1). EIA expects diesel fuel prices to be $255/b and $237/b in 1Q 2023 and 2Q 2023, respectively. It also expects that retail diesel fuel prices to average $4.20 per gallon in 2023. The company’s U.S. Gulf Coast ultra-low sulfur diesel (ULSD) less Brent crack spread in the fourth quarter of 2022 was 52.78/b. Its U.S. Mid-Continent ULSD less Brent was $59.53/b in 4Q 2022. The company’s North Atlantic ULSD less Brent price was $73.03/b. According to data provided in Figure 1 and Figure 2, the difference between gasoline prices and Brent crude oil prices in the first quarter of 2023 is expected to be lower than in 4Q 2022. However, due to lower crude oil prices and higher gasoline prices in 2Q 2023, the difference between gasoline prices and Brent crude prices is expected to increase in the second quarter of 2023. Also, the difference between diesel fuel prices and Brent crude oil prices in 1Q 2023 is expected to be lower than in 4Q 2022 and due to falling gasoline prices, this difference is expected to decrease further in the second quarter of 2023. It is worth noting that EIA projects almost no change in U.S. gasoline consumption over the next two years. Furthermore, as the war between Russia and Ukraine is still going on and before the war, Russia had been a major supplier of diesel fuel to Europe, gasoline prices will remain lower than diesel fuel prices in 2023.

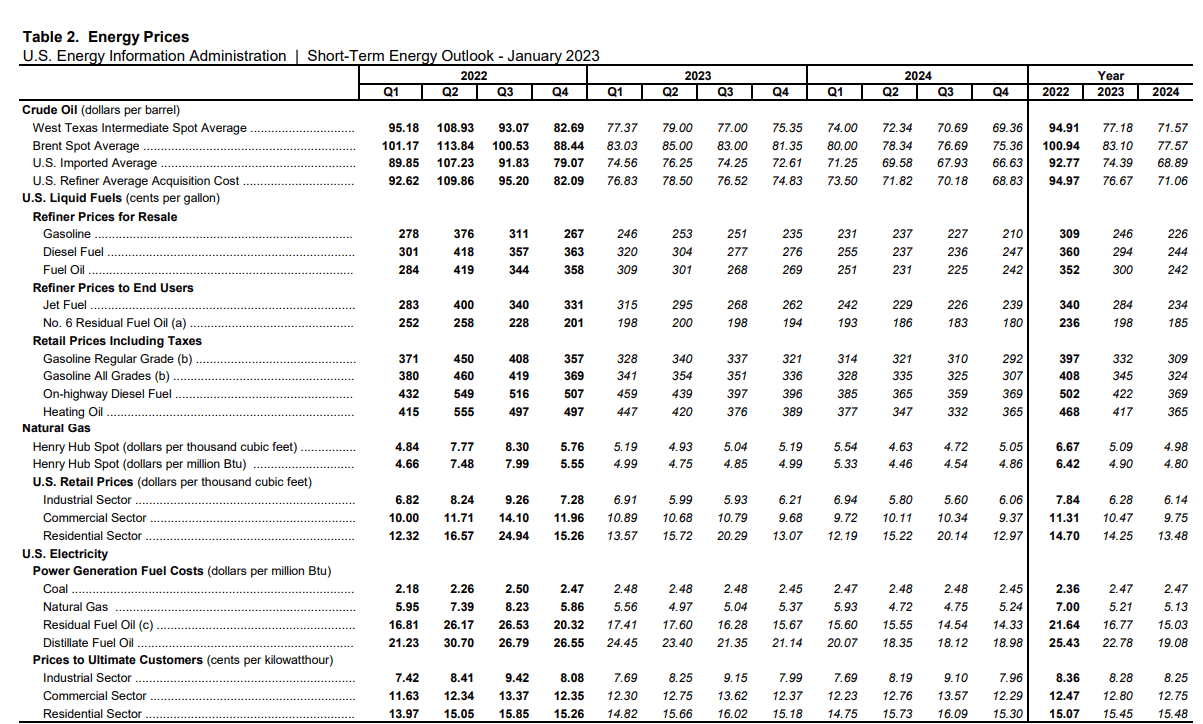

Figure 1 – U.S. energy prices

EIA

Figure 2 – U.S. gasoline, diesel, and crude oil prices

EIA

VLO performance outlook

In the following section, I provided some leverage ratios as well as cash and capital structures to illustrate the credit ratings of Valero Energy Corporation. In the energy sector, one key way for investors to keep an eye on each company’s performance outlook is by considering their debt levels. Since the sector is capital-intensive, high debt levels may lead to a lower ability to purchase new equipment or meet other obligations. Thus, I catered some specific leverage ratios to assess the financial health of an energy company.

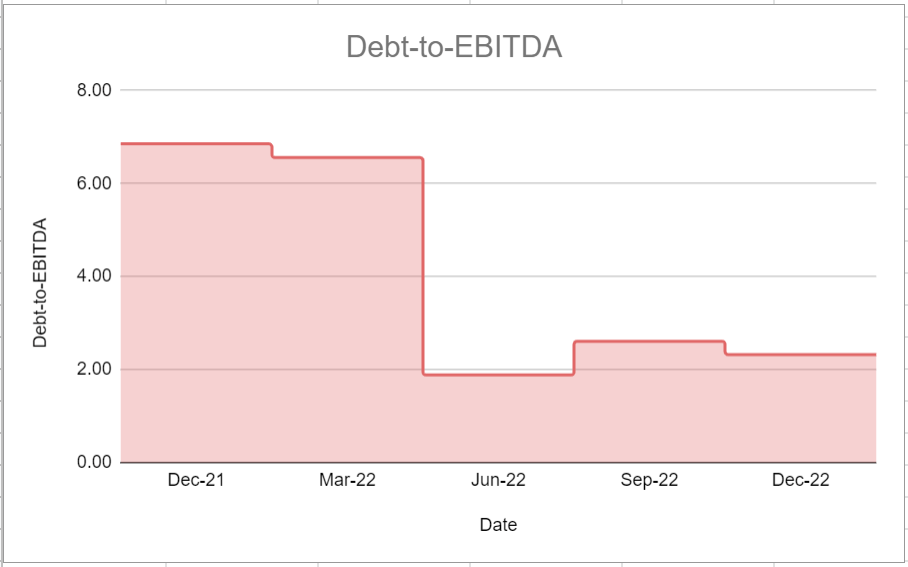

Figure 3 shows VLO’s debt-to-EBITDA ratio during the recent quarters. This ratio determines the probability of defaulting on issued debt, and as energy companies often have a great amount of debt on their balance sheet, this ratio could be of help to determine how many years of EBITDA would be necessary for Valero Energy to be able to pay back its debt. It is observable that the company’s debt-to-EBITDA dropped considerably in the second quarter of 2022. Notwithstanding a slightly increase in the 3Q 2022, it declined to 2.32x in the last quarter of 2022. Overall, Valero Energy’s debt-to-EBITDA in the 4Q 2022 was far lower year-over-year compared with its level of 6.85x at the end of 2021.

Figure 3 – VLO’s debt-to-EBITDA

Author’s calculation

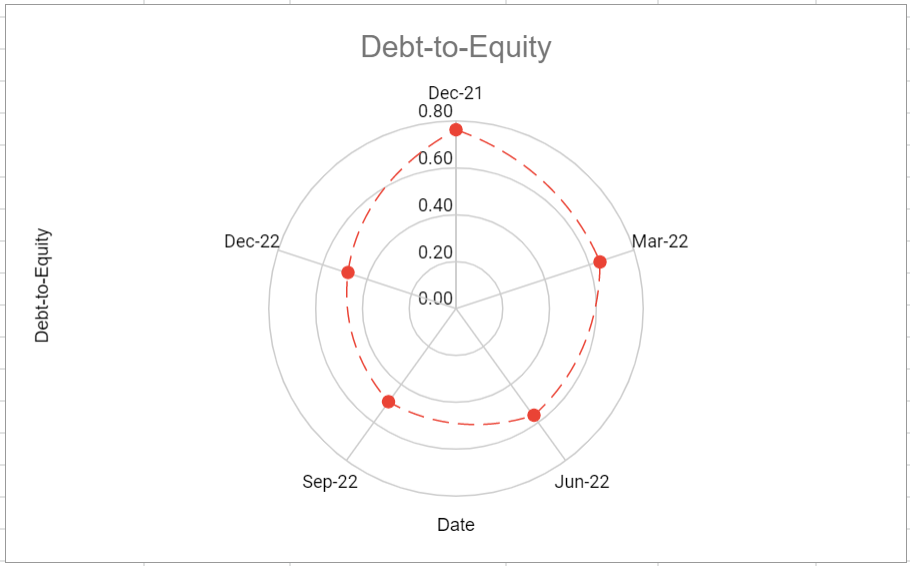

Moreover, Figure 4 is a picture of the company’s debt-equity or risk ratio. The debt-to-equity ratio is a leverage ratio that measures the weight of total debt and financial liabilities compared with total shareholders’ equity. Generally, this ratio determines whether a company’s capital structure is toward debt or equity financing. As it is indicative, during the previous year, VLO had decreasing debt-to-equity amount in every quarter. Finally, it sat at 0.49x in the third and fourth quarter of 2022. Also, the company’s level of risk ratio decreased by 35% year-over-year compared with its amount of 0.76x in the fourth quarter of 2022.

Figure 4 – VLO’s debt-to-equity

Author’s calculations

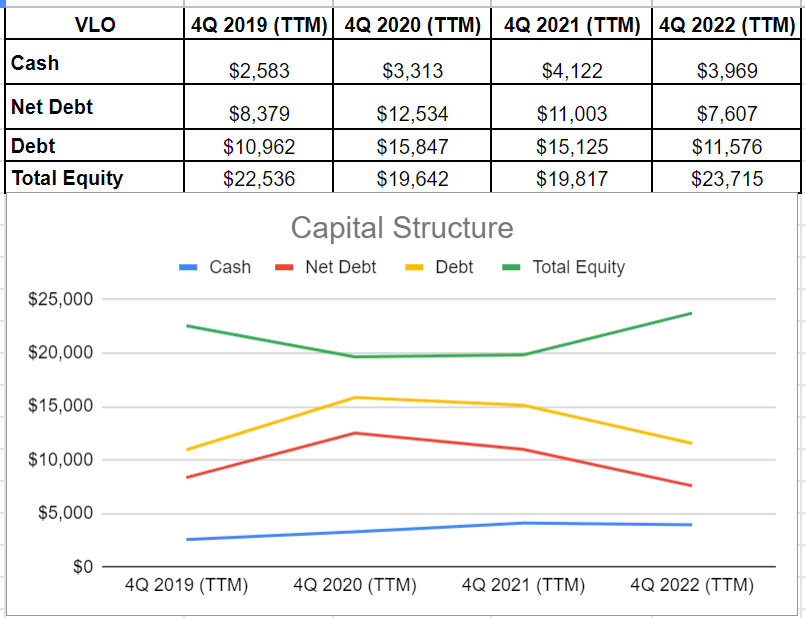

Since the end of 2021, the company’s cash and equivalents decreased roughly by 3% to $3969 million in TTM versus its amount of $4122 million at the end of 2021. The company’s deep drop in its debt amount of $15125 million at the end of 2021 to $11576 million in 2022, combined with cash generation led to a decline in its net debt. In minutiae, VLO’s net debt plunged from $11003 million at the end of 2021 to $7607 million at the end of 2022. Furthermore, VLO’s total equity improved by 19% to $23715 million in 2022 compared with its previous amount of $19817 million at the end of 2021. Thankfully, the company’s net debt and total equity is well enough to tailor a scope of capacity to bring benefits for its shareholders and assimilate upcoming risks. Thus, Valero Energy’s capital structure indicates a healthy position and enables the company to increase its distributions (see Figure 5).

Figure 5 – VLO’s capital structure

Author (SA data)

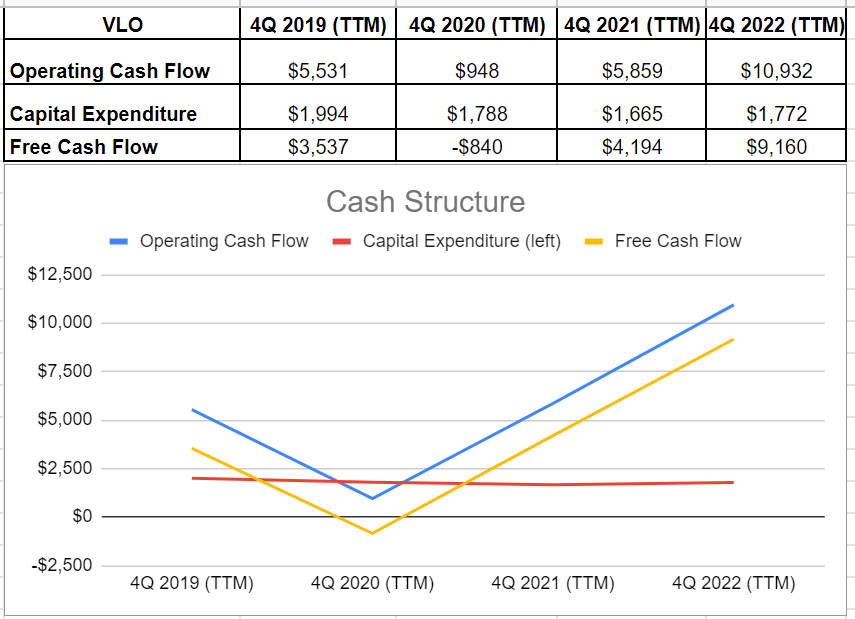

After the downturn of 2020 due to the COVID-19 pandemic, the company has started the recovery process successfully. Its cash operation in 2022 boosted to $10932 million compared with its amount of $5859 million at the end of 2021. Also, Valero Energy’s capital expenditure increased slightly by around 6% to $1772 million in 2022 versus its previous amount of $1665 million at the end of 2021. When all was said and done, the company ultimately generated $9160 million of free cash flow at the end of 2022, which indicates an amazing rise from its previous amount of $4194 million in 2021. This is the highest amount of free cash flow that Valero Energy corporation has had since 2019, which cater a scope of capability for more reliable distributions in the future (see Figure 6).

Figure 6 – VLO’s cash structure

Author (SA data)

Summary

As a result of lower cost of sales, higher throughput volumes, and high refining product prices in the past few quarters, VLO’s free cash flow more than doubled in 2022, and its debt-to-equity ratio and debt-to-EBITDA ratio improved considerably. However, I don’t expect the company’s financial results and ratios in 1Q 2023 to be as strong as in 4Q 2022 as gasoline and diesel fuel prices are falling and the company’s cost of sales are not expected to decrease significantly in the first quarter of 2023. The stock is a hold.