Willamette Valley Vineyards: Back To A Reasonable Entry Point (NASDAQ:WVVI)

Joe Sanzere/iStock via Getty Images

Willamette Valley Vineyards (NASDAQ:WVVI) is a small American winery primarily focused on operations in the Willamette Valley in Oregon. Oregon winegrower Jim Bernau founded what would become Willamette Valley Vineyards in 1983, and it turned into its present corporate form in 1988.

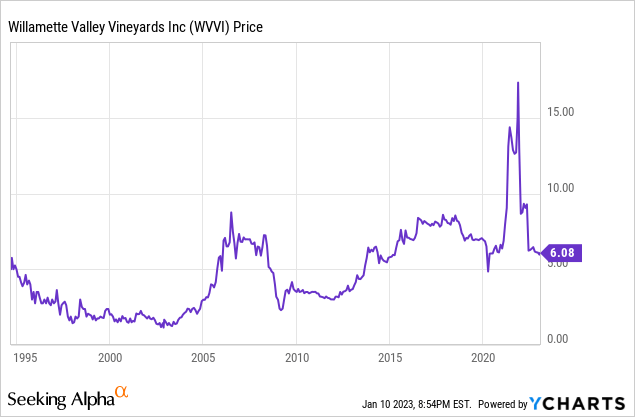

The company would go on to begin trading stock publicly in 1994, with shares starting off at $5. Fast forward 29 years, and the stock is now going for $6 each. The stock has, to put it charitably, not managed to keep up with the S&P 500 over that timespan:

However, I’d argue things aren’t quite as bad as that chart might suggest. While Willamette Valley has historically struggled to generate strong total returns, much of that simply came from shares being dramatically overvalued earlier in the company’s history.

To that point, I’d note that investors were paying as much as four times tangible book value for the company in the 1990s and 2000s. Over the years, Willamette has grown tangible book value considerably, and now shares are at just 0.95x price/tangible book value. In other words, while the stock price has been more or less flat for decades, the company’s actual asset base and revenues have grown considerably, which offer a lot more support for shares today than ten or twenty years ago.

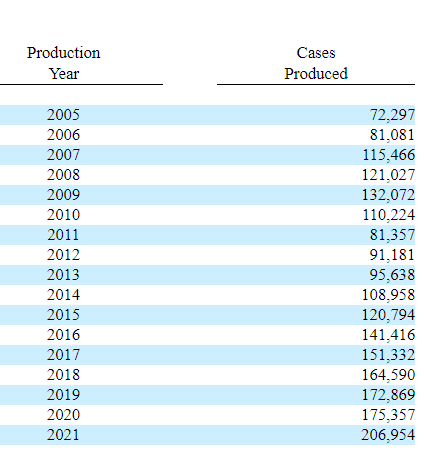

To further make that point, consider this table of wine production from Willamette Valley’s 10-k:

Willamette Valley annual production (10-K)

This shows the number of cases of wine that the company has produced annually dating back to 2005. The company grew production from 72,000 cases to 132,000 in 2009. However, this slumped to less than 100,000 annually in the early 2010s. More recently, however, the company has grown production pretty steadily, with output roughly doubling between 2012 and 2020.

And now, as you can see, Willamette has enjoyed a considerable jump in production, with case output advancing by more than 30,000 in 2021 versus the prior year.

My longest-running complaint with Willamette Valley is that the company is close to being too small to justify the costs of being a publicly traded company. The listing fees, auditing costs, and other compliance and legal expenses of being a publicly traded company are large for a firm that generates just $30 million or so of annual revenues.

If Willamette could, say, double its wine output and resulting sales, however, that would greatly shrink the portion of the firm’s revenues that are getting eaten up simply from overhead. The company has grown wine output dramatically in recent years, and now it is making another big investment push as well, though that has hurt earnings results in the short-run.

Willamette’s Consumer-Focused Growth Strategy

Willamette has long made a point of having a community element to its business. The company offers robust preferred stock shareholder benefits in the form of wine tasting, tours and so on for its shareholders. The firm also makes a point of emphasizing its involvement in the local Oregon community.

To further build upon that local business ethos, Willamette has begun to invest heavily in additional tasting rooms and restaurant locations. This allows Willamette to showcase its wines directly to consumers and hopefully achieve much higher-margin sales than you get from selling through traditional distributors. If Willamette can convert that community interest in the brand into more direct sales, that could be a powerful lever for improving profitability.

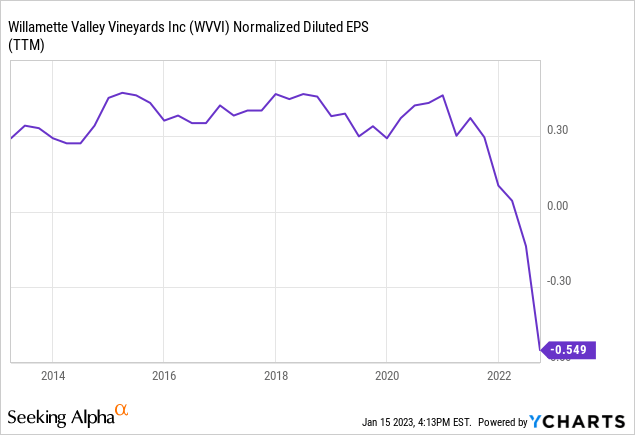

Unfortunately, this sort of expansion plan doesn’t come cheap. Willamette has tipped from being reasonably profitable into outright losses as it has invested heavily in these new hospitality assets:

It’s hard to overstate how dramatic a swing in the company’s finances we’ve seen since this business model shift. The company reliably earned somewhere in the 30-45 cents per share range year after year prior to 2022. With the stock price usually in the $6-$7 range, that amounted to a P/E around 20. All reasonable enough stuff from a valuation perspective, particularly if you felt the land had some upside optionality as well.

Now, however, the company’s earnings have tumbled to a 55 cent loss over the past 12 months. This makes Willamette Valley a more complicated investment decision. Now, investors have to affirmatively bet that the new tasting rooms and restaurants will pay off over time. Whereas, before, the company was steadily accumulating some value from its small but consistent earnings and the rise in underlying winery land valuations.

Here’s CEO and founder Jim Bernau on the earnings shortfall:

“Inventory delays at the start of the year have negatively impacted our sales through distributors in the first nine months of the year. We have also incurred additional expenses in the first nine months of the year in connection with the opening of four new tasting room and restaurant locations in 2022 as we significantly grew our footprint in the direct to consumer segment. We expect higher costs and reduced margins and earnings in the near term as we bring these new locations on line.“

There was similar language in prior quarterly earnings releases about how earnings will be depressed for an ongoing period before these new growth operations pay off in the form of higher profitability.

I would note that almost all of the earnings problems are from rising operating costs related to the firm’s footprint expansion. Year-over-year revenues have been close to flat, and margins are only down slightly. The firm’s existing operations don’t appear to be struggling any more than other food and beverage companies as it deals with higher inflation and supply chain issues.

The bigger question, in my mind, is simply whether the tasting rooms and restaurant will pay off as management expects, or whether their outlook is too optimistic.

That said, having more direct-to-consumer sales seems like a logical strategy, particularly since I see Willamette Valley as on the borderline of being too small to be a particularly successful NASDAQ-listed company otherwise. Making a play for significant growth at higher profit margins intuitively makes sense. And, at a discount to book value now, I believe investors are getting some margin of safety which offsets the fact that the company is currently running a meaningful operating loss.

WVVI Stock Verdict

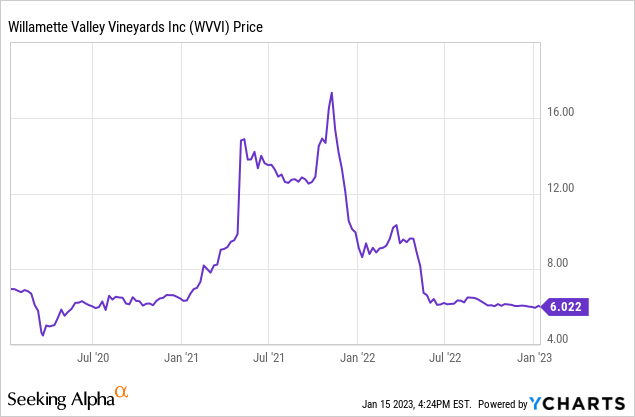

The run-up in Willamette Valley shares last year was utterly baffling. This is a very small and marginally profitable business in the best of times. Much of the value here comes from the underlying 704 acres of land the company owns along with the associated buildings and installed infrastructure there-in. Needless to say, the value of these fixed assets simply aren’t going to double overnight, regardless of what the stock price might do in the short run.

Simply put, there was little possible explanation for Willamette Valley as a $15 stock in 2021. This stock chart it just mystifying:

Regardless, at $6, the math is much more favorable for bulls. For one thing, shares are going for just 1.0x book value and 1.0x revenues, respectively. This gives potential investors a margin of safety. Presumably, even in a worst-case outcome, Willamette could simply sell off its land and wineries and recoup something close to its $6.41/share of reported book value, and perhaps even a premium to that depending on winery land values.

And, if the expansion of the consumer hospitality business pays off, this could be a significantly more profitable business in two or three years from now.

This isn’t my favorite wine stock by any means. However, for people that want to own multiple stocks in the industry, or which find the firm’s location, product, or social purpose of interest, this $6 entry point should work out well enough.

Editor’s Note: This article covers one or more microcap stocks. Please be aware of the risks associated with these stocks.