Two 10% Yielding CEFs Raising Their Monthly Dividends, Selling At Discounts

Zerbor

Looking for a way to benefit from rising rates? Interest rates keep rising, but that environment is seen as a negative for many sectors and companies.

With that in mind, we went searching for some high yield income vehicles that are actually raising their payouts in 2022. We found 2 closed-end funds, CEFs, that have had multiple payout hikes in 2022:

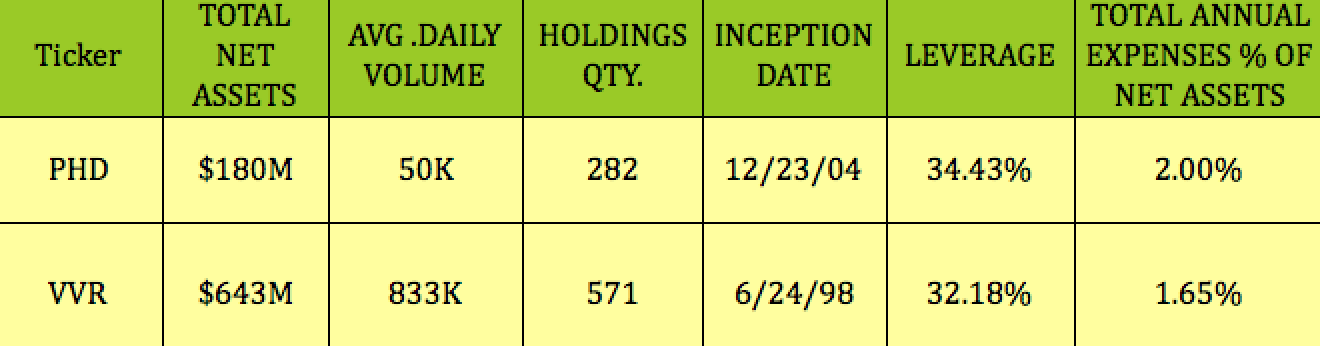

Pioneer Floating Rate Trust (PHD) is a CEF which seeks a high level of current income by investing primarily in floating-rate loans. It also seeks capital preservation as a secondary objective to the extent consistent with its primary goal.

Invesco Senior Income Trust (VVR) is a CEF whose investment objective is to provide a high level of current income, consistent with preservation of capital. The fund achieves its objective via investing primarily in floating or variable senior loans of issuers which operate in a variety of industries and geographic regions

PHD is much smaller than VVR, with $180M in assets, vs. $643M for VVR, which also has much higher average daily volume of 833K, vs. just 50K for PHD.

VVR holds 571 positions, vs. 282 for PHD. Both funds use 30%-plus leverage, with PHD using slightly more than VVR. PHD’s expense ratio is 2.00%, vs. 1.65% for VVR. VVR has been around 6 years longer, IPO’ing in 1998, while PHD debuted in 2004:

Hidden Dividend Stocks Plus

Dividends:

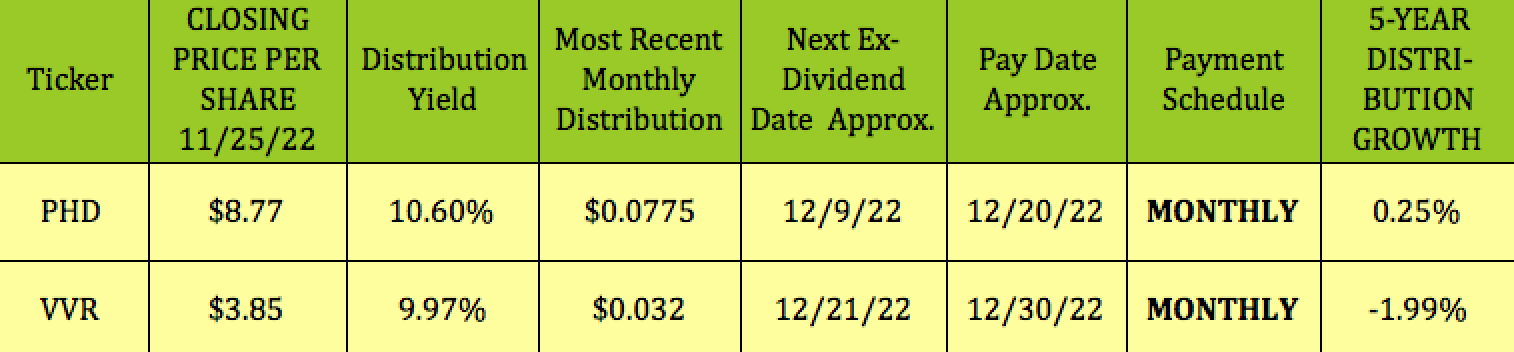

PHD has raised its monthly payouts 4 times so far in 2022:

Starting in June, it was raised from $.0575 to $.0600; in September it increased to $.0700. In October, it was raised again to $.075, and it was raised again in November to $.0775. The December distribution should be declared in early December. PHD’s 5-year dividend growth rate is 0.25%.

VVR has raised its monthly payouts 2 times so far in 2022: In April, it was from $.0210 to $.026; and in October, it was raised from $.026 to $.032. VVR’s 5-year dividend growth rate is -1.99%.

At its 11/25/22 closing price of $8.77, PHD yields 10.60%, based upon its most recent payout. It should go ex-dividend next on ~12/9/22, with ~12/20/22 payout.

At its 11/25/22 closing price of $3.85, VVR yields 9.97%, and should go ex-dividend next on ~12/21/22, with ~12/30/22 payout.

Hidden Dividend Stocks Plus

Both funds have had ample distribution coverage for these periods in 2022:

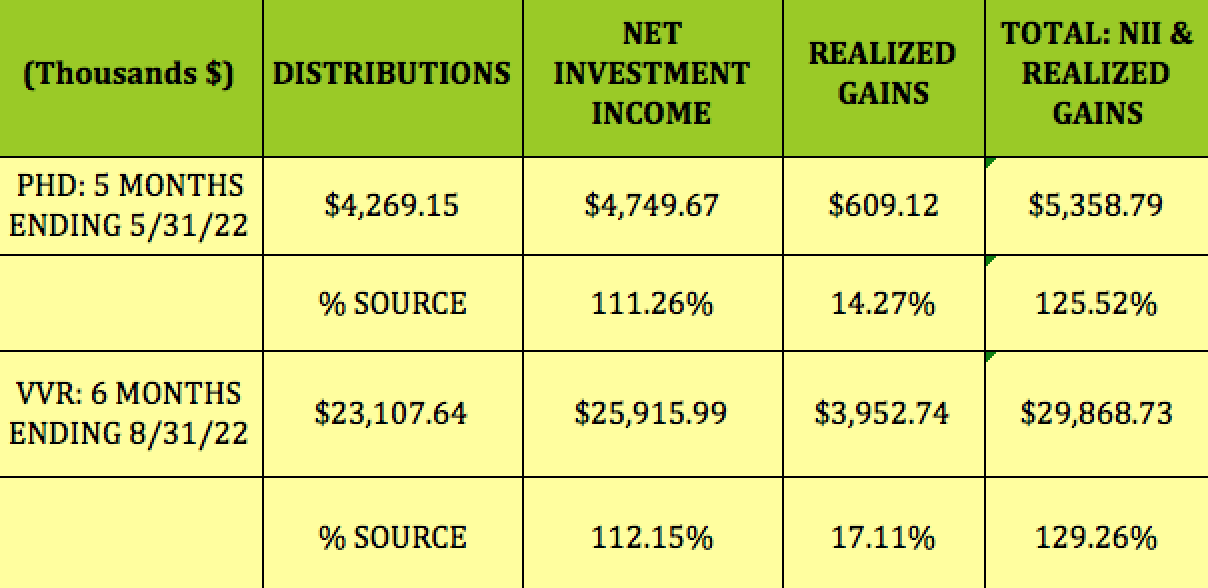

PHD has covered its payouts with NII by 1.11X, with an additional .1427X coming from realized gains, for a total distribution coverage factor of 1.255X, for January through May 2022.

VVR’s coverage factor is similar, but slightly higher, with 1.12X coming from NII, plus .17X coming from realized gains, for a 1.2926X coverage factor for January through August 2022:

Hidden Dividend Stocks Plus

Taxes:

As of 9/30/22, VVR’s fiscal YTD distributions were estimated be comprised of 100% net investment income, with no return of capital:

VVR site

PHD’s most recent 19a letter was back in July 2021, implying that there has been no return of capital since then.

Holdings:

PHD – The portfolio has an average weighted tenor of 4.68 years, with an effective duration of 0.14 Years:

PHD site

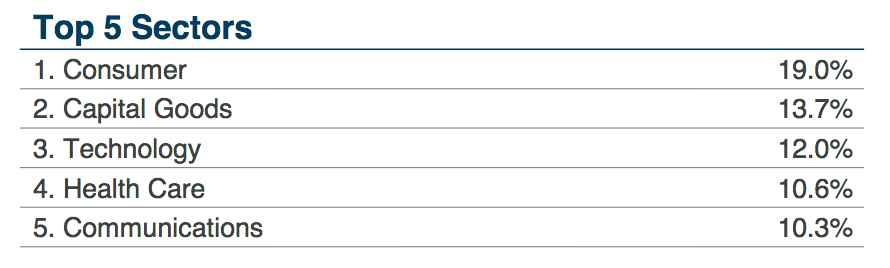

PHD’s top 5 sectors comprise ~66% of its portfolio, with the Consumer sector being its top exposure, at 19%, followed by Capital Goods, 13.7%, Tech, at 12%, Health Care, at 10.6%, and Communications, at 10/3%:

PHD site

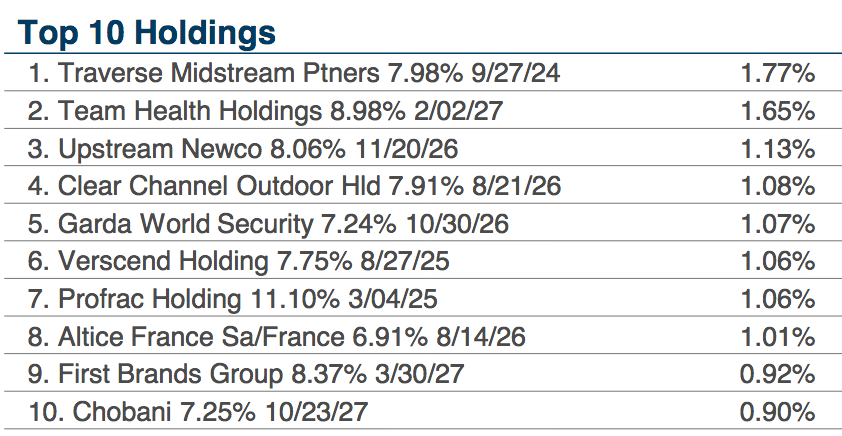

PHD’s top 10 holdings comprise ~11.7% of its portfolio, with the nearest maturity coming in September 2024, and the longest one in October 2027. The coupon rates range from 6.9% to 8.98%:

PHD site

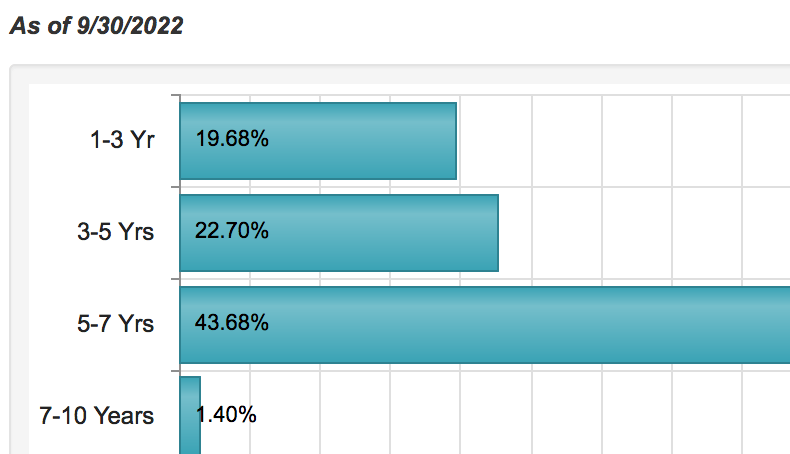

VVR‘s portfolio has an average maturity of 4.24 years, with ~44% in 5-7 year maturities, ~23% in 3-5 years, and ~20% in 1-3 year maturities.

VVR site

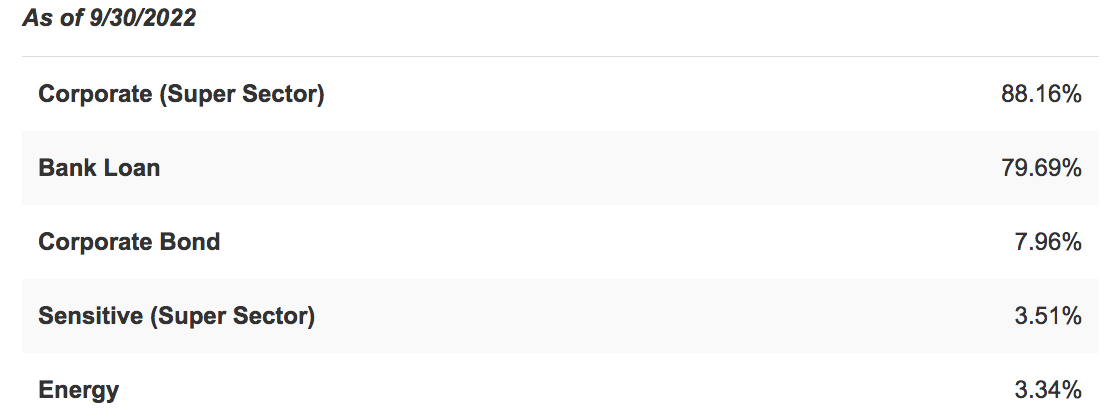

The portfolio is comprised of ~80% Bank loans, with a smaller position in Energy-related holdings.

VVR site

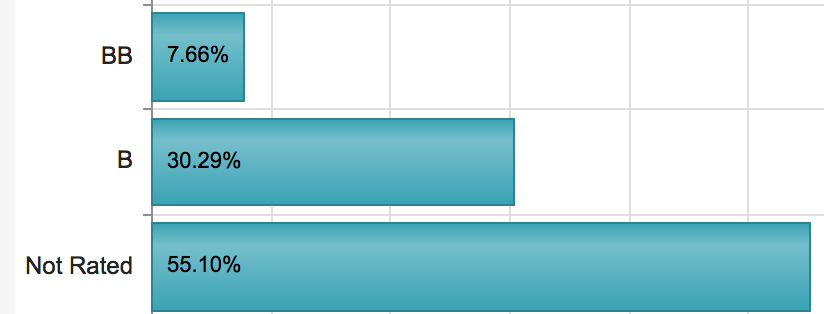

VVR’s portfolio is dominated by unrated instruments, at 55%, and B-rated ones, at ~30%:

VVR site

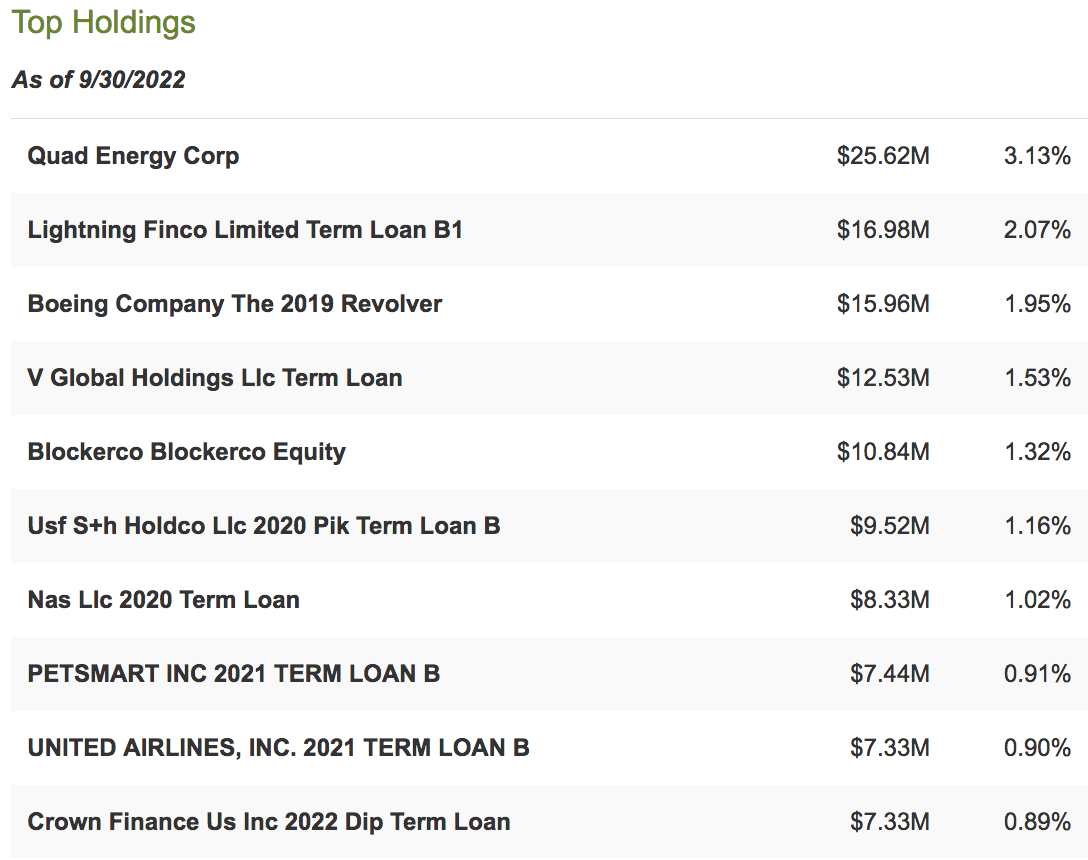

VVR’s top 10 comprised ~15% of its portfolio, and included debt from such well-known names as Boeing, PetSmart, and United Airlines, as of 9/30/22:

VVR site

Performance:

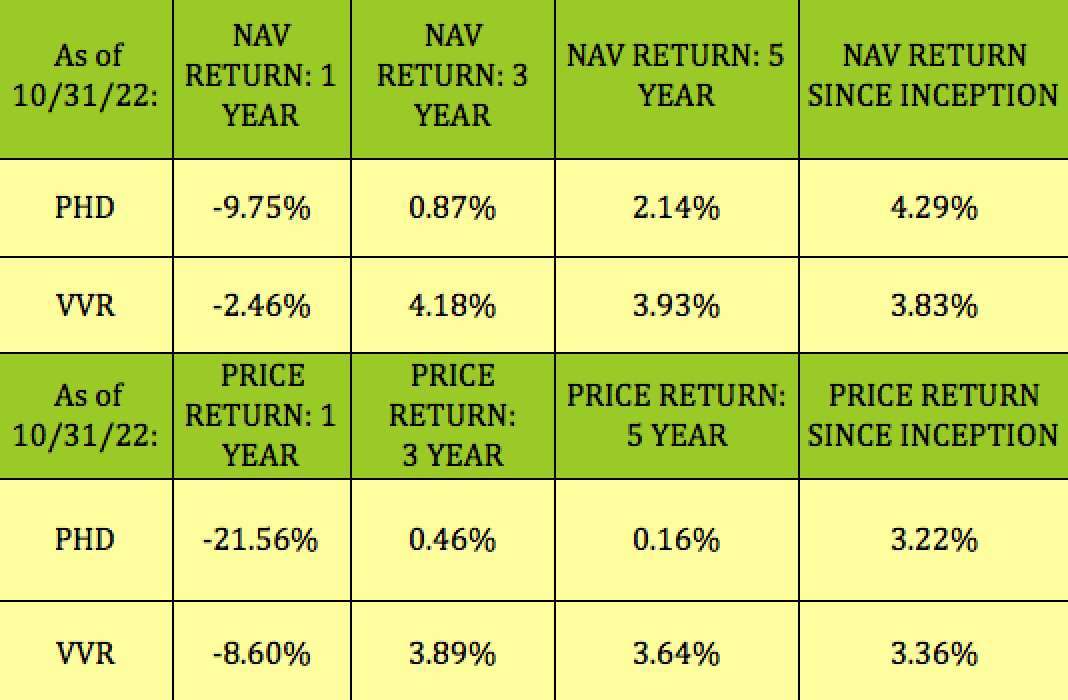

While PHD has a slightly higher NAV return since inception, VVR wins the race by far in the more recent 1-, 3-, and 5-year periods.

On a price basis, the 2 funds have very similar 3%-plus returns since inception. However, the market has been much kinder to VVR over the past 1-, 3-, and 5-year periods:

Hidden Dividend Stocks Plus

Valuations:

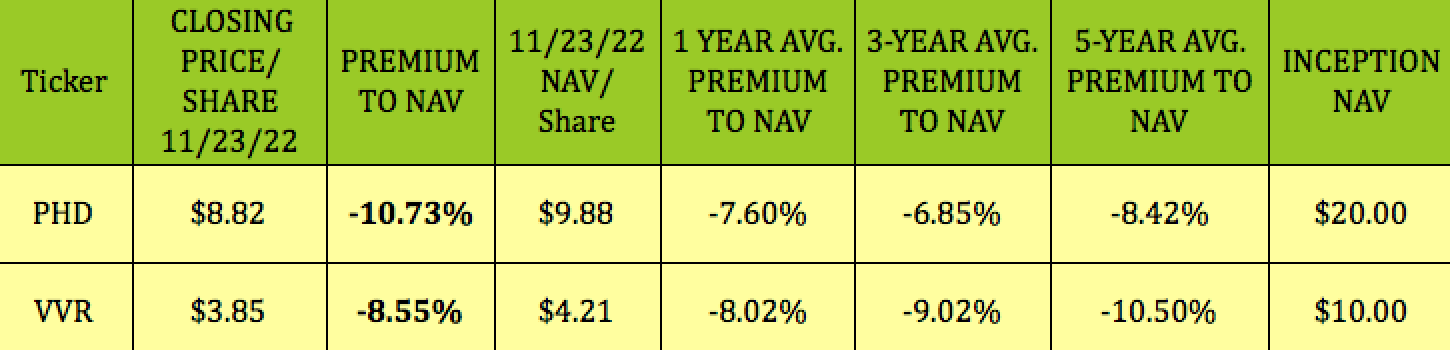

Both funds are currently trading at discounts to NAV/share, with PHD at 10.73% and VVR at 8.55%.

PHD’s current discount compares favorably with its 1-, 3-, and 5-year discounts, while VVR’s 8.55% discount is deeper than its 1-year 8% average discount, but a bit lower than its 3- and 5-year averages of 9% and 10.5%, respectively.

Buying CEFs at discounts to NAV that are deeper than their historical averages can be a useful strategy, due to mean reversion.

Hidden Dividend Stocks Plus

Parting Thoughts:

With the Fed on track to continue its rate hikes at least in the 1st half of 2023, these floating rate funds could be a good place to stash some cash for the near term.

Although its discount isn’t quite as deep as its 3- and 5-year averages, we favor VVR, because of its better long-term returns.

If you’re interested in other high yield vehicles, we cover them every Friday and Sunday in our articles.

If you’re interested in other high yield vehicles, we cover them every weekend in our articles. All tables by Hidden Dividend Stocks Plus, except where otherwise noted.