Ondas Holdings Prepares For Possibly Lumpy 2023 Growth (NASDAQ:ONDS)

metamorworks

A Quick Take On Ondas Holdings

Ondas Holdings (NASDAQ:ONDS) reported its Q3 2022 financial results on November 14, 2022.

The firm provides software-defined wireless technologies and commercial drone robotics solutions.

Management has the potential for any number of contract wins in 2023, but their probability is difficult to determine.

Given the high current valuation of the stock and the firm’s uncertain ‘lumpy’ contract business model, I’m cautious, although interested investors may make a case to go risk-on currently.

Accordingly, I’m on Hold for ONDS.

Ondas Overview

Sunnyvale, California-based Ondas Networks was founded in 2006 to provide wireless data radio technologies for IoT applications in the electric utilities, oil & gas, water, rail, transportation as well as government industries.

Management is headed by Chairman and CEO Eric A. Brock, who has been with the firm since 2017 and was previously Portfolio Manager at Clough Capital Partners.

Ondas’ lead product is FullMAX, a software-defined radio [SDR] system consisting of a wireless base station, fixed and mobile remote radios as well as supporting technology for wide-area broadband networks that enable secure industrial-grade connectivity.

The company’s SDR equipment is fully IEEE 802.16s compliant, has the ability to use frequencies between 30 MHz and 6 GHz, and has a wide coverage of up to 30 miles away from the tower.

Management calculates the total area coverage per FullMAX tower to be up to 2,800 square miles and compares it to the average of 4G tower, which they claim to be around 28 square miles.

“For example, to cover a territory of over 10,000 square miles may require only four FullMAX towers compared with more than 350 typical 4G towers, depending on the topography of the region.”

Besides their FullMAX technology, Ondas provides network design, RF planning, product training and spectrum consulting, technical support and related software.

Below is an overview image of the company’s target industries and applications:

Target Industries (SEC)

Ondas markets its products to critical infrastructure providers through a direct sales force, third-party resellers, customer referrals, consultant referrals, trade show attendance, general marketing efforts as well as public relations.

The firm has also acquired Airobotics to merge with its American Robotics subsidiary to provide a range of mobile data solutions in various industry verticals worldwide.

Ondas’ Market & Competition

According to a recent market research report by MarketsAndMarkets, the global software-defined radio wireless broadband industry is expected to reach $30 billion by 2022.

This represents an 8.63% CAGR between 2017 and 2022.

The land-based commercial segment is expected to lead demand growth due to increased investment by private operators in improved technologies.

Major competitors that provide or are developing software-defined wireless technologies include:

-

Harris

-

Northrop Grumman (NOC)

-

BAE Systems (OTCPK:BAESF)

-

Rockwell Collins

-

Thales

-

General Dynamics (GD)

-

Huawei

-

ZTE Corp (OTCPK:ZTCOY)

-

Elbit Systems (ESLT)

The company’s technology is, according to their website, cheaper to install than LTE 4G or 5G networks due to the lower costs of the radio frequency spectrum and provides larger coverage of up to 30 miles from a tower.

Ondas’ Recent Financial Results

-

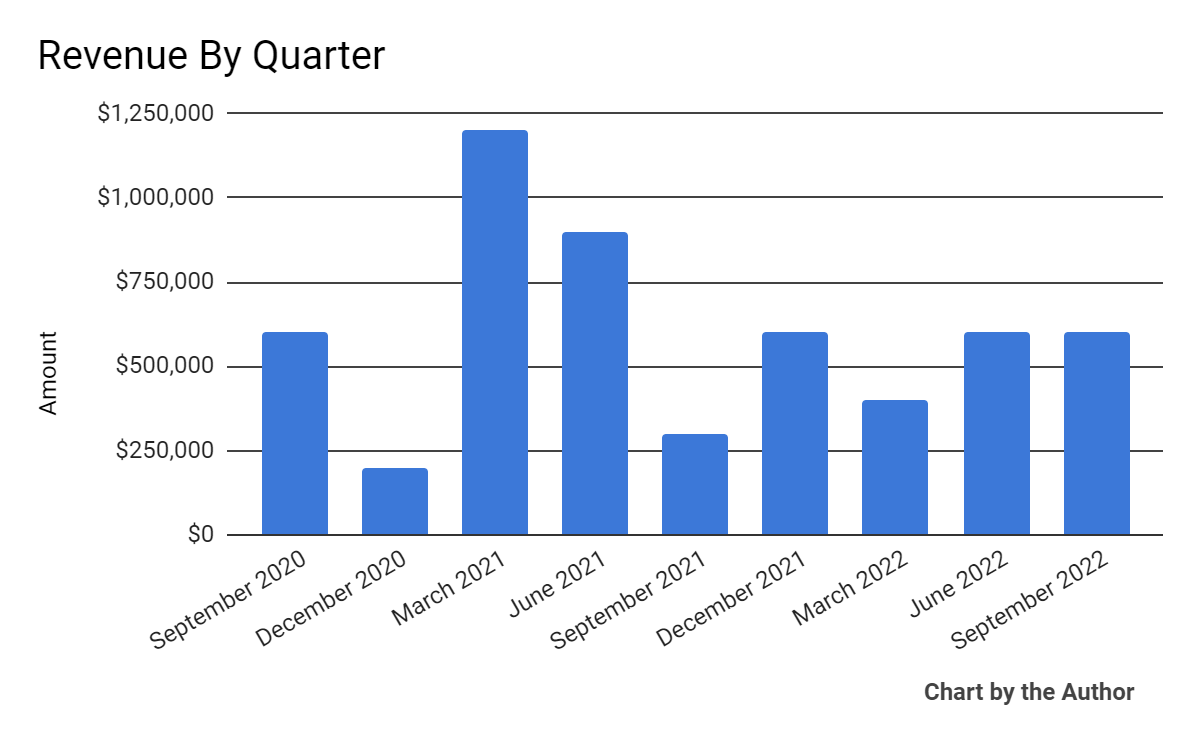

Total revenue by quarter has produced the following trajectory:

Total Revenue (Seeking Alpha)

-

Gross profit margin by quarter has trended higher in recent quarters:

Gross Profit Margin (Seeking Alpha)

-

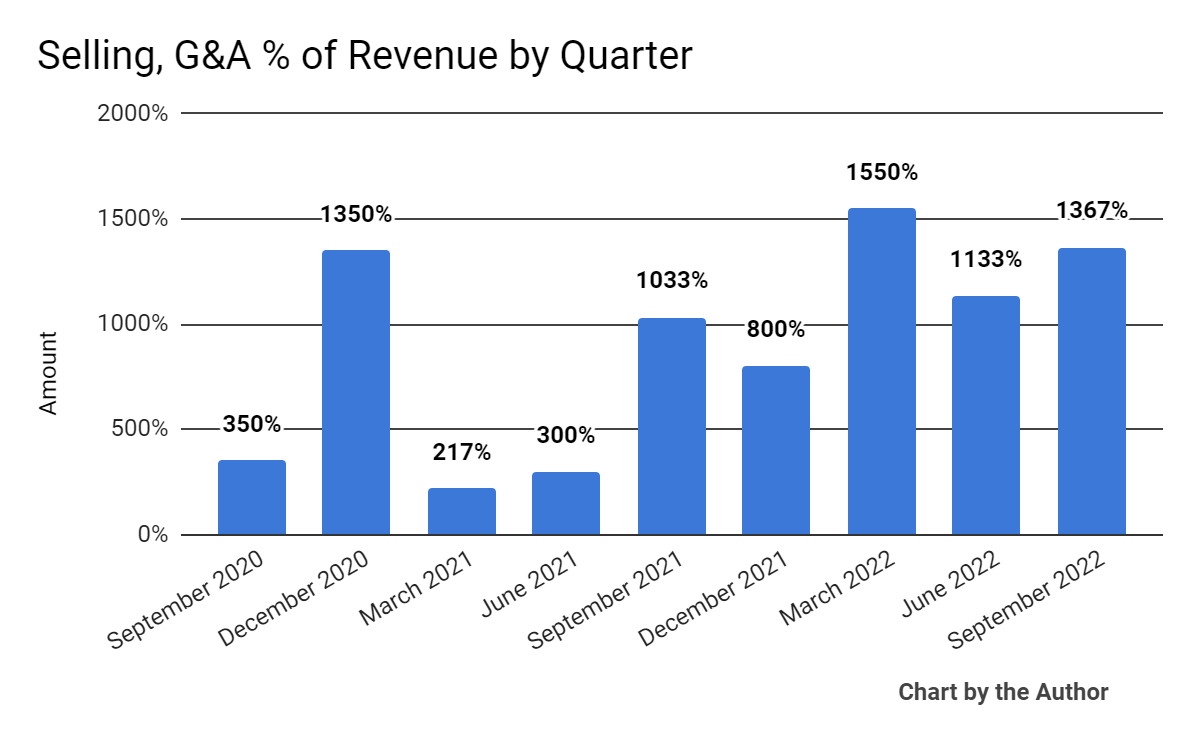

Selling, G&A expenses as a percentage of total revenue by quarter have increased in recent quarters and remain very elevated:

Selling, G&A % Of Revenue (Seeking Alpha)

-

Operating losses by quarter have worsened materially in recent quarters:

Operating Income (Seeking Alpha)

-

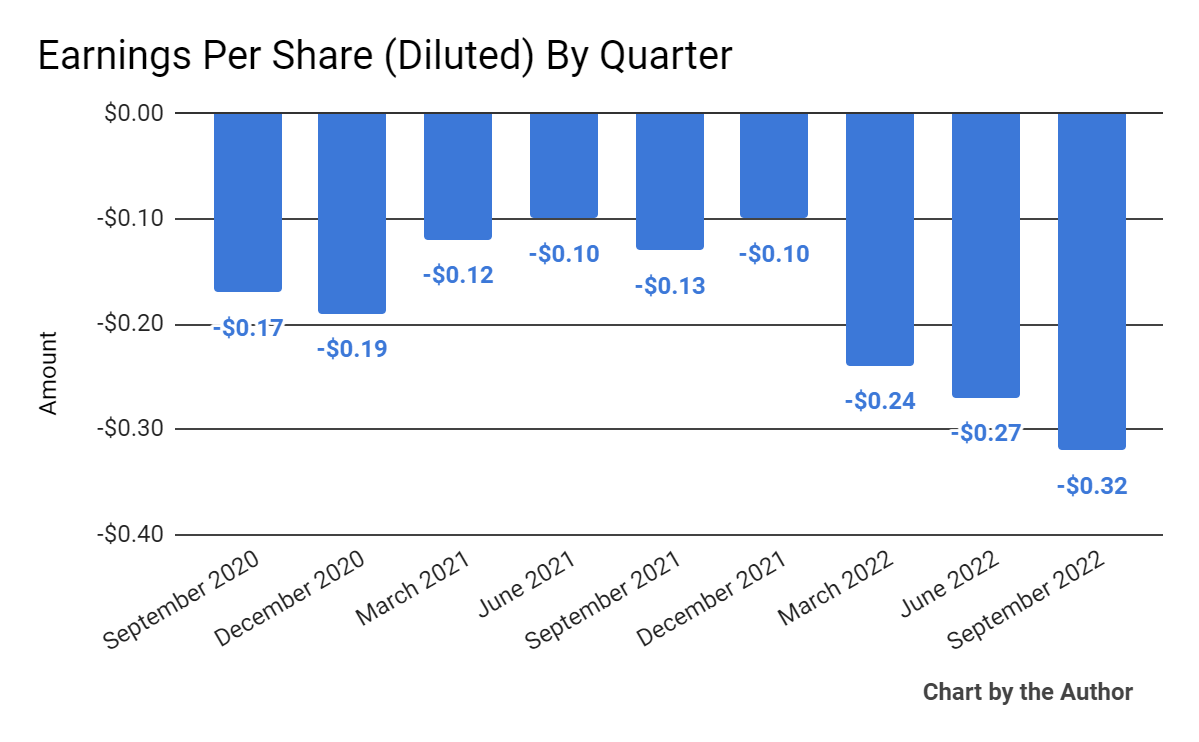

Earnings per share (Diluted) have also deteriorated sharply recently:

Earnings Per Share (Seeking Alpha)

(All data in the above charts is GAAP)

In the past 12 months, ONDS’s stock price has fallen 66.7% vs. that of the Nasdaq 100 Index’s drop of 15.4%, as the chart indicates below:

52-Week Stock Price Comparison (Seeking Alpha)

In its last earnings call (Source – Seeking Alpha), covering Q3 2022’s results, management highlighted its $250 million investment in a variety of its business segments, with no reward for investors to date.

However, the firm is ‘seeing fleet demand build’ as its Airobotics segment continues to build out according to its business plan.

As to its financial results, total revenue doubled year-over-year, while gross profit margin rose sequentially.

SG&A as a percentage of total revenue continued to fluctuate at an extremely high level and operating losses worsened materially, as did earnings per share.

For the balance sheet, the firm finished the quarter with $15.3 million in cash and equivalents and $300,000 in long-term debt.

Over the trailing twelve months, free cash used was $35.9 million, of which capital expenditures accounted for $4.4 million. The company paid a hefty $5.7 million in stock-based compensation in the last four quarters.

Valuation And Other Metrics For Ondas

Below is a table of relevant capitalization and valuation figures for the company:

|

Measure [TTM] |

Amount |

|

Enterprise Value / Sales |

33.7 |

|

Enterprise Value / EBITDA |

NM |

|

Price / Sales |

35.7 |

|

Revenue Growth Rate |

-12.3% |

|

Net Income Margin |

NM |

|

GAAP EBITDA % |

NM |

|

Market Capitalization |

$86,340,000 |

|

Enterprise Value |

$74,630,000 |

|

Operating Cash Flow |

-$31,470,000 |

|

Earnings Per Share (Fully Diluted) |

-$0.93 |

(Source – Seeking Alpha)

Future Prospects For Ondas

Company leadership believes that the firm’s strong balance sheet should remove the share discount the markets have placed on smaller companies with high operating losses.

Ondas’ near-term future received a bit more clarity from its recent announcement of Q4 revenue, which is likely to be above expectations.

The announcement referenced a potential Q4 2022 revenue beat of $500,000 over consensus estimates of $1.56 million.

ONDS finished Q4 with an order backlog of around $12.9 million, with orders representing growing activity across its major segments.

For fiscal 2023, management now expects revenue of around $28 million at the midpoint of the range, versus consensus estimates of nearly $25 million.

A potential upside catalyst to the stock could include wins for any number of contracts the firm and its subsidiaries are pursuing.

While the stock of contract-oriented companies like Ondas can move quickly based on a contract win announcement, the proof is always in how quickly the firm can deliver products to recognize that future revenue.

So, ‘lumpy’ contract-centric revenue streams can mean a wild ride for investors at times.

Compared to subscription revenue companies which have more predictable revenue streams, such companies can see substantially higher volatility in their stock price over the short term.

Regarding valuation, the market is valuing ONDS at an Enterprise Value/Revenue multiple of 33.7x.

The primary risks to the company’s outlook are the uncertain nature of its contract business and its tiny size which makes the purchase decision by larger firms more difficult.

Given the high current valuation of the stock and the firm’s uncertain ‘lumpy’ contract business model, I’m cautious, although interested investors may make a case to go risk-on based on its potential for growth and the potential for a short-term catalyst.

For the near term, though, I’m on Hold for ONDS.

Editor’s Note: This article covers one or more microcap stocks. Please be aware of the risks associated with these stocks.