ILF ETF: Focus On Latin America With A 5% Yield (NYSEARCA:ILF)

Jordan Siemens/DigitalVision via Getty Images

Thesis

Latin America is becoming interesting as the local governments are beginning to cut interest rates. After Brazil reduced its interest rate again in March 2024, Colombia followed suit by cutting rates on April 30, 2024. Monetary loosening is usually accompanied by a buoyant equity market, although regional factors also play a large role in overall equity performance.

In this article we are going to have a closer look at the iShares Latin America 40 ETF (NYSEARCA:ILF), an exchange traded fund that invests in South American equities.

Composition – overweight Brazil and Mexico

First let us have a look at how the fund invests from a country perspective:

Geographic Breakdown (Fund Fact Sheet)

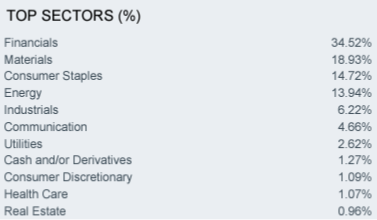

The ETF is overweight Brazil and Mexico, which represent over 80% of the fund. From a sectoral standpoint, financials and materials have the largest representation:

Sectors (Fund Fact Sheet)

Financials represent 34% of the fund, followed by materials at 18% and consumer staples at 14%. From an individual name perspective the top names are Vale (VALE), Petróleo Brasileiro (PBR) and Itau (ITUB). Please note these are all New York Stock Exchange listed ADRs, but the fund does contain many locally listed equities. Locally listed names run foreign exchange risk and local political risk.

Mexico – benefiting from China tensions

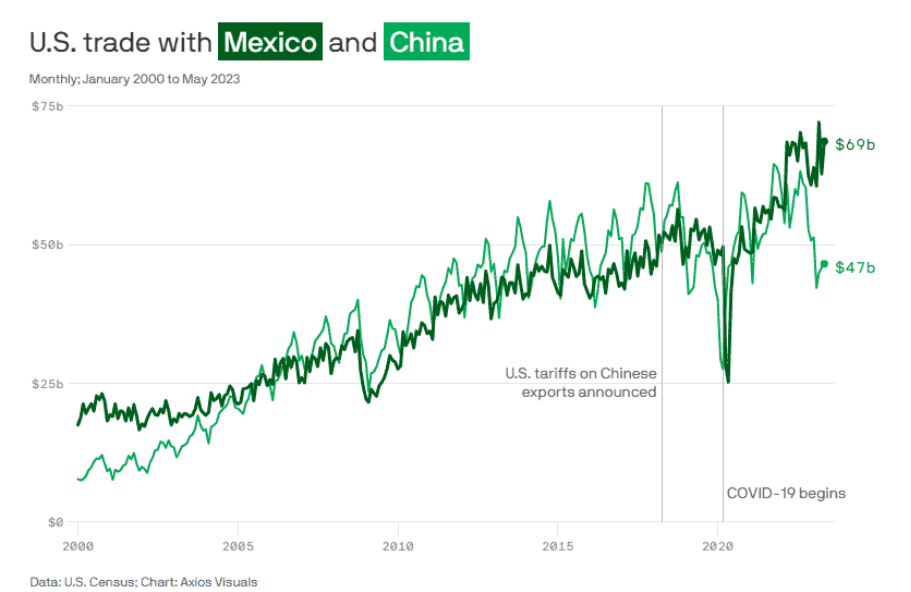

The second largest geographic exposure in the fund, namely Mexico, is currently experiencing a secular change in fortunes. With China tensions running high, and China becoming a world-stage competitor for the U.S., America has chosen to ‘near-shore’ its supply chain to Mexico as much as possible:

U.S. trade with Mexico (Axios)

This trend is set to continue, with the likes of Tesla discussing building a new plant in Mexico, and many companies choosing to shorten their supply chains via production in the southern neighbor.

The first impact of this secular change has been felt in the currency, with the Mexican peso appreciating significantly in the past two years, while the equity market has also outperformed. Expect this trend to continue. Secular trends take time to fully develop, but they have tangible impacts for both individuals as well as capital markets.

An increase in jobs and job payments in Mexico will eventually make their way to more profitable Mexican companies, which in turn will be reflected in higher P/E ratios and EPS figures. We feel Mexican equities will re-rate higher from a P/E standpoint as this trend continues and becomes more apparent to all market participants.

While from a risk standpoint Mexico is still known for its occasional bouts of cartel violence, the government has been very prescriptive about ring-fencing the cartel operations from the rest of the economy, especially when large enterprises are considered.

Performance – providing diversification

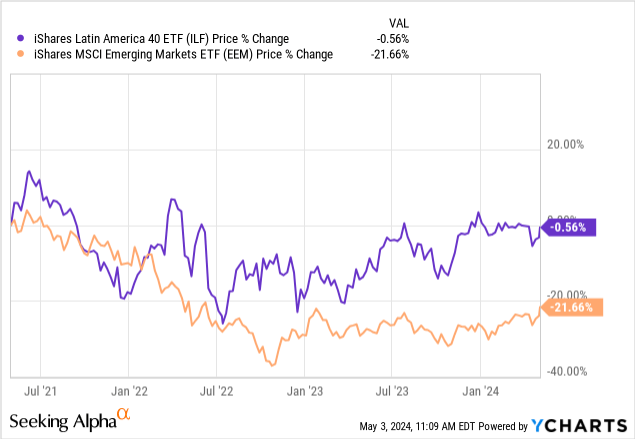

ILF has proven to be a savvy portfolio diversifier when looking at EM:

When comparing the ETF to the iShares MSCI Emerging Markets ETF (EEM) we can clearly see the benefits of diversification. EEM has a significant amount of exposure to China equities, and has been dragged down in the past few years by that allocation.

Valuation metrics are appealing

What makes this fund appealing outside the EM diversification aspect, is the valuation:

Valuations (Morningstar)

The ETF focuses on large value names with an incredible 8x P/E ratio. We have come to understand that EM has lower P/E figures for a reason from the China and Russia experiences, but there are no obvious looming political risks in Latin America currently.

One can argue quite the opposite – being close to the U.S. from a geographic and historic relationship standpoint, has made Latin America (‘Latam‘) more resilient to serious conflicts given the economic ties with the U.S. (we are specifically referencing here any wars or outright conflicts between countries). While Russia invaded Ukraine and China might take action on Taiwan, there is no brewing similar conflict in Latam, and we do not see one ever happening. Latam suffers from corruption and graft, but it does not torpedo investors via wars with other nations.

We are of the opinion that Latam represents a growth story on the back of more resilient democracies, and the economic systems have moved towards a larger integration with the global economy, with all the related benefits.

Dividend is high, but relies on Financials and Energy names

The ETF has a 5% trailing 12-months dividend yield as you can see from the Seeking Alpha landing page. However, the name pays only semi-annually and relies on Financials and Energy names for the bulk of the cash, thus the dividend will vary.

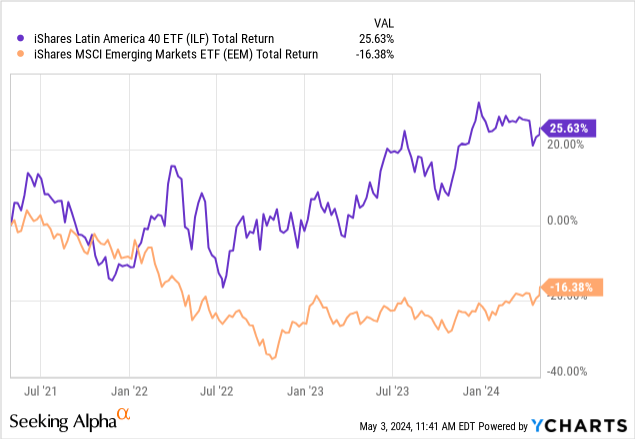

However it is unusual to find such high dividend yields in EM equity funds. When we run the above graph vs EEM on a total return basis (i.e. dividends included), we get an even better picture:

When factoring dividends in, ILF is up +25% in the past 3 years, versus -16% for EEM.

A soft landing and lower rates are supportive

A soft landing in the U.S. and lower local rates are supportive for a continued outperformance in ILF from a macro standpoint. From an individual security perspective we have shown investors above the relative cheapness of the respective equities via their P/E ratios.

Conclusion

ILF is an exchange traded fund focused on Latam equities. The vehicle is overweight Brazil and Mexico equities, and has a large 5% trailing 12-months dividend yield paid semi-annually. The dividend comes from financials and energy/materials names in the fund, and will change as underlying equities alter their dividend policy. The fund is a diversification tool for EM equities, having significantly outperformed the Asia focused EEM fund. We are witnessing a secular change in Mexico via the higher U.S. trade, replacing China in the supply chain. Similarly Brazil and Colombia have been cutting their local interest rates, thus providing stimulative monetary policy that should be supportive of their equities. We like ILF here as a portfolio diversifier and an attractively valued EM equity fund.