Enterprise Product’s Growth Doesn’t End At 2024 (NYSE:EPD)

Alex Potemkin

Enterprise Products (NYSE:EPD) is in a state of continued improvement in the Permian Basin with 3 new gas processing facilities brought online with 3 additional under construction. Though natural gas remains in a bear market domestically, the firm is realizing strength in their liquids business with crude oil and NGL volumes realizing strength in q1’24. Management anticipates to maintain their elevated capital budget throughout eFY24-25 before tapering off in eFY26 as projects come online. Enterprise should realize significant growth as a result, especially as producers favor more liquids-rich basins. I reiterate my BUY recommendation for EPD units with a price target of $35.70/unit at 10x eFY25 EV/aEBITDA.

Be sure to read my initial report covering Enterprise Products here:

Enterprise Products Partners Has A Huge Runway In The Permian Basin

Enterprise Operational Update

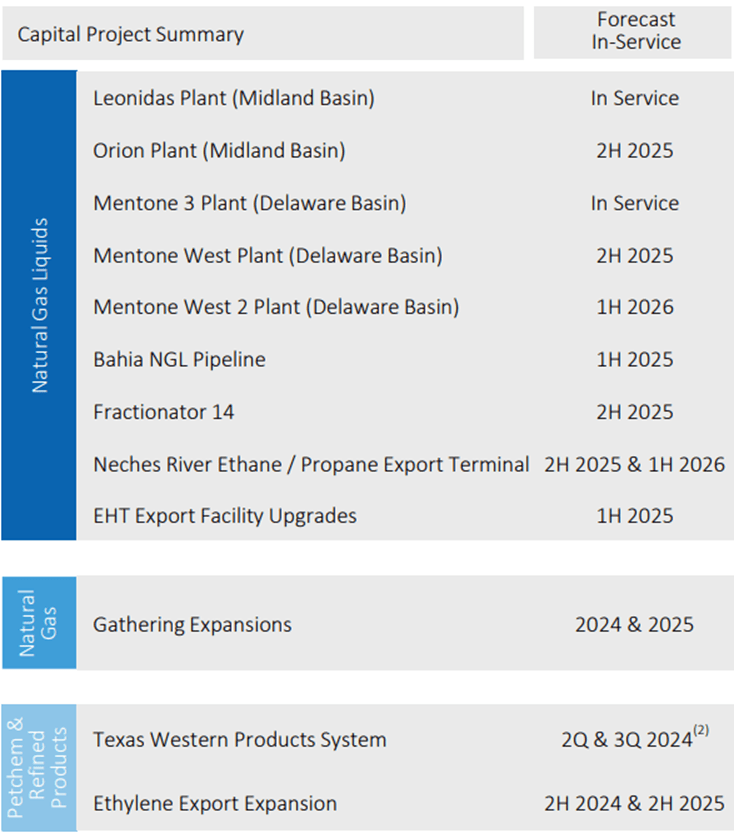

Enterprise is positioning itself exceptionally well with significant growth occurring across the Permian Basin as operators bolster production at their Delaware and Midland Basins. In q1’24, Enterprise added 600MMcf/d of natural gas processing capacity in these two basins as the firm brought online their Leonidas plant in the Midland Basin and Mentone 3 plant in the Delaware Basin. These plants also have the capacity to extract 40Mbbl/d of NGLs. In addition to these facilities, Enterprise has 3 additional 300MMcf/d plants under construction in the Delaware Basin and one in the Midland Basin. The firm is also in the process of constructing their Bahia NGL pipeline and Frac 14 which are expected to go online in 1h25 and 2h25, respectively.

Corporate Reports

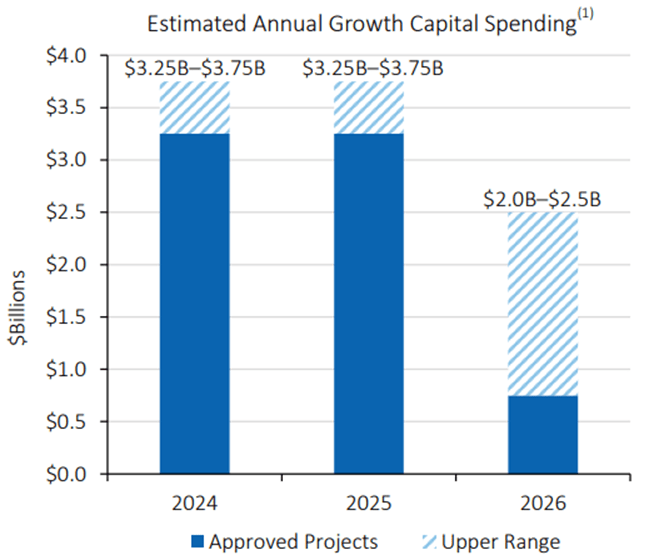

In total, management expects to invest $3.25-3.75b in eFY24 and eFY25 in capital projects before tapering off to $2-2.5b in eFY26. As of the end of April, the firm has a total of $6.9b in projects currently under construction. $550mm of the capital investments made in eFY24 will be in sustaining expenditures, which will include their petchem turnarounds. Management anticipates sustaining capital investments to decline to $450mm, suggesting more growth capital will be spent in the coming year as capacity in the Permian expands.

Corporate Reports

In addition to these projects, Enterprise began service of Phase 1 on the Texas Western Products System back in March 2024, with 10Mbbl/d of truck loading capacity and 900Mbbl of storage capacity for gasoline and diesel. Management expects Phase 2, which will be the terminals in Albuquerque, New Mexico, and Grand Junction, Colorado, to come online in eq2’24 or eq3’24. At the time of the q1’24 earnings call, truck load volumes were ramping up daily with Albuquerque being on the verge of commissioning. In order to supply refined products to these terminals, Enterprise converted segments of its Chaparral and Mid-America NGL pipeline systems to accommodate gasoline and diesel.

Management updated Enterprise’s position on their SPOT, or seaport oil terminal in which the firm received a license to move forward to the next step in commissioning the project. Once operational, this deepwater terminal will be capable of loading 2MMbbl/d of crude oil. The terminal will be located offshore Brazoria County, Texas, and will have a direct connection to the ECHO terminal with the ability to load at a rate of 80Mbbl/hour.

Corporate Reports

Enterprise did realize strong incremental volume increases, resulting in a 19% year-over-year increase in revenue generation. Most of this growth was driven by crude oil pipelines & services as well as petchem & refined products & services revenue, growing at 30% and 58%, respectively. Management did mention in their q1’24 earnings call that Enterprise will be undergoing a planned turnaround at their PDH plants, the IBDH facility, and their high-purity isobutylene facility in eFY24. PDH was expected to be completed in May 2024 with PDH 2 being completed in June.

Corporate Reports

Enterprise realized significant tailwinds in relation to higher volumes across their NGL segment and natural gas processing in the Permian. The natural gas processing segment realized a 429MMcf/d increase in fee-based volumes and significantly improved the GOM, increasing to 37% in q1’24, up from 26% in q1’23. The NGL transport & services segment also experienced modest margin improvements with Enterprise realizing higher average transportation fees and an incremental increase of 45Mbbl/d in NGL volumes in the quarter. The crude oil segment experienced significant tailwinds as crude transport volumes increased by 65Mbbl/d on their Midland-to-ECHO Pipeline System. Margins improved on the back of higher fees and transport volumes.

Corporate Reports

Petrochemicals experienced strength as a result of their octane enhancement facilities as well as realized strength in their ethylene pipelines and export terminal. Enterprise did experience some sequential headwinds in the segment as PDH 1 was down for 52 days and their propylene spitters were down for 32 days in q1’24 for both planned and unplanned maintenance. Propylene prices remain challenged as additional capacity comes online, which may be attributable to new capacity being brought online in China while the broader market demands more modest growth. This segment may experience some macro risks net of the firm’s octane enhancements.

TradingEconomics

Valuation & Shareholder Value

Corporate Reports

EPD currently trades at 9.75x EV/aEBITDA, which I believe is relatively low when considering the growth opportunities at hand. Management anticipates to balance out the firm’s cash flow generation by using 55-60% of operating cash flow to pay out distributions and unit buybacks. This has driven Enterprise to have a massive yield of 7.11% for distributions alone. In total, Enterprise has paid out $4.4b in distributions and buybacks over the last twelve months. In terms of debt, the firm did add a marginal amount of debt to the balance sheet; however, they remain near their 3x leverage target.

FinChat

Comparing EPD to its peers, there remains some room for EPD to realize a higher valuation closer to 11x EBITDA, especially when considering the firm’s growth projects across the Permian Basin.

Corporate Reports

Overall, I believe EPD has some upside potential in the tank and will have the ability to realize both aEBITDA growth and expansion of their multiples. I reiterate my BUY recommendation for EPD units with a price target of $35.70/unit at 10x eFY25 EV/aEBITDA.