BDC Weekly Review: BDCs Are Building Up Loan Loss Reserves

Darren415

This article was first released to Systematic Income subscribers and free trials on Feb. 11.

Welcome to another installment of our BDC Market Weekly Review, where we discuss market activity in the Business Development Company (“BDC”) sector from both the bottom-up – highlighting individual news and events – as well as the top-down – providing an overview of the broader market.

We also try to add some historical context as well as relevant themes that look to be driving the market or that investors ought to be mindful of. This update covers the period through the second week of February.

Be sure to check out our other Weeklies – covering the Closed-End Fund (“CEF”) as well as the preferreds/baby bond markets for perspectives across the broader income space. Also, have a look at our primer of the BDC sector, with a focus on how it compares to credit CEFs.

Market Action

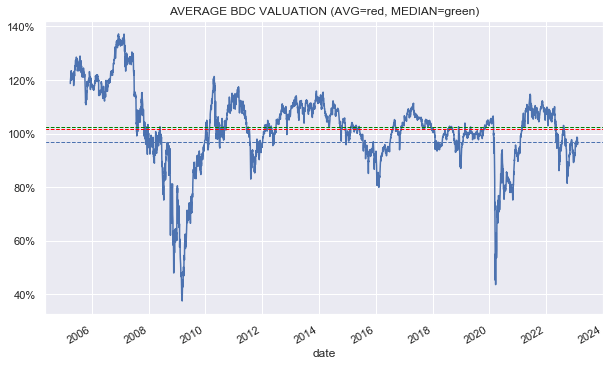

BDCs had a rare off week this year with a -1.5% total return. WhiteHorse Finance (WHF), which we highlighted the other week as being unusually cheap on a historic basis, outperformed with a 3% rally.

Valuations remain elevated, as the continued rise in sector earnings and dividend hikes create a tailwind for the sector.

Systematic Income

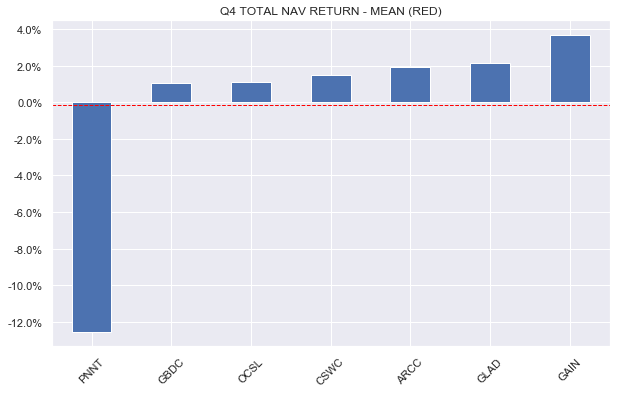

Earnings continue to trickle in. Outside of PennantPark (PNNT), which is going through a painful unwind of its hefty RAM Energy position, the rest of the sector has delivered positive total NAV returns for the quarter.

Systematic Income

Market Themes

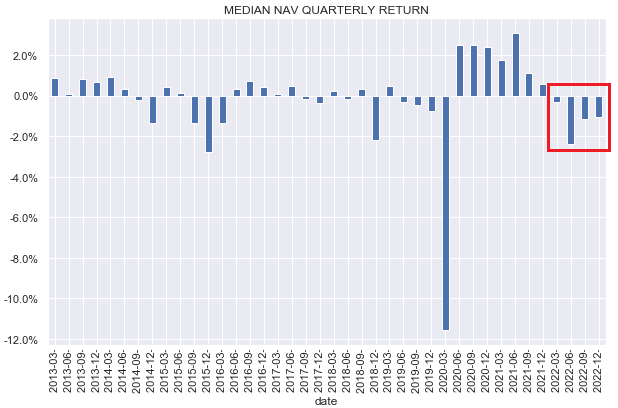

Though not all Q4 results are in, the median NAV has moved lower for the fourth quarter in a row, with the total cumulative 12-month trailing NAV drop around 4%.

Systematic Income

Though these losses are a combination of different factors, they are largely made up of unrealized depreciation, i.e., mark-to-market losses from yields moving higher over the past year.

Although NAV drops may not look great, they do come with a couple of offsetting benefits. First is that new loans are being made at higher yields than loans that are being prepaid or that are maturing, creating an income tailwind for the sector.

And two, current default rates remain unusually low, both in the private credit as well as public credit markets. This is supported by an economy that continues to run at a decent level despite the Fed’s sharp tightening, defaults that were brought forward by the unexpected COVID pandemic in 2020 clearing out some of the weaker companies and fairly strong corporate fundamentals such as low leverage and low interest expense.

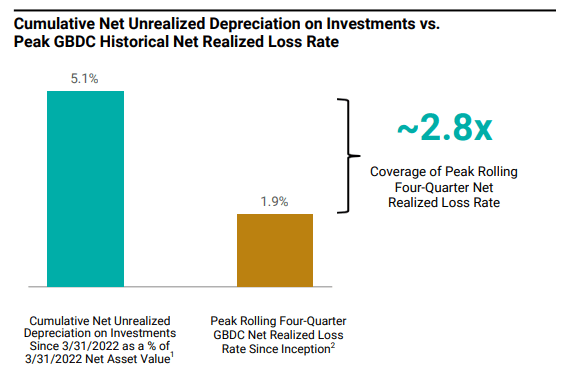

What this suggests is that some or much of the unrealized depreciation that we have seen could reverse when the economy starts its eventual drift higher. Golub Capital BDC (GBDC) has an interesting chart in its presentation, showing that its cumulative net unrealized depreciation since Mar-22 was nearly 3x higher its peak rolling four-quarter net realized loss.

GBDC

In other words, unless the next recession proves to be unusually severe, the NAV drops we have witnessed across the sector can be viewed as a kind of loan-loss reserve that investors often hear banks put in during macro downshifts. These loan loss reserves could easily be unwound, creating a NAV tailwind once the macro bottom is in.

However, even if we do see a wave of losses across the sector, some of these losses are already “in the kitty,” meaning whatever losses happen, they will be cushioned by the current stores of unrealized depreciation.

Market Commentary

PennantPark had a terrible quarter, with a 14% drop in the NAV. The main reasons are two long-standing oversized equity positions in RAM Energy and Cano Health. RAM Energy is being effectively unwound with its major asset now sold so that will mark the end of that position. Cano Health fell by 84% over Q4 but has now rallied back 40% (the stock trades in the public market) so if this holds, half of its loss will be made back.

PNNT stock price fell only about half that of the NAV drop so much of this loss was already priced into the stock and has rallied further by the end of the week. The company continues to push its portfolio towards secured loans by reducing its equity holdings so we shouldn’t expect similarly large moves in the NAV going forward. At the same time, such losses are an indication of historic underwriting quality.

Ares Capital (ARCC) saw a 26% jump in net income from the previous quarter (9% increase year-on-year) and a drop of around 1% in the NAV, resulting in a pretty strong Q4 result overall. The base dividend remained the same at $0.48. ARCC paid out a total $0.51 in Q4 ($0.48 base + $0.03 supplemental with the supplemental declared earlier in the year). Current dividend coverage is a stupidly high 131% so it is very unlikely they will keep the dividend at current levels for long.

This conservative dividend stance is a view on a normalization in interest rates at some point later this year. In short, ARCC simply don’t want to be in a position to have to cut the dividend so they don’t want to raise it now. However, with additional income tailwinds in store, they may have no choice in the medium term.

Stance and Takeaways

This week we continued to take down the overall risk profile of our High Income Portfolio in light of the sharp rally over the last couple of months.

Specifically, we moved the small PNNT allocation to the Saratoga 2027 baby bond (SAY) and the BDC Oaktree Specialty Lending (OCSL). PNNT had a nice bounce on Friday which erased about half of the loss related to the Q4 earnings release. Year-to-date the stock is flat in total return terms and has outperformed OCSL so it provides a nice timing to switch to a lower-beta / higher-quality stock. It does look like its underwriting problems are catching up with PNNT so its lowish valuation could persist for a while and creates the risk for further downside in the NAV.

We also moved half of the 2% ARCC position back to OCSL after a double-digit return round-trip over about a month as ARCC sharply outperformed OCSL over this stretch. We made the original switch to ARCC when OCSL traded up to a 5% higher valuation. Now trading at a 6% lower valuation than ARCC, OCSL offers a more attractively priced stock.