Debt Ceiling Deal May Drain A Massive Amount Of Liquidity From The Market

Viorika/iStock via Getty Images

The debt ceiling headlines have been a significant tailwind for stocks, primarily due to the draining of the Treasury General Account (TGA) and the flight to safety into mega-cap stocks. However, with an agreement reached to increase the debt ceiling, the dynamics should reverse, creating a sell-the-news event.

The TGA’s depletion, resulting from reduced debt issuance, has benefited the market by freeing-up reserve balances. However, as the debt ceiling is raised and new debt issuance occurs, the TGA will likely see a substantial increase.

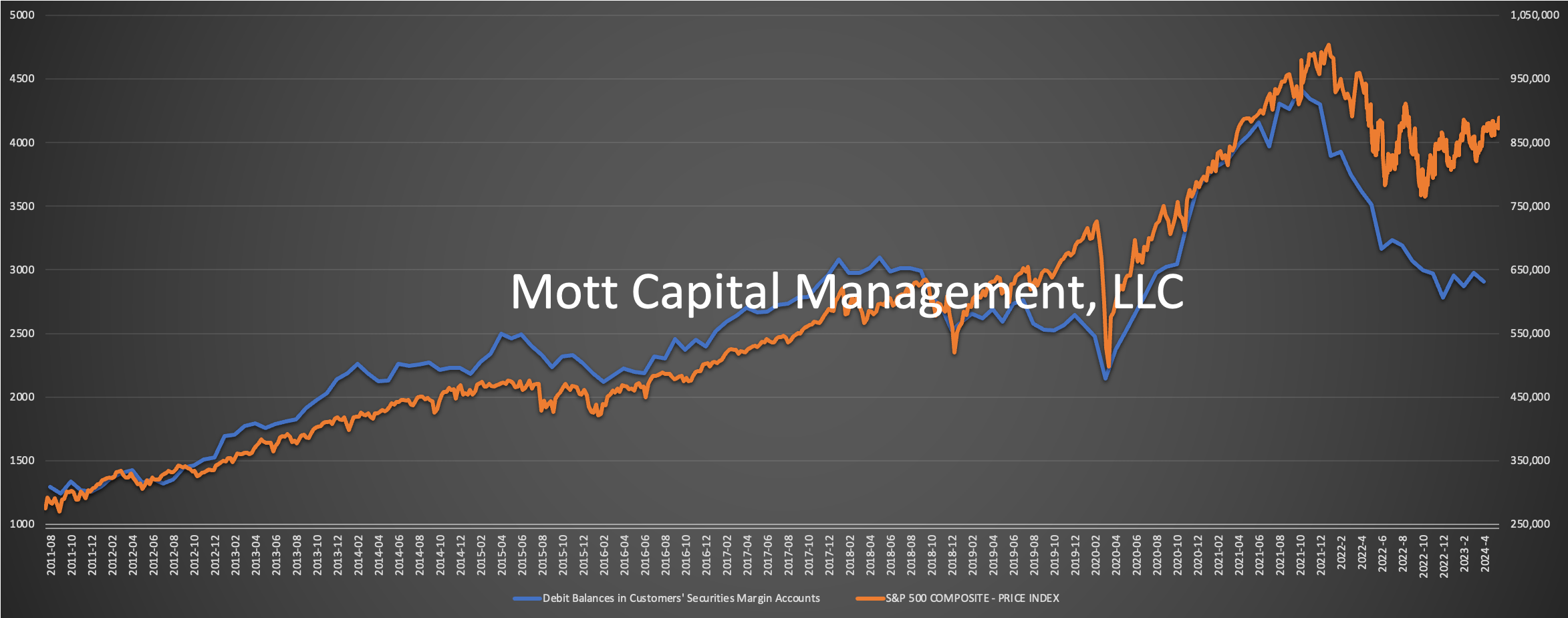

As the TGA rises and reserve balances decrease, there is a potential for liquidity to be drained from the market. The relationship between the TGA and the S&P 500 has been evident over time, suggesting that once the TGA rises again and reserve balances start to fall, the S&P 500 could reverse its trend and move lower.

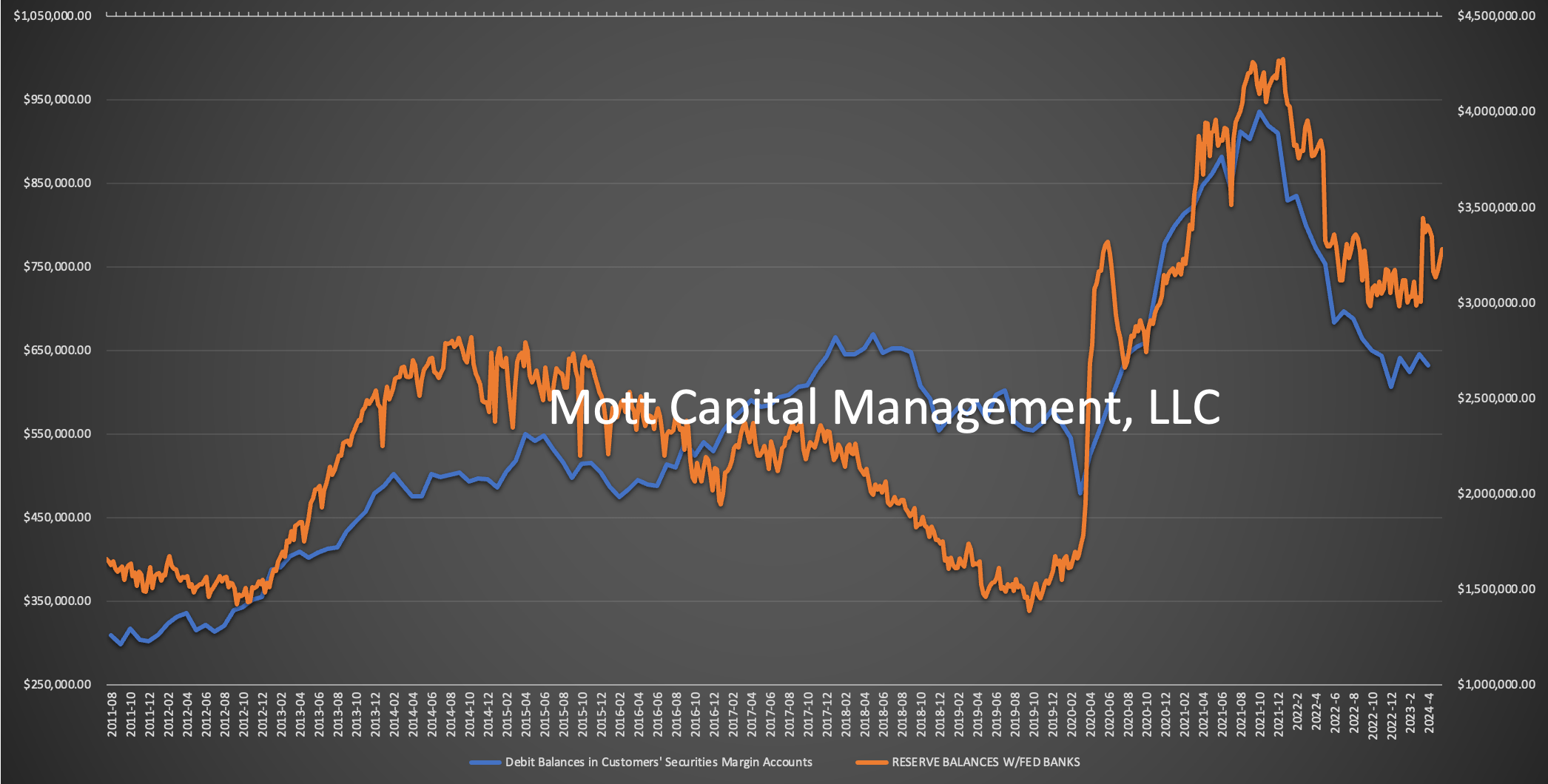

The amount of money flowing back into the TGA and the source of funds used to buy the newly issued debt will play a crucial role in determining the magnitude of the reserve balance decline. This, in turn, could trigger a de-leveraging process. Historical data from FINRA indicates a lasting relationship between reserve balance and margin levels, further supporting this notion.

Mott Capital

As the Treasury General Account (TGA) increases, it represents a liability on the Federal Reserve’s balance sheet. Consequently, an increase in the TGA will likely result in a decline in reserve balances. This decrease in reserve balances can lead to a reduction in margin levels within the market.

When margin levels fall, liquidity is effectively withdrawn from the market, initiating a de-leveraging process. This can impact market participants who rely on margin borrowing to finance their investments. As margin levels decrease, it can create selling pressure and contribute to market downturns.

Mott Capital

Flight-To-Safety

There has been a notable rotation in recent weeks towards mega-cap stocks, which has led to distortions in the movement of indexes, particularly the NASDAQ 100. This is primarily due to the top-heavy nature of the NASDAQ 100, where a few stocks have driven the overall returns. Strong balance sheets, large market capitalizations, significant free cash flows, and robust earnings potential characterize these stocks. Additionally, they are highly liquid and, in some cases, have market caps bigger than some G-7 economies, which may have made them attractive to investors seeking safety amid concerns over interest rate risk.

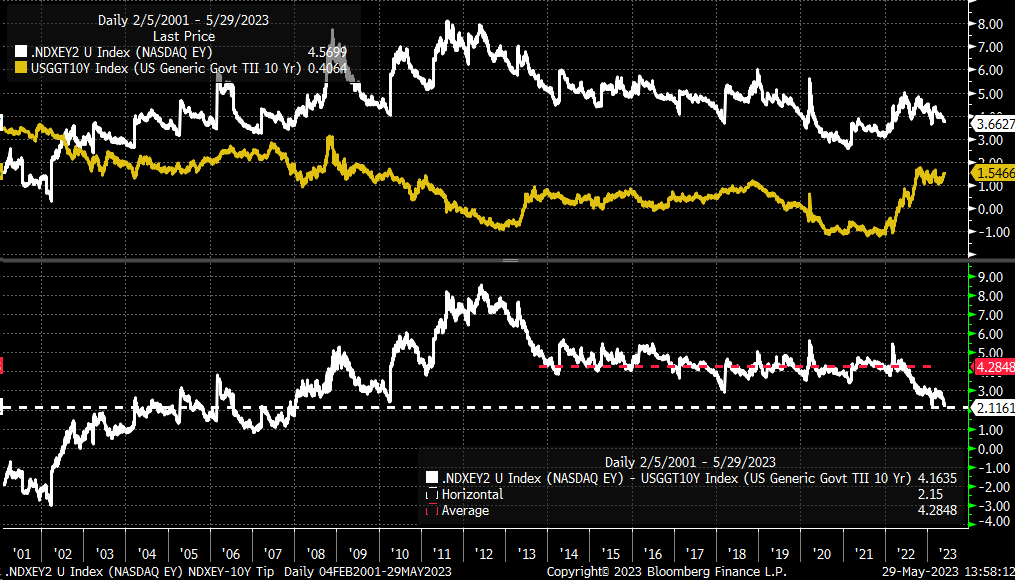

This trend is particularly evident when examining the spread between the earnings yield of the NASDAQ 100 and the 10-year real yield. This spread has reached its lowest level since 2007. The uncertainty surrounding the debt ceiling may have prompted investors to gravitate towards the most liquid and safest assets, which, in this case, appear to be the mega-cap names based on this relationship.

Bloomberg

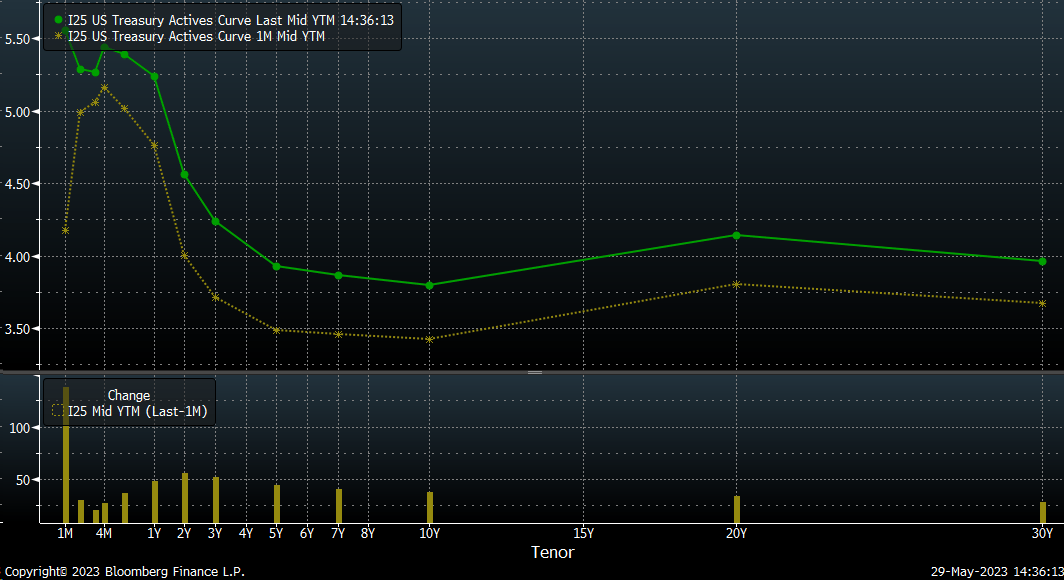

The uncertainty in the market has indeed been reflected in the yield curve, particularly with the significant increase in bond yields at the front end of the curve over the past month. This rise in yields indicates a shift in market sentiment and expectations regarding interest rates.

Bloomberg

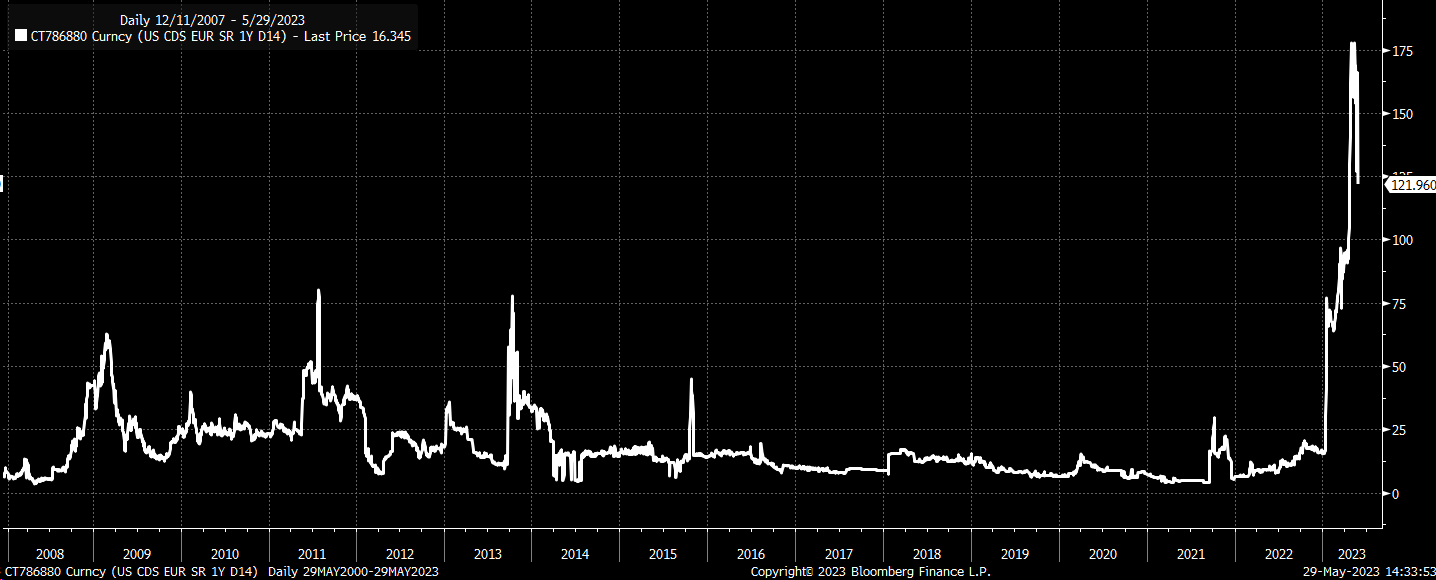

The surge in the 1-year US Credit Default Swap (CDS) to its highest levels clearly indicates heightened market concerns and perceived risk associated with the US defaulting on its debt. The CDS serves as a form of insurance that firms can use to hedge against the possibility of a default.

Bloomberg

However, investors may shift their focus back to the front end of the yield curve, which could lead to a rotation out of the highly liquid and safer mega-cap names. This rotation could result in unwinding the big rally seen in the NASDAQ 100.

Regarding market liquidity, if the unwind of the Treasury General Account leads to a significant increase in the issuance of new debt and the subsequent increase in the TGA, it could potentially drain liquidity from the market.

In this case, the market would be confronted with a deleveraging process and the unwind of a flight to safety simultaneously, which could make the debt ceiling agreement a “sell-the-news” event.