New CEO Won’t Save Lyft (NASDAQ:LYFT)

5./15 WEST

For several years I’ve covered the deterioration of Lyft (NASDAQ:LYFT) stock. In 2020 the obstacles were obvious. Lyft’s core business revolved around transporting people who were told to stay at home. Needless to say, shares have declined nearly 70% since then.

In August 2022 Lyft stock seemed “cheap” given the fact it traded at a transport multiple. However, a turnaround was needed given the strength in Uber’s (UBER) expansion into other verticals and success on the financial side of the business. I recommending selling Lyft shares then, and the stock is down another 52% since then.

Finally, earlier this year in February I questioned Lyft’s turnaround plan. The company is almost purely a one-dimensional ride-sharing company with a dominant competitor in Uber, and plenty of alternatives such as public transportation, or simply driving your own car. Shares of Lyft are down 9% since February.

The deterioration of Lyft’s business has been easy to telegraph. Luckily for anyone that’s put faith into the fledgling ride-share app, the company is finally starting to make some major changes.

New CEO

David Risher, who was a Lyft board member, has been named the new CEO, replacing the co-founders.

The initial reaction was a 5% pop in Lyft shares, which was a reasonable reaction. Often when founder led companies see a change in leadership, some changes are likely coming and investors sometimes assume a sale of the company could follow.

However after a conference call with investors, Lyft shares erased early market gains after the new CEO said Lyft wasn’t for sale and while the company was going to potentially move into other areas of business – it wasn’t certain.

I wouldn’t expect an incoming CEO to immediately declare the company is for sale, so no surprise there. However, with the founders now pushed out of operational control, it could open the door for a sale or strategic partnerships.

From an operational standpoint, as I will go over later, the core ride sharing business simply isn’t compelling enough from an investment perspective. Investors would have preferred a strong message on expansion plans, especially because Mr. Risher is already on the board of Lyft and is keenly aware of the challenges.

As with most CEO changes, the jury will remain out until Mr. Risher is given some time to put his stamp on the company operationally.

Outlook Reaffirmed

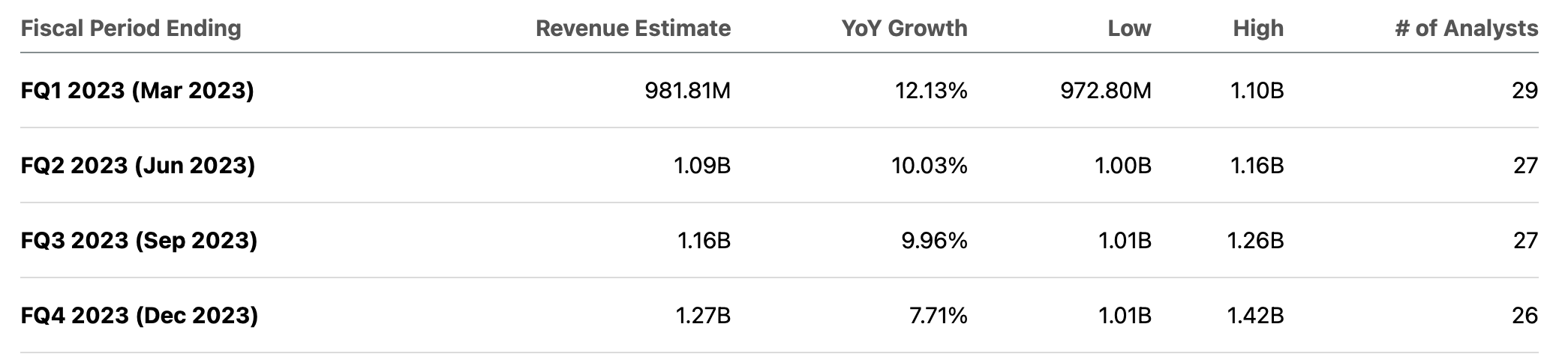

Investors did get some assurance that fundamentally things weren’t deteriorating further after the company reiterated Q1 guidance of $975M in revenue and between $5M-$15M in adjusted EBITDA.

On the revenue side, $975M is actually below the mid-point expectation of $981M. More challenging is subsequent quarters where Lyft’s revenue is expected to slip below a double-digit growth rate.

Seeking Alpha

The profit side is going to be a challenge for Lyft. With a strong competitor like Uber, Lyft has little ability to drive up pricing. The other option is to drive down costs, which the new CEO noted his experience running a non-profit for 13 years gives him some experience “doing more with less”.

Lyft Q4 Press Release

The problem is, Lyft is miles away from operating profits. Looking back at Q4 illustrates the company could reduce costs 42% and return to Q4 2021 levels and still not be profitable.

Q4 Financial Overview

| Q4 2021 | Q4 2022 | % Increase | |

| Revenue | $969.9M | $1.175B | 23.7% |

| Cost of Revenue | $551.2M | $774.4M | 40.5% |

| Operation and Support | $109.9M | $120.7M | 9.8% |

| R&D | $195.0M | $234.6M | 20.3% |

| Sales & Marketing | $123.9M | $130.7M | 5.5% |

| G&A | $263.6M | $510.6M | 93.7% |

| Total Costs & Expenses | $1.24B | $1.771B | 42.8% |

| Loss From Operations | ($273.6M) | ($596M) |

Data Source: Lyft Q4 Slide Deck

Lyft is handcuffed on the cost of revenue side because if the company starts paying drivers less – the drivers simply shift to Uber or another gig. Raise pricing on the consumer end and the same phenomenon happens as users would simply shift to using Uber.

Transformation Needed

Lyft needs to move quickly. The company needs to aggressively move into other markets and/or verticals. Luckily for Lyft, Uber has laid out the blueprint in both areas – it’s confusing why Lyft didn’t follow Uber down the path of food/goods delivery and international markets.

Assuming Lyft does start to move into other verticals, I don’t think it’s a compelling enough investment. Playing second fiddle to Uber hasn’t generated any significant returns for shareholders in ride-sharing, it’s safe to assume food delivery or international expansion wouldn’t produce similar results.

While it’s more likely Lyft goes down a path of transformation, it’s unclear it yields any significant returns for shareholders.

Conclusions

Lyft has historically moved too slowly. The company didn’t expand into low hanging fruit verticals whereas Uber did. That has deteriorated financials and ultimately the stock price.

The core business has no pricing power because Uber is relatively financially healthy and the fact consumers and drivers can move between apps rather easily.

A new CEO might clear the way for some changes to be made, and potentially a sale of the company – but the upside to investors seems limited based on the financials. I would avoid Lyft until the company can prove it can compete.