Doximity: Good Business But Extremely Overvalued (NYSE:DOCS)

Solskin

Investment Thesis

Doximity (NYSE:DOCS) is the most used healthcare social platform in the US, with over 2 million users, representing 80% of US physicians, and 90% of graduating US medical students. Thanks to this large user base of US doctors, Doximity has been able to attract the interest of the best US pharmaceutical companies and hospitals that happily pay the company to promote their products on its platform.

Doximity’s business model was able to generate returns worth of the most famous social media platforms in the world, however, its own strength is also its biggest problem, it’s excessively focused on a small niche.

Despite being expected to triple its revenues and maintain high margins, Doximity is extremely overvalued at today’s prices if compared to an intrinsic value of $13.7 per share.

In today’s analysis, we will assess why Doximity’s business model represents the biggest constraint to the company’s future performance to the point that, at today’s prices, Doximity does not represent a good investment opportunity.

Business Model

Despite having more than 2 million users, Doximity does not generate revenues directly from its user base, which can access Doximity’s services for free, apart from small exceptions like Dialer Pro.

On the Doximity App physicians and medical student can create their own profiles and connect with their peers sharing their thoughts and career developments. The platform is full of medical content with which physicians can stay up-to-date and expand their knowledge. Other than acting as a social media, Doximity offers Digital Fax and eSignature services, with which physician can improve their productivity, and last but not least, directly on the app is it possible to access Dialer, a telehealth solution with which doctors can contact their patients and visit them, both via call and video format, from anywhere in the US.

Revenues are generated from marketing and hiring services offered to pharmaceutical companies and hospitals under a subscription program. Marketing services comprise the promotion of new drugs and clinical trials, to increase healthcare’s brand awareness, as well as digital activities to facilitate the interaction between healthcare institutions and physicians. Hiring solutions instead, leverage on the amount of data about physicians possessed by Doximity, to offer detailed job opportunities on behalf of healthcare institutions.

For a smaller part revenues are generated from Dialer Enterprise and Dialer Pro telehealth solutions. Dialer Pro is offered to physicians that require enhanced capabilities, while Dialer Enterprise permits healthcare institutions to access even more advanced functionalities, like customer management, to better suit enterprise needs.

Operating Performance

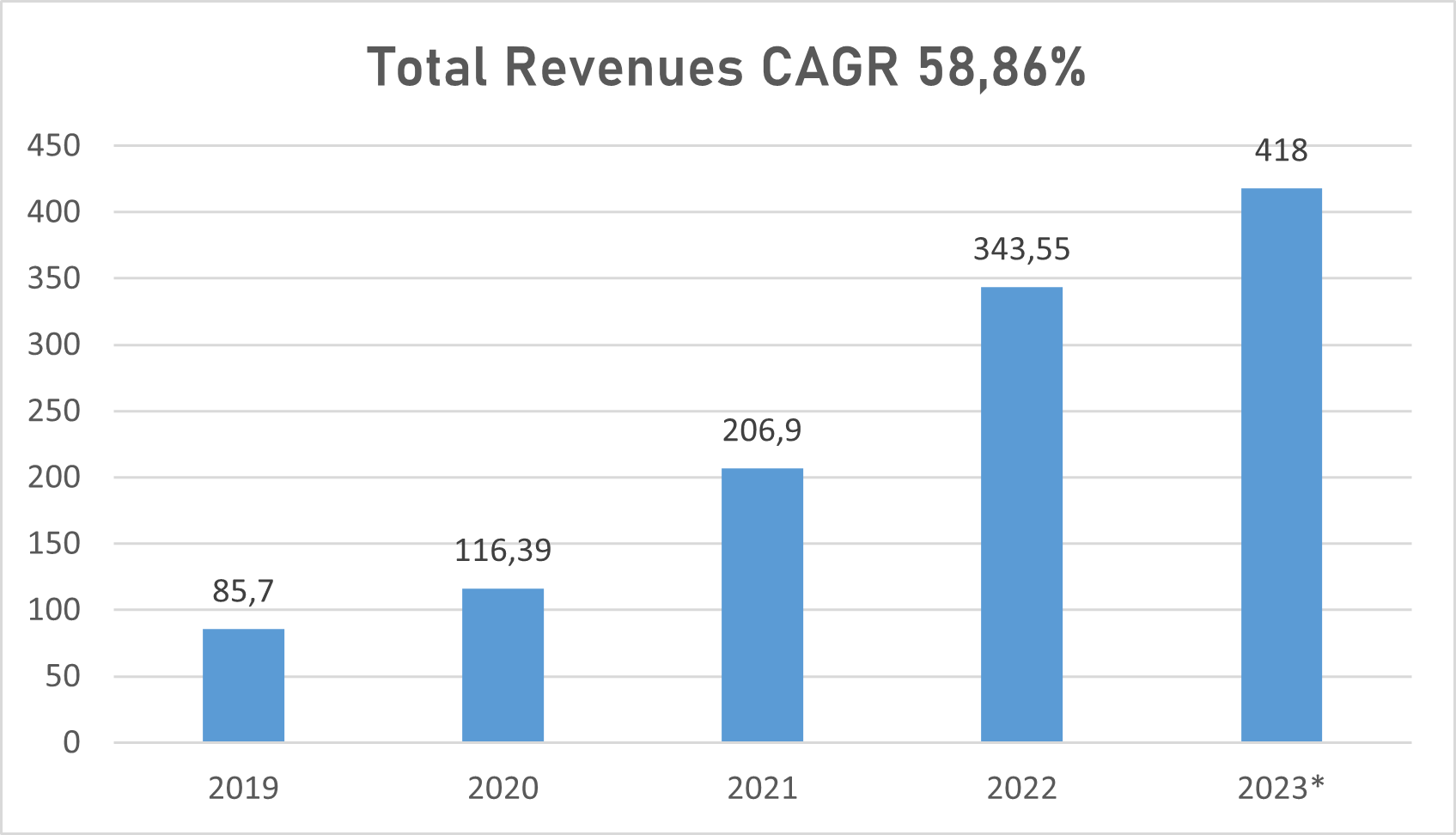

Looking at Doximity’s operating performance, revenues increased from $85 million in the 2019 fiscal year, to $418 million expected for the 2023 fiscal year, a compound annual growth rate (CAGR) of 58.86%.

Doximity’s revenues (TIKR Terminal)

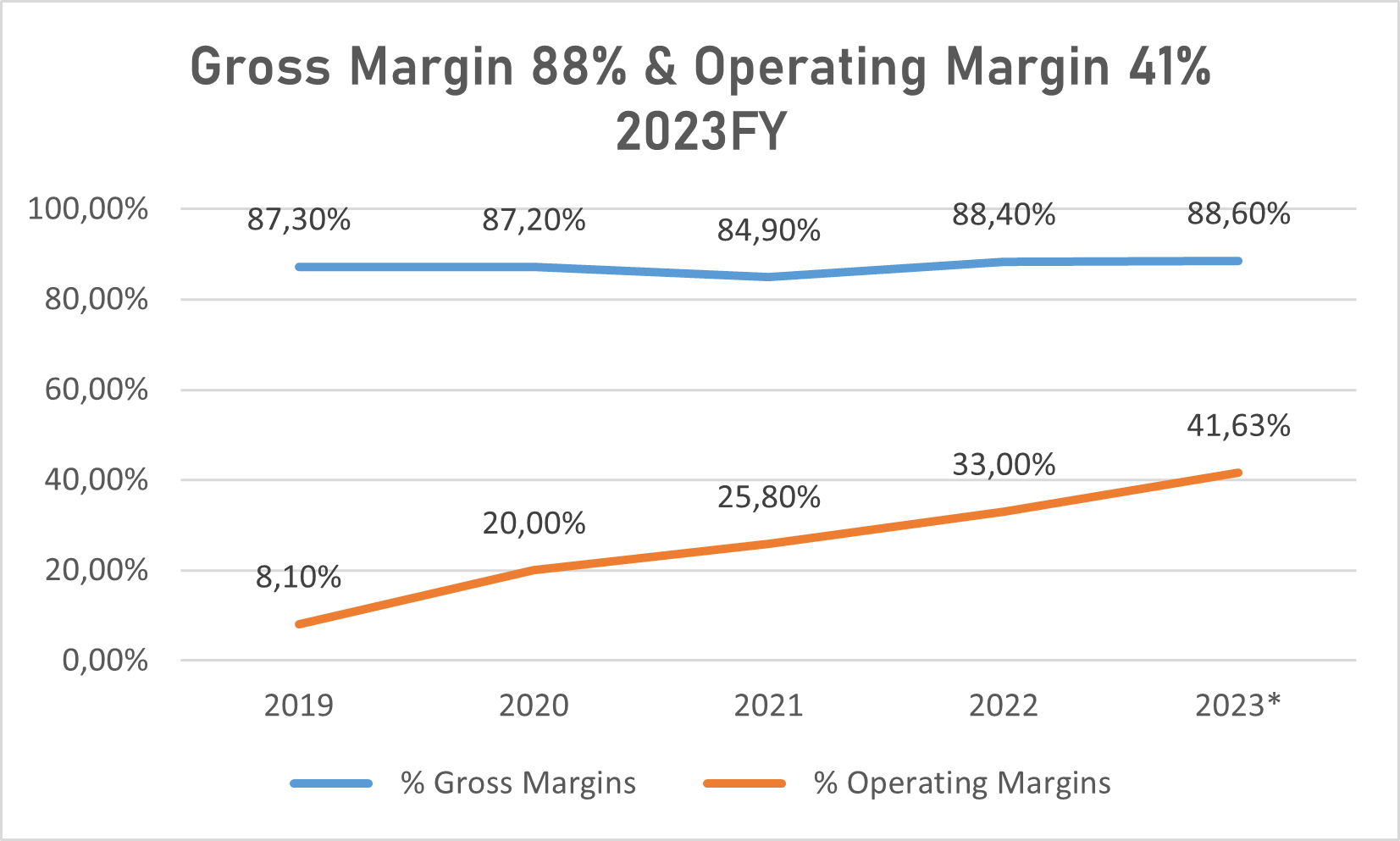

Both the gross margin and the operating margins are excellent, respectively expected to be 88% and 41% in the closing fiscal year, with the operating margin that has been improving in the past four years. The return on invested capital (ROIC) is impressive too, respectively 20% and 18% since the company turned public in 2021.

Doximity gross margin & operating margin (TIKR Terminal)

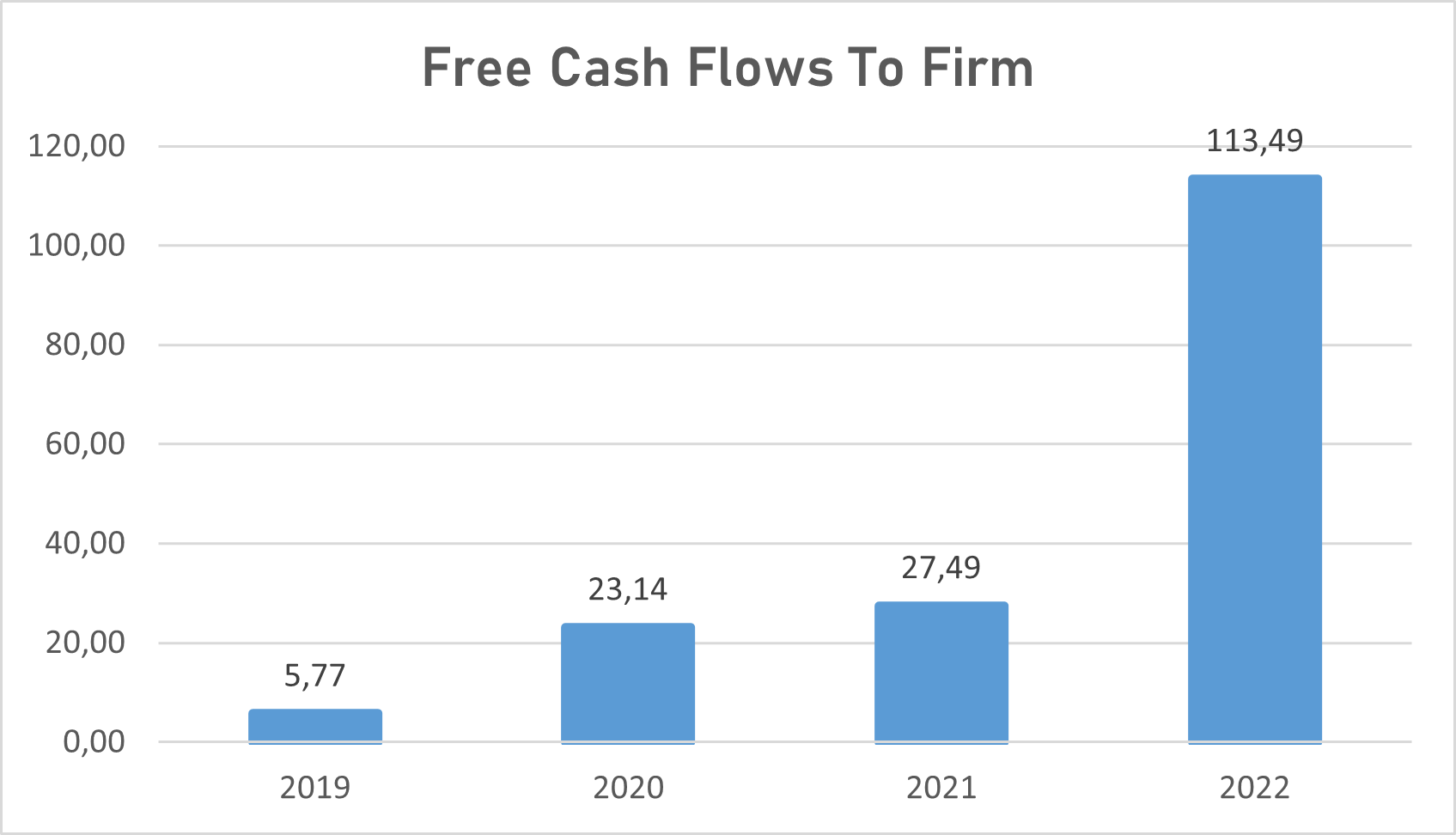

As proof of its strong business model, Doximity grew its free cash flows to the firm (FCFF), from a mere $5.7 million in 2019 to $113 million in the 2022 fiscal year.

Doximity’s FCFF (Personal Data)

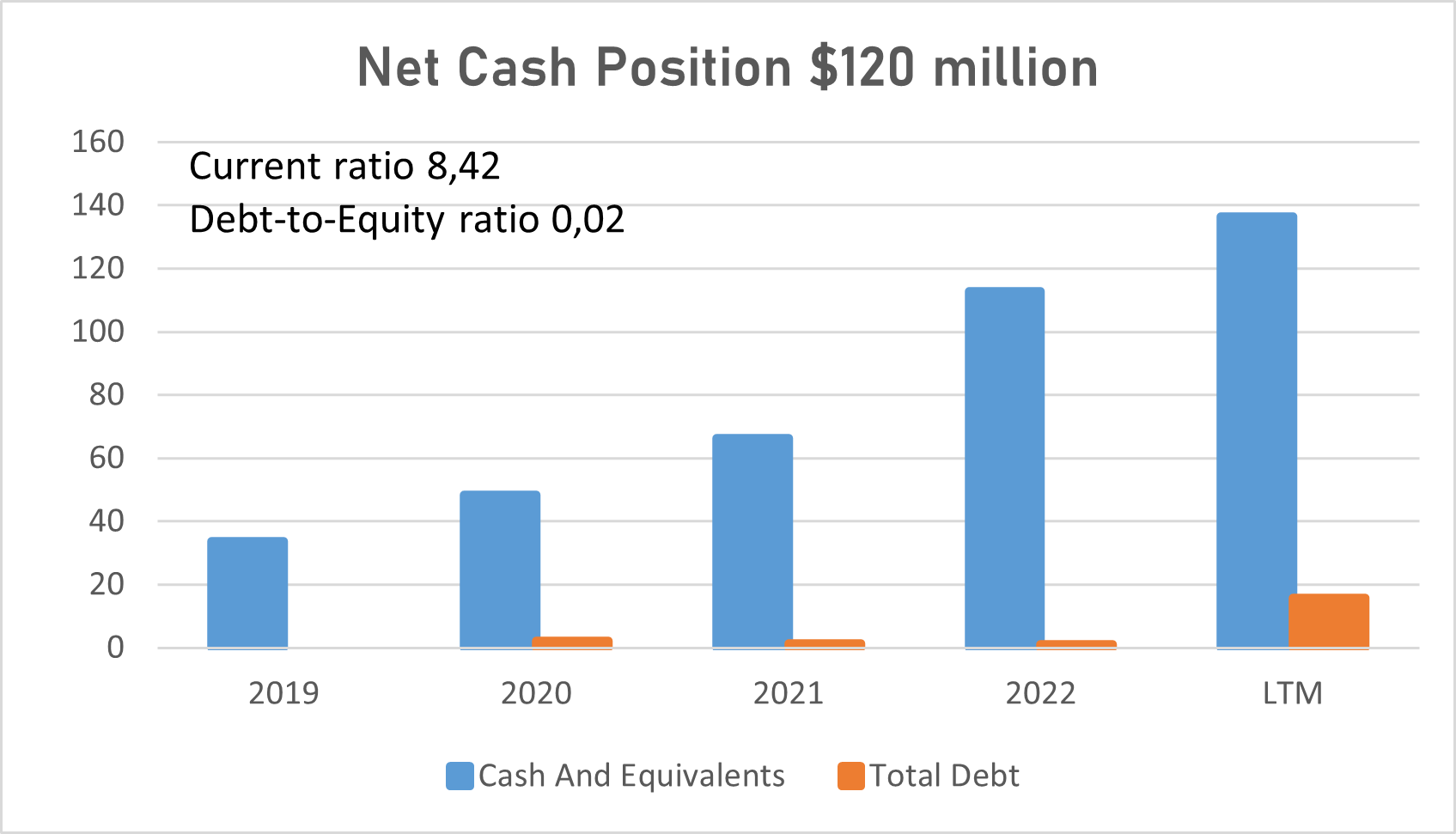

Looking at the financial position of the company, here again, Doximity shows solid results with a net cash position of $120 million, with only $14.5 million in debt outstanding represented by operating leases.

Doximity’s financial position (TIKR Terminal )

Risks

Despite Doximity’s business model proving to be highly successful, the company’s future performance will be curbed by none other than its own business model.

Both the strength and threats of Doximity rely upon the small niche that it’s serving. As a social network platform, Doximity decided to offer its services only to US physicians and graduating medical students, to the point that common people cannot even access the platform, only available for the US market. Thanks to such a focused niche Doximity has been able to attract healthcare institutions willing to pay to reach targeted customers interested in their products. But this focus on such a small niche will limit Doximity’s future opportunities.

There are currently a little more than 1 million physicians in the US, of which 80% are already on the platform, and around 2 million among nurse and physician assistants of which 50% are Doximity users. Even counting for the number of graduating medical students each year, Doximity’s user base cannot be expected to keep growing forever. Even international expansions will be a problem considering the stringent regulations of the healthcare industry.

LinkedIn for example, the most famous social for professional networking, is available all over the world and to every profession, accounting for 875 million users in 2022. Doximity’s business model is very similar to LinkedIn ones, but it’s hard to assume that will reach results even closer to those.

With a limited user base, collecting data will be harder for Doximity, and data are the lifeblood of social network companies that offers advertising services. The more data a company can collect, the more accurate the advertising services are, and the more companies are interested in promoting their products on the platform.

DCF Model

I use the discounted cash flow analysis method to value companies. The aim of a DCF analysis is to determine the present value of expected cash flows generated by the company in the future. The first step is to project the growth rate at which revenues will grow in the future. Secondly, we will need to assume the degree of efficiency and profitability at which the company will turn revenues into cash flows.

Efficiency is represented by the operating margin, and profitability by the ROIC. Having the revenue projections and future operating margins, we obtain the EBIT and, after subtracting taxes, we get the net operating profit after taxes. The ROIC is used to determine the reinvestments needed to support future growth, determining how much profit the company generates from every dollar reinvested into the company.

Future cash flows are calculated by subtracting the reinvestments from the net operating profit after taxes. The higher the growth rate, the higher the reinvestments needed to support it, hence the lower future cash flows will be.

The last step of a DCF analysis is to apply the discount rate to future cash flows, usually calculated using the weighted average cost of capital (‘WACC’).

Projections

Trying to project Doximity’s future performance, we will proceeds using LinkedIn as a base for our assumptions regarding future growth rates, especially looking at LinkedIn before being acquired by Microsoft (MSFT), while as regards efficiency and profitability, we will assume Doximity to keep delivering strong results, leveraging on its focused niche to keep attracting healthcare institutions interested in its products.

Starting with revenues, one of the best assumptions we can make is to assume Doximity to reach revenues on par with LinkedIn ones. Of course, assumptions are based on LinkedIn’s performance pre-Microsoft acquisition, when it still was a relatively small company and not the giant it is now. That’s because we assume Doximity to remain a niche platform going into the future. In addition to that, we will use only LinkedIn revenues generated in the US by marketing and hiring solutions, that perfectly replicate Doximity’s business lines.

LinkedIn past performance (Bloomberg Terminal)

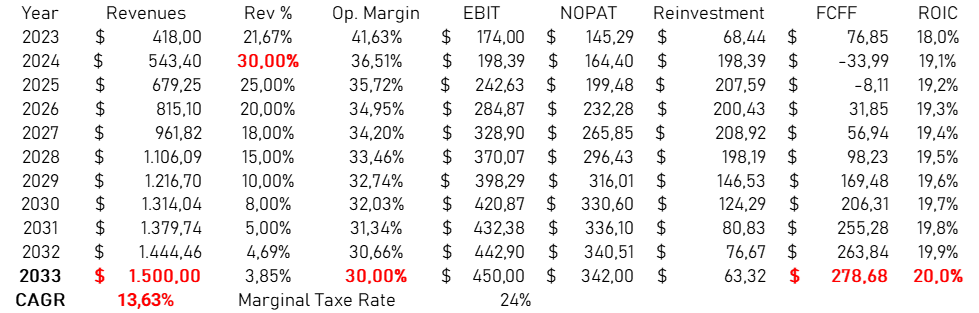

Therefore, we can assume Doximity to reach revenues of around $1.5 billion by 2033 before entering its steady state, equal to the revenues generated in the sole US market by LinkedIn by its marketing and hiring solutions back in 2015. Revenues are expected to triple in ten years at a CAGR of 13.6%.

In my opinion, $1.5 billion represent one of the best outcomes for Doximity, considering that LinkedIn at that time, other than offering its services to a broader range of professionals, had 125 million users in the US, a user base not reachable by Doximity.

Moving on to efficiency and profitability, we can expect Doximity to maintain its high operating margins and ROIC going into the future, as it will keep attracting pharmaceutical companies and hospitals thanks to its unique platform perfectly suited to promote their products. The operating margin is expected to be around 30% by 2033, lower than current levels assuming that competition will increase among other online advertising companies, while the ROIC is expected to remain around 20%, as Doximity doesn’t require heavy investments in capital.

With these assumptions, Doximity’s FCFF are expected to be around $280 million by 2033.

Doximity’s future performance (Personal Data)

Valuation

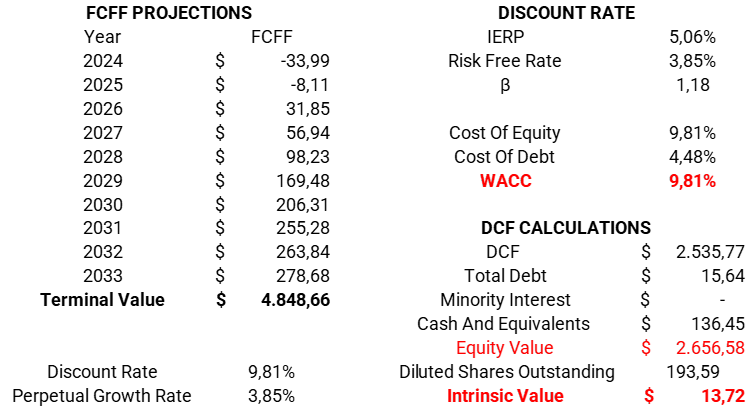

Applying a discount rate of 9.81%, calculated using the WACC, the present value of these cash flows is equal to an equity value of $2.6 billion or $13.72 per share.

Doximity’s intrinsic value (Personal Data)

Conclusion

Given my analysis and assumptions, Doximity stocks result to be highly overvalued at today’s prices.

Even assuming Doximity’s revenues to triple and maintain efficiency and profitability levels on par with advertising companies like Meta Platforms (META) and Google (GOOGL), Doximity’s business model is too narrow and specific to permit the company to expand immensely in the future.

Given these stringent constraints, which limit the assumptions we can make about the company’s future and badly affect its intrinsic value, its current stock price doesn’t permit Doximity to be considered a good investment opportunity.