DCP Midstream, LP: 8% Floating Rate Preferreds With Strong Coverage (NYSE:DCP.PB)

HAYKIRDI

Looking to take advantage of rising rates? As Fed Chief Powell said this week, the Fed isn’t done raising rates, which means that floating rate investments could be a good way to go with the flow in 2023.

This article covers two Energy sector preferreds:

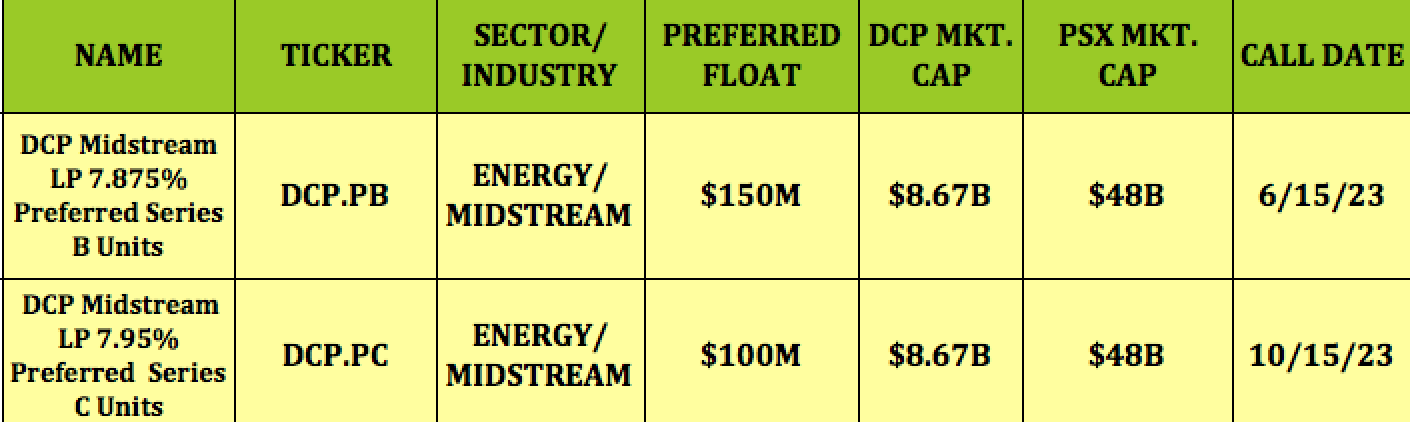

-DCP Midstream LP 7.875% Preferred Shares Series B Units (NYSE:DCP.PB)

-DCP Midstream LP 7.95% Preferred Shares Series C Units (DCP.PC)

Company Profile:

DCP Midstream LP (DCP) is a Fortune 500 natural gas company with a diversified portfolio of logistics, marketing, gathering, and processing assets across 9 states. Headquartered in Denver, Colorado, we are one of the largest natural gas liquids producers and marketers, and one of the largest natural gas processors in the US. (DCP site)

DCP site

Buyout:

DCP reached an agreement with Phillips 66 (PSX) in early January 2023, in which PSX agreed to buy all of DCP’s common units for $41.75/unit, increasing its economic interest in DCP Midstream to 86.8%. The transaction is expected to close in the second quarter of 2023.

Preferreds’ Profiles:

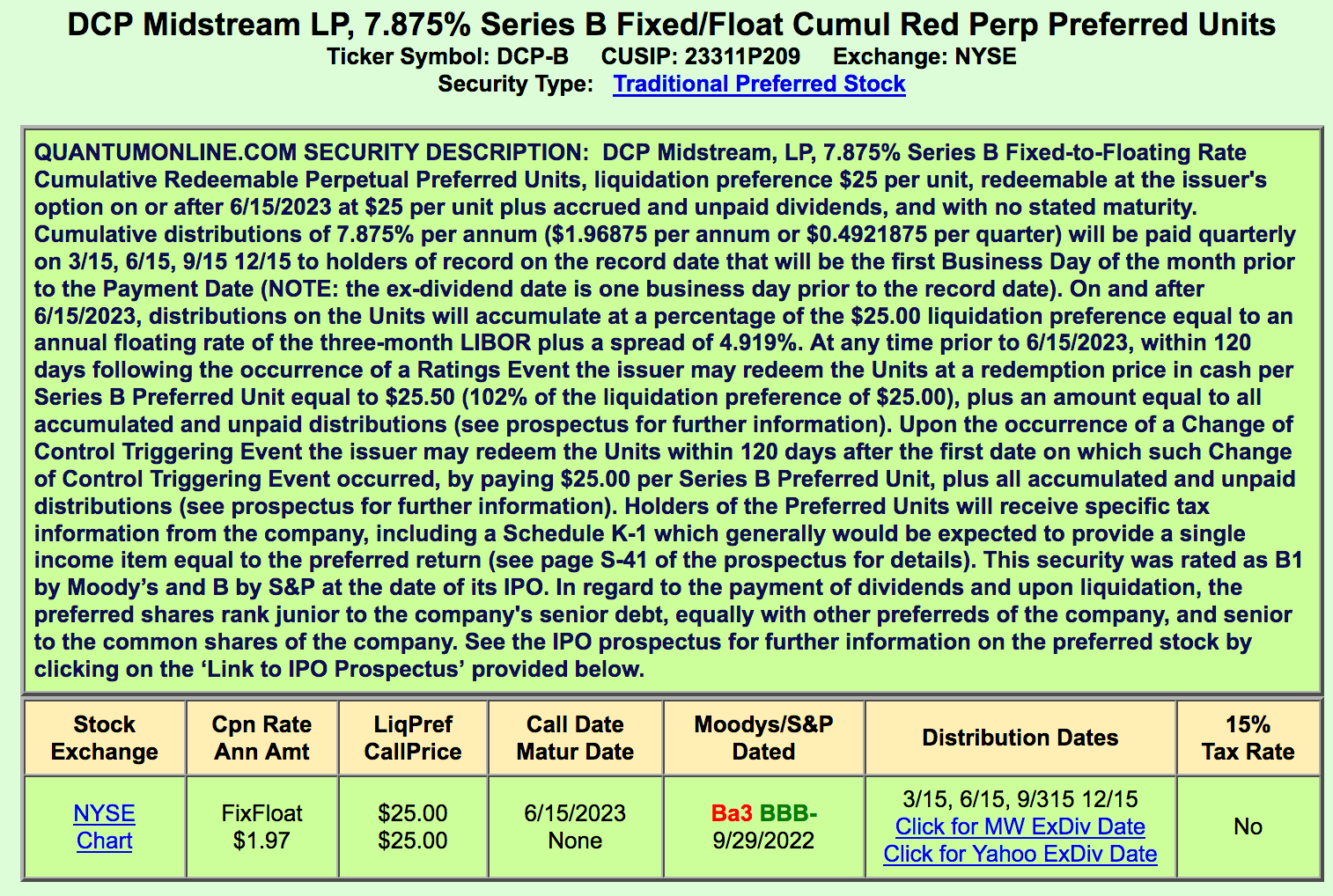

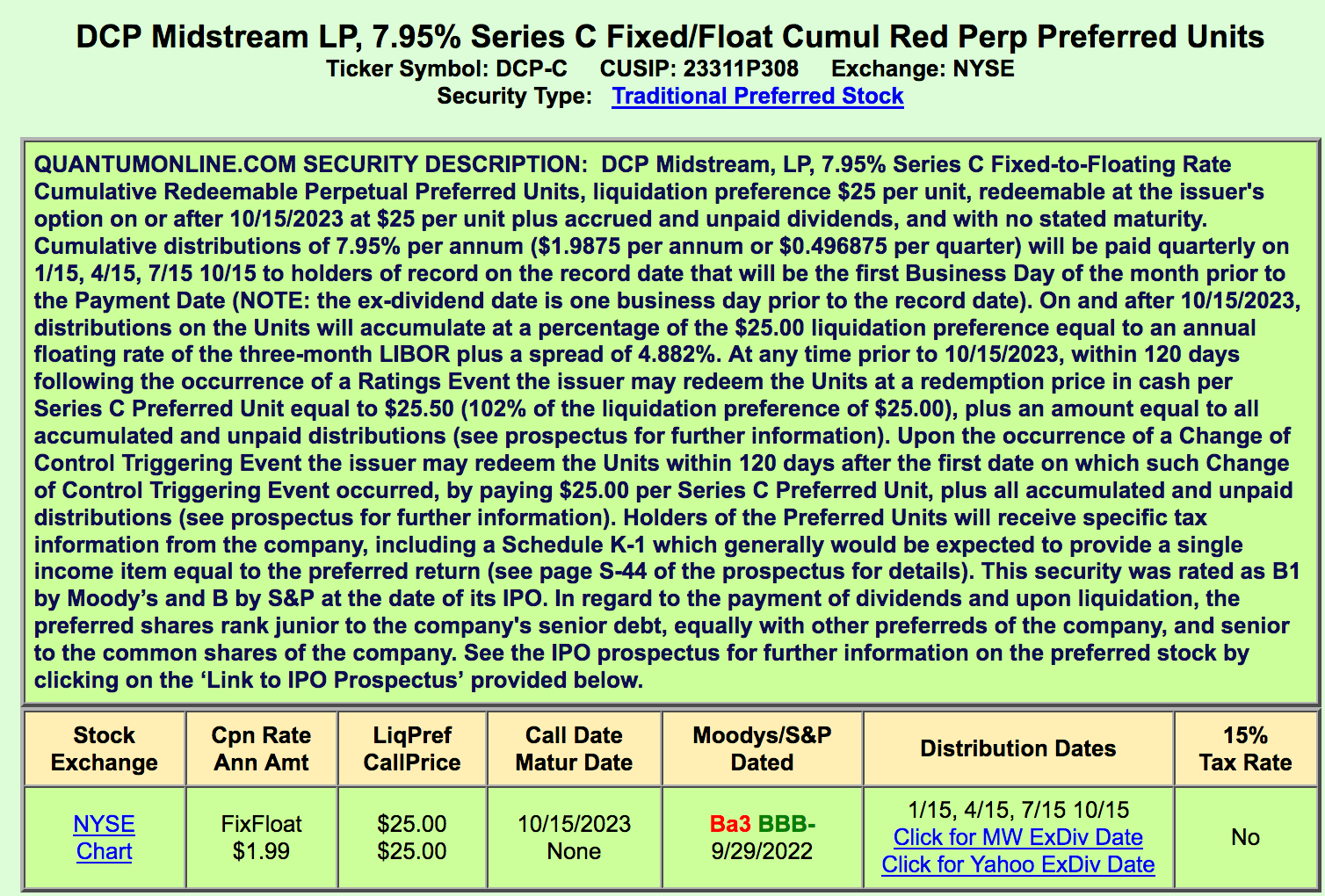

DCP-B is the larger of the two issues, with a $150M float, vs. $100M for DCP-C. DCP-B also enters its floating period sooner, on its 6/15/2023 call date, whereas DCP-C’s floating rate period doesn’t start until its 10/15/2023 call date.

PSX has a $48B market cap, vs. $8.67B for DCP:

Hidden Dividend Stocks Plus

These are both cumulative units, meaning that DCP must pay you for any skipped distributions, before paying any common distributions. However, in light of the PSX pending buyout, there’s an additional wrinkle, in that, the buyout would mean a change in control of DCP. In that case, they could redeem them within 120 days after the buyout deal closes for $25.00, plus all accumulated unpaid distributions.

qntmnln

DCP-C has a slightly higher dividend yield, of 7.95%, vs. 7.875% for DCP-B.

qntmnln

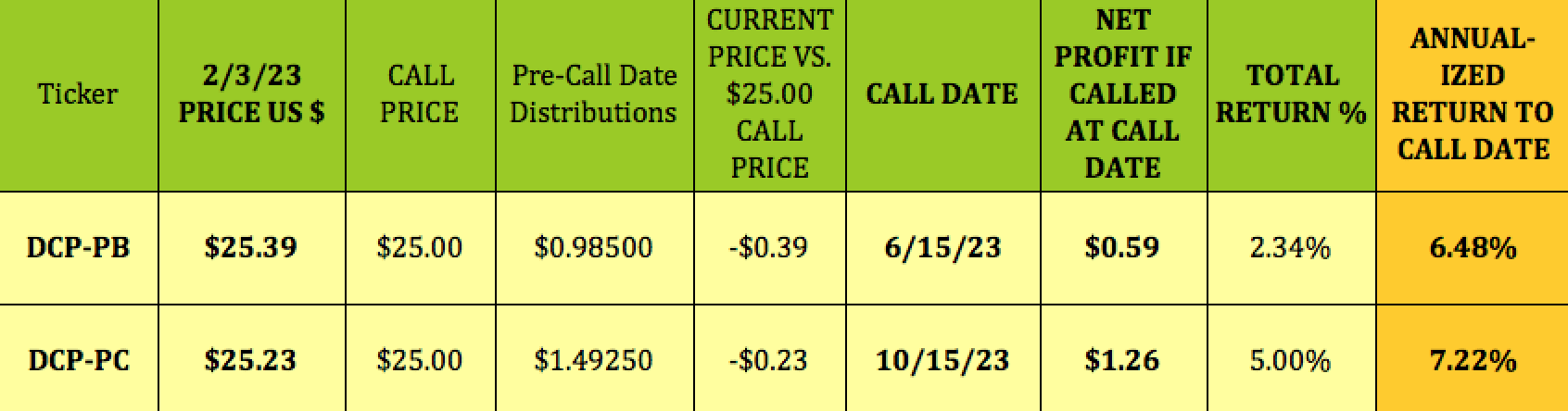

Here’s a breakdown of the potential net profit if these units were to be redeemed on their call dates.

DCP-B has two more distributions prior to its 6/15/2023 call date, allowing for 2 more quarterly distributions, for a total of $.985/unit. With the price at $25.39, $.39 above the $25.00 call price, your net profit would be $.59/unit if they were to be called on 6/15/2023. The total return would be 2.3% in ~4.5 months, or ~6.5% annualized.

DCP-C has three more quarterly distributions prior to its 10/15/2023, totaling $1.26/unit. The net profit would be $1.26/unit, as these units are $.23 above their $25.00 call rate. The total return would be 5% in ~8.5 months, or ~7% annualized.

Hidden Dividend Stocks Plus

Dividends:

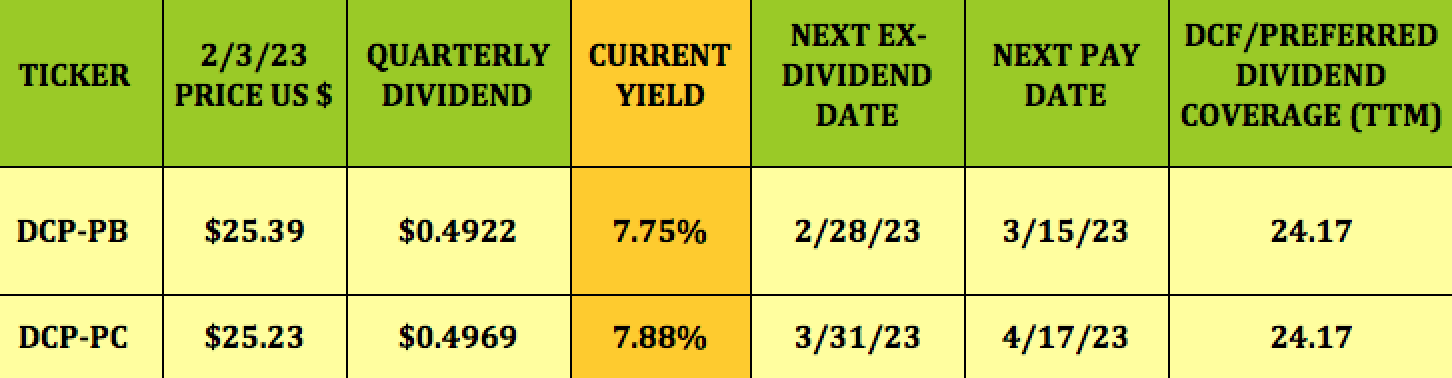

At its 2/3/23 price of $25.39, DCP-B yields 7.75%. It pays $.4922/quarter and goes ex-dividend next on 2/28/23, with a 3/15/23 pay date.

DCP-B pays $0.4969/quarter and yields 7.88%. It goes ex-dividend next on 3/31/23, with a 4/17/23 pay date.

Hidden Dividend Stocks Plus

DCP-B’s floating rate of 4.919% is a bit higher than DCP-C’s 4.882% rate. With the 3-Month LIBOR rate currently up to 4.81%, (vs. just .30% a year ago), DCP-B’s total rate would be 9.73%, if the 3M LIBOR rate is 4.81% from 6/15/2023 onward. Since its price is $25.39, though, the equivalent future yield would be a bit lower, at 9.58%, still quite attractive.

DCP-C’s total rate would be 9.69% if the 3M LIBOR rate is 4.81% from 10/15/2023 onward. Its equivalent future yield would be 9.60%, similar to DCP-B’s yield.

Hidden Dividend Stocks Plus

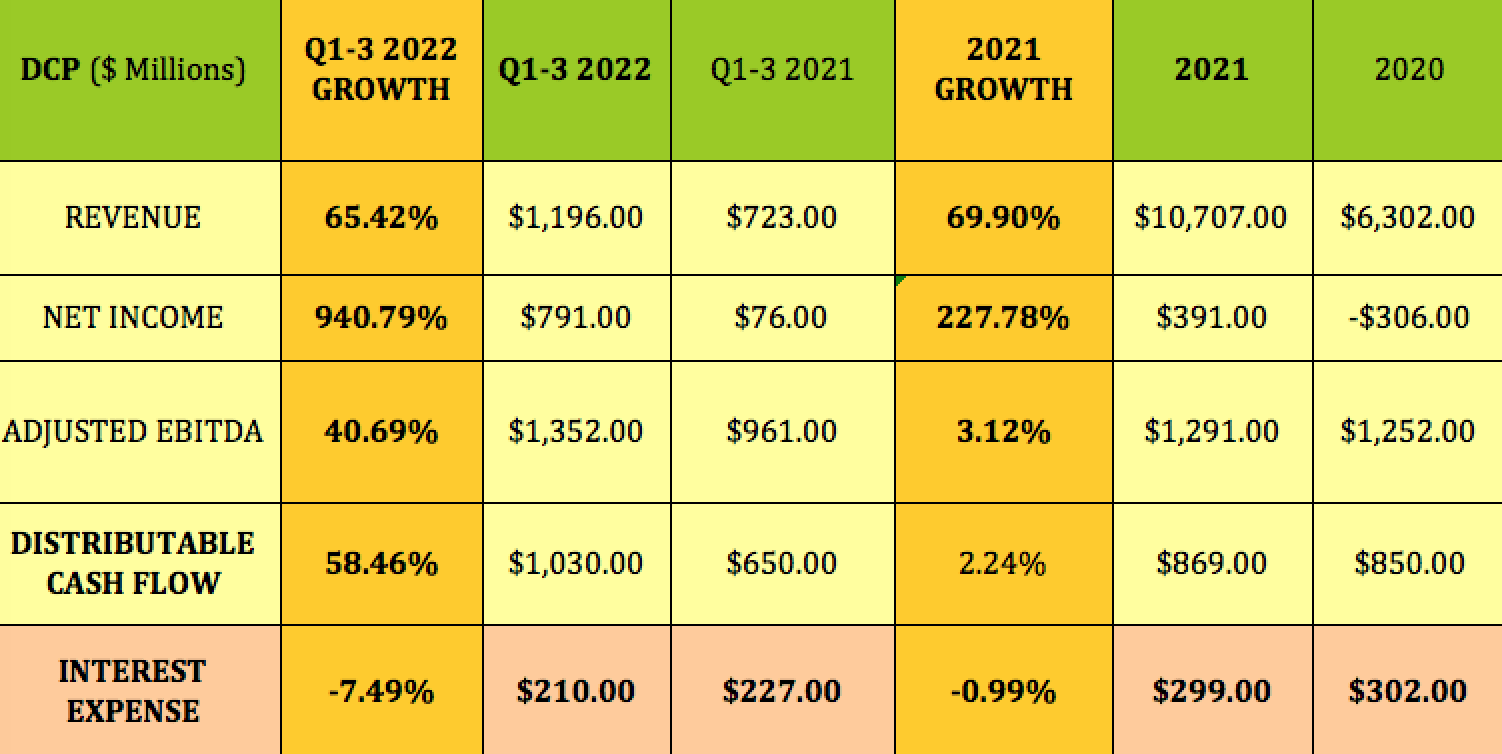

DCP’s preferred distribution coverage was steady in 2020 and 2021, with DCF coverage of over 15X. DCF preferred distribution coverage ramped up 54% in Q1-3 ’22 to a very strong 23.89X factor, and is 24.17X on a trailing basis.

Distributable Cash Flow, DCF, adds back non-cash Depreciation and Amortization expenses, which are considerable for midstream industry companies.

Even using Net Income/Preferred Distributions as a measurement, preferred distribution coverage was a strong 17.58X in Q1-3 ’22.

Hidden Dividend Stocks Plus

Taxes:

Unitholders receive a K-1 report at tax time for these preferreds.

Earnings:

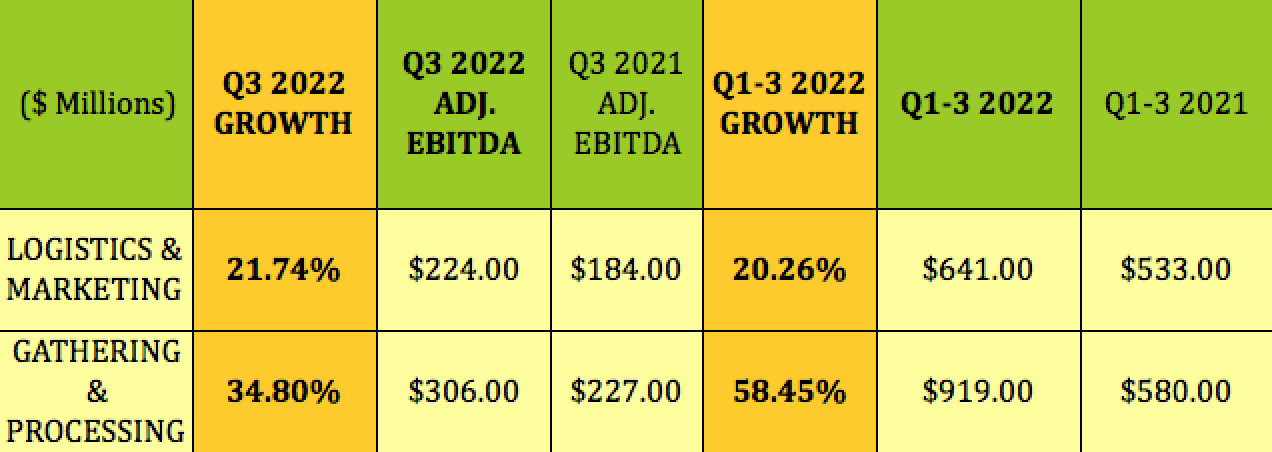

DCP’s Logistics & Marketing segment continued its strong growth in Q3 ’22, with Adjusted EBITDA rising ~22%. Q1-3 EBITDA was up ~20%. The Gathering & Processing segment is the more profitable of the two – its EBITDA rose ~35% in Q3 ’22, and was up ~58% in Q1-3 ’22:

Hidden Dividend Stocks Plus

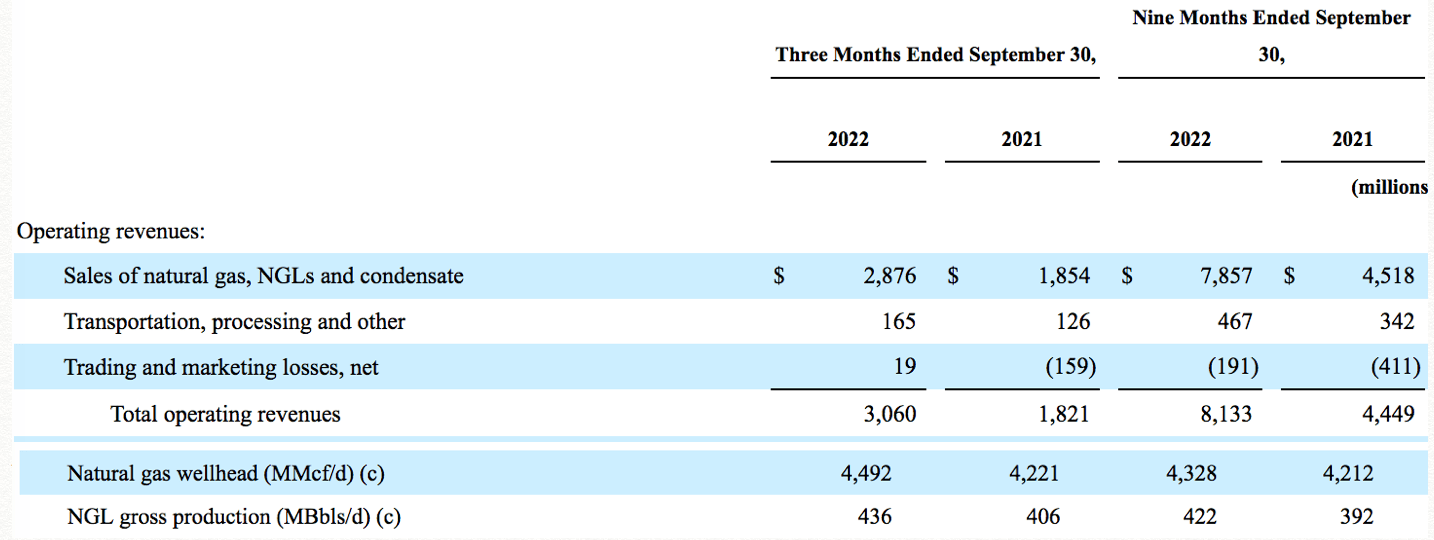

Logistics & Marketing had 56% of DCP’s total operating revenues in Q3 ’22, with revenues rising 44%. Gathering & Processing revenues surged 68%, to $3.06B in Q3 ’22, and were up 83% in Q1-3 ’22:

DCP site

Natural Gas, NGL’s, and condensate sales rose 55% in Q3 ’22, and were up 74% for Q1-3 ’22. Natural Gas volume accelerated in Q3 ’22, rising 6.4%, vs. ~3% in Q1-3 ’22. NGL production volumes had ~7.4% growth in Q3 ’22, and ~7.7% in Q1-3 ’22:

DCP site

Q1-3 ’22: Overall Revenues rose ~65%, almost in line with 2021’s torrid 60% growth rate, while Net Income surged over 9X. Adjusted EBITDA rose over 40%, and DCF rose over 58%, vs. just 3% and 2% in 2021, respectively.

Interest expense also improved, declining by 7.5%:

Hidden Dividend Stocks Plus

Profitability and Leverage:

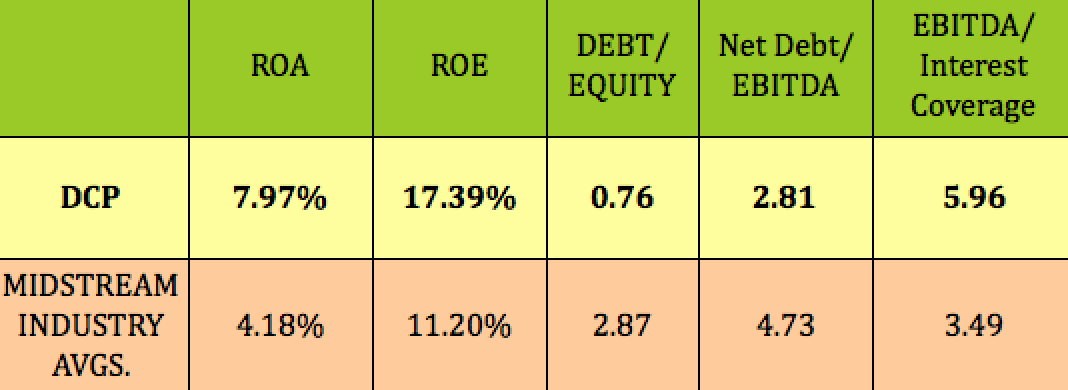

DCP’s trailing profitability and leverage figures are much better than midstream averages. Its 0.76X debt/equity and 2.81X net debt/EBITDA leverage figures are some of the lowest we’ve seen in this industry.

Hidden Dividend Stocks Plus

Debt and Liquidity:

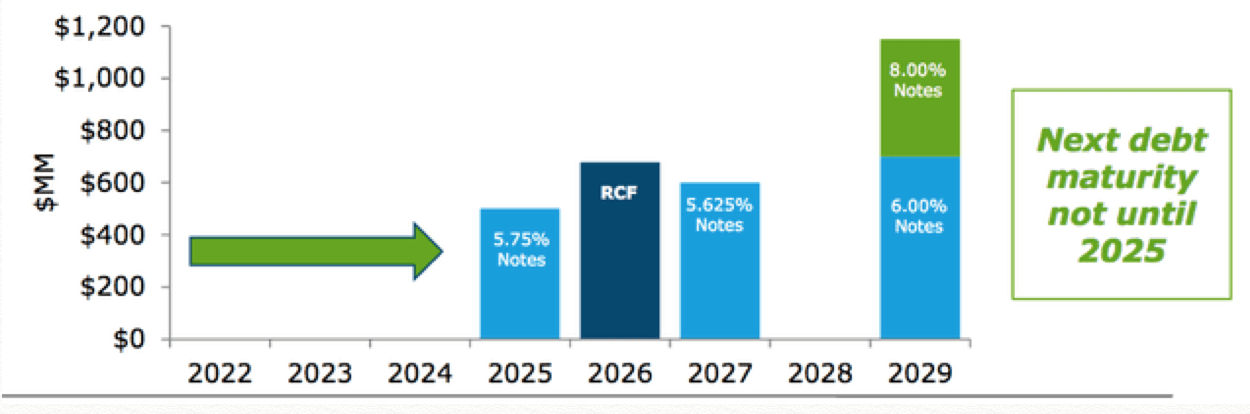

DCP has no debt maturing until 2025.Management reduced absolute debt by over $300M in the third quarter, and by over $600M year to date. It had ~$1.83B in liquidity, comprised of $93M in cash, and $1.7B in available credit, as of 9/30/23.

It received an upgrade from S&P to investment grade, and Moody’s updated rating outlook rose to positive from stable.

DCP site

Performance:

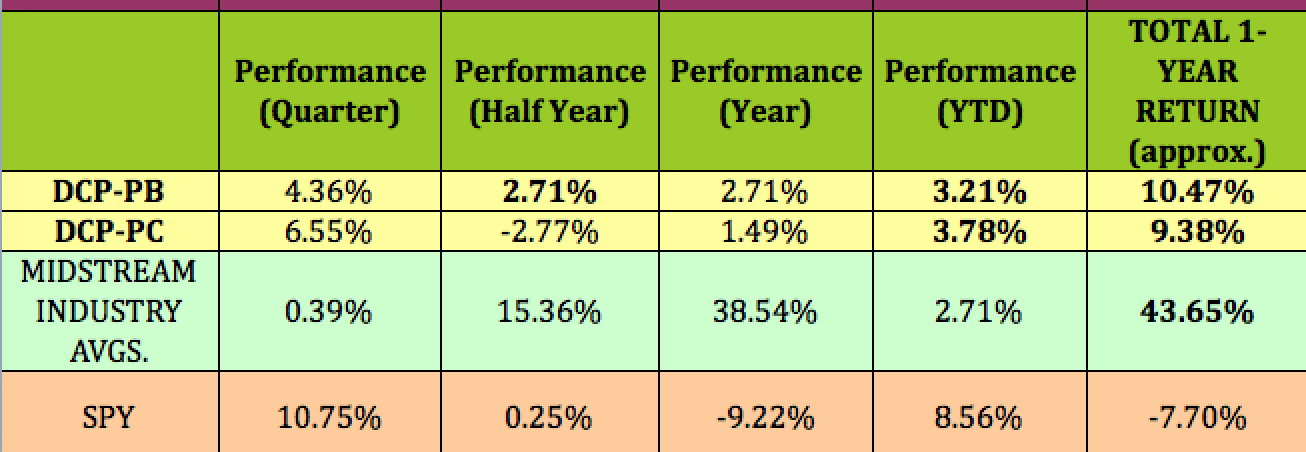

The two units have flip-flop performance in the time periods below, with DCP-B having a total 1-year return of ~10.47%, vs. 9.38% for DCP-C, but DCP-C outperforming DCP-B more recently, over the past quarter, and so far in 2023.

Hidden Dividend Stocks Plus

Parting Thoughts:

We reached out to DCP’s investor relations department for more info on how the PSX deal will affect the DCP preferreds, which we’ll post here in the comments section as they become available. PSX has investment grade credit ratings of A3/BBB+.

We rate both DCP-B and DCP-C as BUYS, with DCP-C holding a slight edge, since its call date isn’t until October, giving unit holders more time for collecting quarterly distributions, and bringing their breakeven further below $25.00.

The main risk is that these preferred units are redeemed within the 120 day change of control period following the targeted Q2 ’23 buyout closing date. If you want to be more conservative, wait for a market selloff, when you may be able to buy them under $25.00.

All tables furnished by Hidden Dividend Stocks Plus, unless otherwise noted.