Clarus Stock: Cash Crunch Needs To End Fast (NASDAQ:CLAR)

IvelinRadkov

Intro

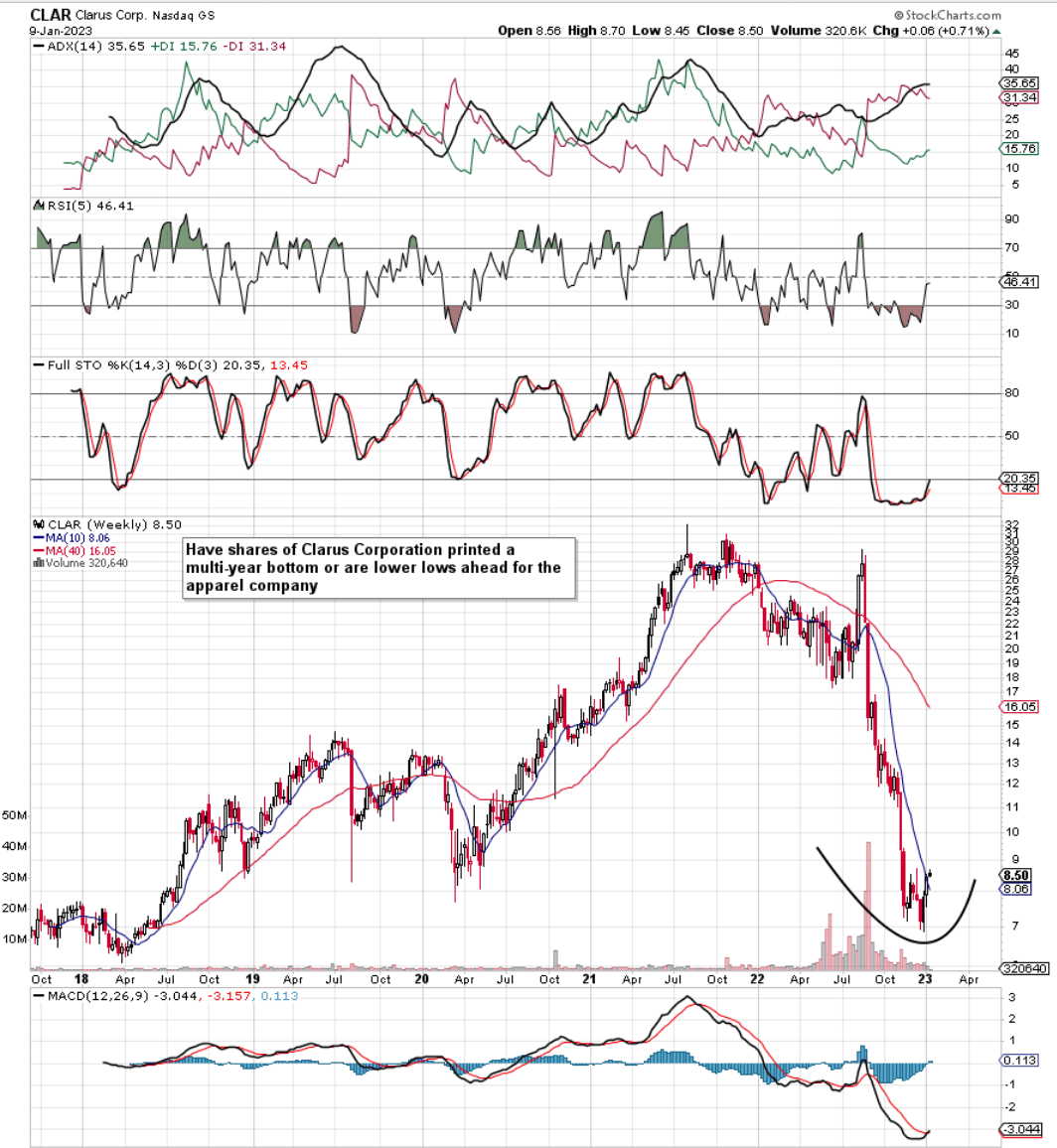

As we can see below, fiscal 2022 was a horrible year for apparel manufacturer Clarus Corporation (NASDAQ:CLAR), although green shoots may be finally beginning to appear in the stock. As we can see from the intermediate chart below, shares have now delivered a tentative buy signal through the MACD indicator due to price having rebounded above the stock’s 10-week moving average. Furthermore, the MACD’s histogram move into positive territory may be another sign that the worst is over for Clarus Corporation.

Therefore, considering Clarus’ ultra-oversold conditions, we can gauge whether a sustained move to the upside may be in play here by going through the company’s key metrics which make up the dividend. If there is a path to sustained growth in the payout through internally driven earnings & cash flow, then the share price should move up accordingly all things remaining equal.

Clarus Technical Chart (Stockcharts.com)

Profitability

Dividends come from earnings (which consequently generate cash), and dividends simply cannot be sustained unless a robust earnings trend is there to meet those payments over time. Net profit in Clarus‘ fiscal third quarter came in at $2.8 million as higher freight costs, unfavorable forex trends, and a poor showing from the Adventure segment led to a poor comparable (bottom-line figure of $4.5 million in Q3 last year).

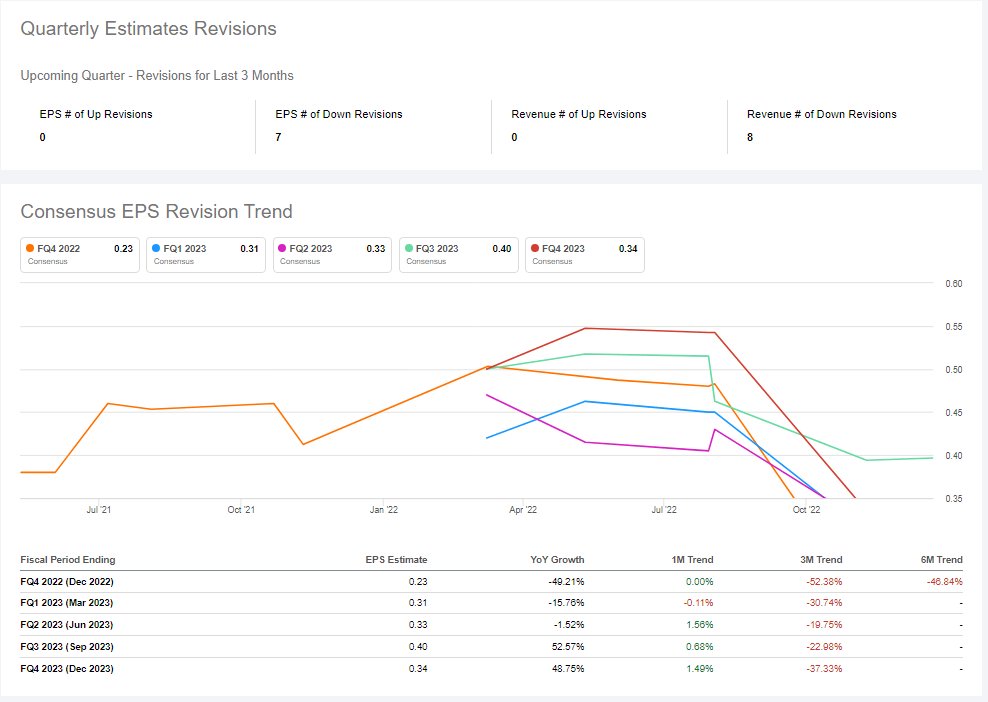

Given that sales increased by 6% in the third quarter over the prior-year quarter due in part to the Maxtrax acquisition, the Q3 bottom-line print this year was poor, to say the least. Furthermore, as we see below, forward-looking earning revisions continue to be dialed down by analysts who follow this name with the upcoming fourth quarter expected to report a sequential bottom-line decline (Normalized Q4 estimate of $0.23). From a dividend perspective, the payout (quarterly sum of $0.025) remains well-covered at least from an earnings standpoint.

Clarus Forward Looking Quarterly EPS Estimates (Seeking Alpha)

Cash-Flow

Since the income statement however contains many non-cash costs, it doesn’t always give us an accurate picture of the viability of the dividend. That above-mentioned net profit tally of $2.8 million did not manage to convert into positive operating cash flow where $11.6 million was actually shelled out in the quarter. Moreover, when one adds the $2.1 million of capital expenditure spent in Q3, free cash flow came in at a disappointing -$13.6 million for the third quarter.

Therefore, the dividend cash-flow pay-out ratio was nonexistent in Q3 as elevated inventory and accounts receivables resulted in not enough cash being available to balance the books. Suffice it to say, management had two points in this scenario. Drain down the cash balance to cover the shortfall or issue more debt to balance the books. Management decided to issue $37.1 million in debt to cover the shortfall, which obviously had ramifications for the balance sheet as we see in the next section.

Balance Sheet & Value

Long-term debt rose to $156.9 million in the third quarter, which means Clarus’ debt-to-equity ($363.1 million) ratio came in at 0.43 at the end of the company’s third quarter. Given that Clarus’ reported equity remains higher than the company’s market cap ($314+ million), the stock at present is trading under its stated book value (P/B ratio of 0.85).

However, when we delve into the company’s balance sheet, we see that inventory ($156.9 million), Goodwill ($112 million) & other intangible assets ($176 million) make up 70%+ of the company’s assets. These elevated percentages definitely bring risk to Clarus stated equity, as their stated values may not be realized over time. Suffice it to say, Clarus’ trailing interest coverage ratio of 5.89 will continue to collapse if earnings growth and leverage continue to go in opposite directions.

Conclusion

Clarus Corporation management’s expectation of positive cash-flow generation needs to take place in order for the bleeding to be stopped here. Margins are under pressure, and the piling up of debt only adds more risk to a balance sheet that is already overextended. Sales growth is a secondary issue at this stage, as gross margins continue to come under pressure from sky-high freight costs as well as supply-chain inefficiencies. If the Clarus Corporation cash crunch indeed continues, a dividend cut would be on the cards here. We look forward to continued coverage.