What I Learned From My Biggest Losers Of 2022

RichVintage

Over the long run, our real estate investment trust (“REIT”) investing strategy at High Yield Landlord has generated very attractive rates of return.

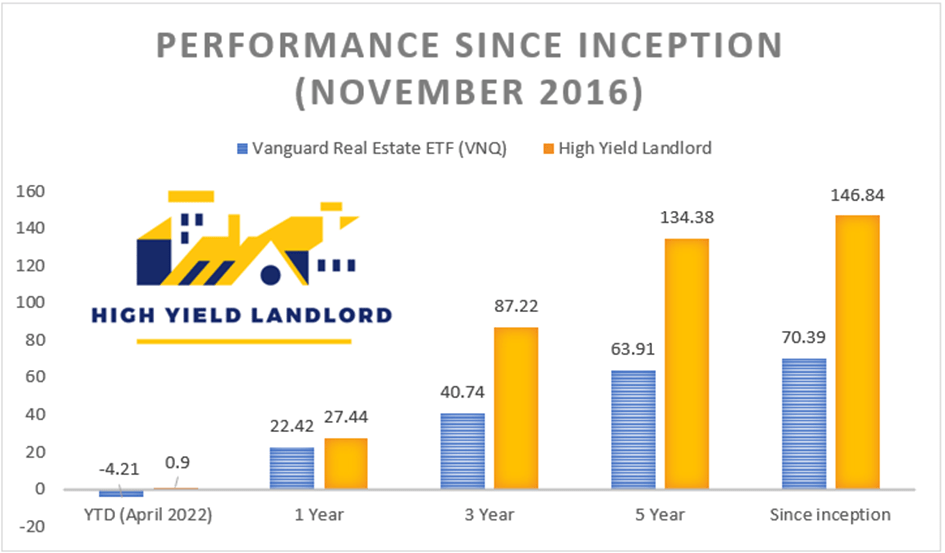

In late 2016, I decided to move all my real estate investments to Interactive Brokers to start building a track record that could come in handy later on as I become a professional REIT analyst. Since its inception up until the recent market correction, it had returned a total of 146.84%, which averages out to ~18% per year. In comparison, the relevant REIT exchange-traded fund (“ETF”) (VNQ) returned 70.39%, which averages out to ~10% per year over this time period:

High Yield Landlord performance until recent correction

But then, the REIT market suddenly dropped by ~30%, and as you would expect, it brought down our portfolio to much lower levels.

The 30% drop was the performance of the market-cap weighted REIT ETF VNQ that mainly invests in large-cap, investment grade rated REITs.

So you can imagine that many REITs must have dropped a lot more.

Some that lacked an investment grade rating dropped by closer to 50%!

And unfortunately, since we don’t have a crystal ball, we also suffered some of those losses.

In most cases, we think that these steep corrections are at least partly unwarranted. The market has the tendency to correct too much and rapidly bounce back later.

But rather than dismiss this poor performance as just “volatility,” let’s review some of our biggest losers to see if there is anything we can learn from them:

BSR Real Estate Investment Trust (OTCPK:BSRTF)

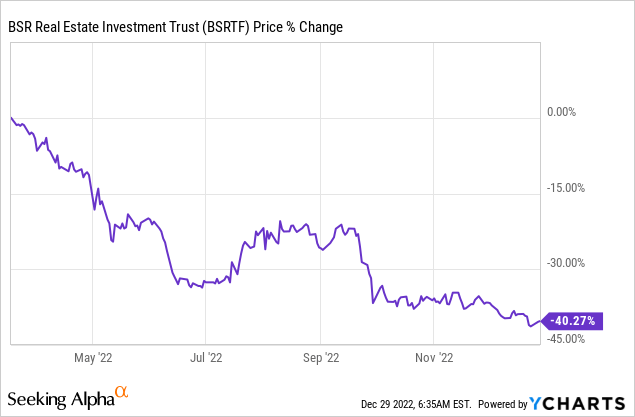

BSR REIT is the first one that comes to my mind, because I have accumulated a lot of it lately and it has become one of our largest holdings at High Yield Landlord.

We first bought it at around $11 in May of 2011 and saw it rise all the way to $22 within a year. It was one of our best performing investments of 2021.

But here we are today, and it is down 40% from its highs, and trades at just $13 per share.

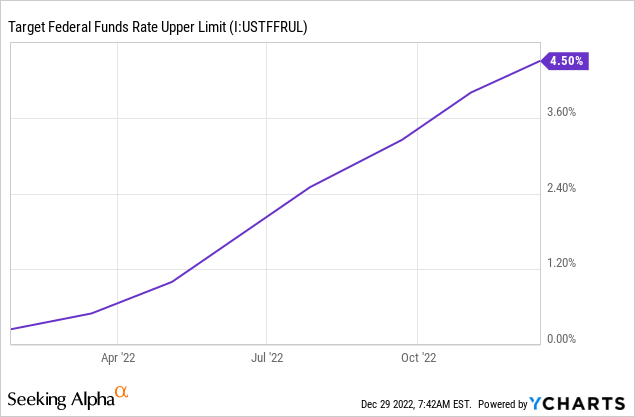

In hindsight, it is easy to look back and say that we should have sold above $20 when the Fed began to hike interest rates.

But we didn’t because it was still priced reasonably and its rents were growing rapidly. Its NAV per share was $22, so we weren’t paying a premium, and since most of its apartment communities are in rapidly growing Texan markets, its same property NOI was growing (and still is!) at around 10%.

BSR REIT

Moreover, we thought that any cap rate expansion would be more or less matched by rising NOI. Besides, we also thought that a major expansion in cap rates was unlikely given that there is a lot of demand for apartment communities, especially in sunbelt markets.

Blackstone (BX) and other private equity players have recently bought out entire apartment REITs, and the larger REITs like AvalonBay Communities (AVB) have not had difficulties selling assets at 3.5-4.5% cap rates. This in part is because there are lots of cash buyers who need long-dated, inflation-protected assets.

But regardless, BSR has dropped by 40%, and, in hindsight, we overlooked one thing: the impact of rising interest rates is materially higher on the market sentiment of REITs that own lower cap rate assets like Texan apartment communities.

This explains why BSR is down so much.

The lesson is to favor REITs that own higher cap rate properties in an environment of rising interest rates, especially if you expect significant rate hikes like today.

The flipside of this is that you should probably favor lower cap rate assets when interest rates begin to decline. This is why I have been accumulating a lot more shares of BSR at these prices. Just to get back to its NAV, it would need to rise by 70%+, and you earn a 4% dividend yield while you wait. The management is also buying back shares.

iStar Inc. (STAR)

STAR is a similar story as BSR.

STAR is the biggest shareholder and manager of Safehold Inc. (SAFE), which is a REIT that specializes in ground leases.

Ground leases are arguably the safest real estate investments that you can make in terms of cash flow resilience, but they are also some of the most sensitive to interest rates because the lease terms are very long, up to 99 years. In case you are not familiar with ground leases, you can watch the video below:

We first invested in the company at ~$8 per share in August of 2020. It then more than doubled in the following year, as it rose to $21. Just like BSR, it was one of our best performing investment in 2021.

But here was our mistake:

We gave too much credit to this surge in share price to the growing fundamental value of the company.

Yes, SAFE was growing rapidly and creating a lot of value for STAR, but the reality is that this exceptional surge was also largely the result of the historically low interest rates.

Perhaps, we should have realized that this wouldn’t last and that a surge in interest rates would pose a very significant thread to the valuation of the company. It is of course easy to say that today, but we couldn’t know back then that Russia was about invade Ukraine, which extended the period of high inflation, and forced the Fed to double-down on its efforts to fight inflation.

This caused STAR’s share price to collapse. It dropped all the way to ~$10, and it then also made a one-time special dividend distribution, which put its share price today at $7.50.

We sold half of our position at around $19 in November 2021. In hindsight, we probably should have sold it all given that ground leases are extremely sensitive to interest rates and rates were posed to return on the rise.

The lesson again here is to recognize that not all property sectors react the same way to rising interest rates.

Bottom Line

Even the best investors in the world have losers in their portfolio.

This is normal and even expected.

Every investment has risks, and sometimes these risk factors play out.

But you cannot put the blame only on these risk factors.

In the case of BSR and STAR, we failed to recognize or the very least underappreciated the fact that rising interest rates wouldn’t have the same impact on every property sector.

The REITs that focus on lower cap rate properties were the most heavily impacted by rising rates, and we probably could have seen this coming.

We live and we learn!

Now, let us know in the comment section below what were some of your worst performers in 2022.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.