Verizon Q4 Earnings: A Strategy To Lose Market Share (NYSE:VZ)

David Ramos

Thesis

Verizon (NYSE:VZ) has an older demographic of customers who are higher-income earners and laggards in technology innovation adoption. With this insight, management’s strategy makes sense; to prioritize existing margins rather than growth in user base volumes and to cut capex, favoring near-term shareholder yields as opposed to long term technology leadership. The problem is, I think this is precisely what is leading to a creep up in churn rates and a slow bleed in market share. Something has to change lest Verizon remains an underperformer.

My Read on Q4 FY22 earnings

Verizon reported its Q4 FY22 results last week. The key highlights for me were threefold:

1. Guidance cut

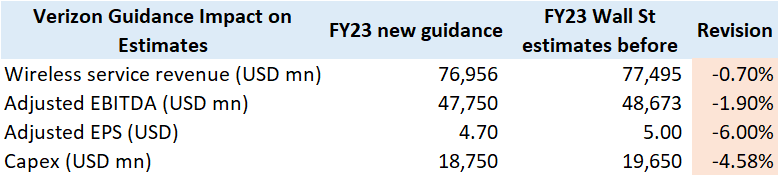

Verizon Guidance Cuts vs Consensus Estimates (Company Filings, Capital IQ, Author’s Analysis)

As the table above shows, Verizon disappointed Wall St on its revised FY23 guidance on key operating parameters of wireless service revenues (which makes up 78% of total company revenues), adjusted EBITDA and adjusted EPS.

Some investors and analysts may view the ~4.6% cut in FY23 capex as welcome news, as it would imply greater cash available for shareholder distributions. However, based on further analysis discussed in this article, I do not view this as a particularly positive sign.

2. Lack of growth aggression from commentary

You can expect Verizon to compete, but I want to underline again that we will not sacrifice financials for volumes. We continue to focus on improving our cost of acquisition and retention and believe current promotional incentives are not sustainable for the industry in the long run. Although we have participated, to some extent, in this dynamic, expect us to pursue more ways to move away from the aggressive handset subsidies.

– CEO Hans Vestberg in Q4 FY22 earnings call (bolded emphasis is mine)

This clearly indicated to me that Verizon is not going to prioritize growth. Further analysis below reveals likely reasons as to why I believe Verizon is not incentivized to grow.

3. Continued rise in churn rate

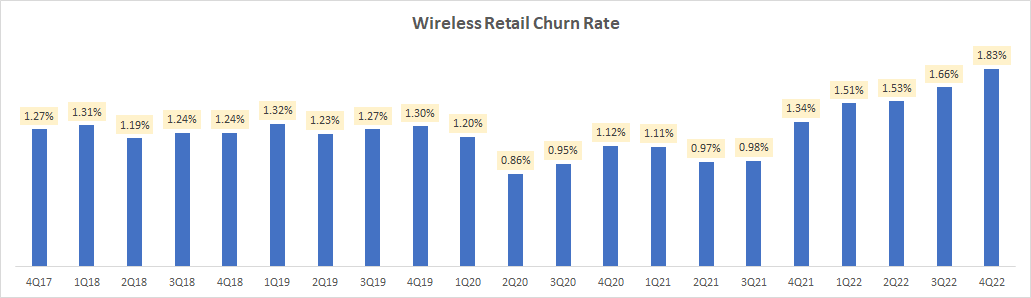

Wireless Retail Churn Rate (Company Filings, Author’s Analysis)

This is a key metric to track because consumer wireless retail makes up 34% of total company revenues. The breakup is as follows; consumer wireless service makes up 58% of total consumer revenue, which corresponds to 44% of total company revenue. About 79% of total consumer wireless is sold through the retail channel.

Verizon’s churn rate here continues to climb up for the 6th consecutive quarter in a row to 1.83%. This highlights potential market share loss.

Analysis of Verizon Customer Trends

My analysis of Verizon’s customer trends from a Statista Consumer Insights study reveals insightful color on Verizon’s competitive positioning and strategy. For context, 76% of Verizon’s total revenue and 86% of the total adjusted EBITDA comes from the consumer segment, making this analysis and the insights drawn from it very material to the future prospects of Verizon.

The surveys used in the analysis below include a wide sample size of 8,800 smartphone users in the United States.

Verizon Wireless is losing market share

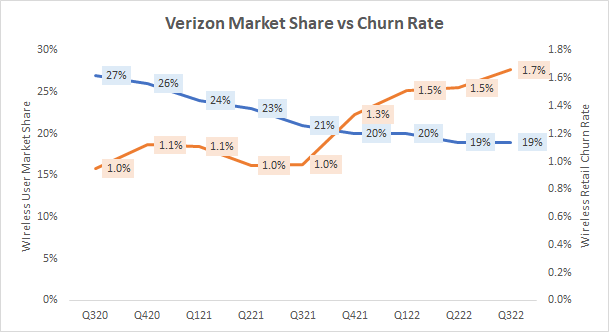

Verizon Market Share vs Churn Rate (Statista, Company Filings, Author’s Analysis)

As suspected, the higher churn rates do indeed coincide with a loss in wireless user market share.

Verizon’s users are older

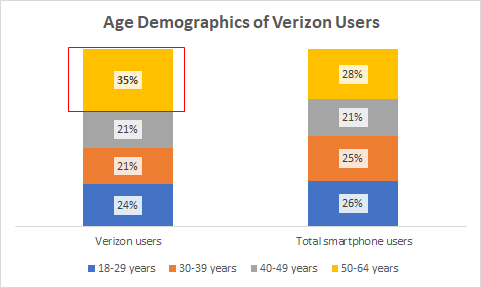

Age Demographics of Verizon Users (Statista, Author’s Analysis)

The chart above shows a much higher proportion of users in the 50-64 years age group compared to the total group of smartphone users. Assuming low telecom network provider switching effects, then I infer that Verizon is left with a customer mix with a relatively lower customer lifetime value (LTV).

Naturally, this would be mitigated if more consumers switch to Verizon. However, currently, the market share and churn rates are not in Verizon’s favor. But what about in the future? What does it take to switch a consumer to another telecom network provider? I believe the switching cost of a telecom provider is not high, but the switching impetus must be strong. People do not switch providers unless they get a better deal on prices, there is a lack of network coverage, disappointment in service quality or a motivation to migrate to a better technology.

Given the US’ mature telecom network, network coverage and service quality is unlikely to be a main issue. The key drivers causing users to switch providers then would be pricing and superior technology:

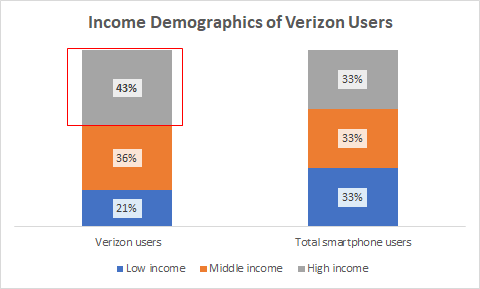

Pricing cuts are unlikely as Verizon’s main user base has higher incomes

Income Demographics of Verizon Users (Statista, Author’s Analysis)

Unsurprisingly, the higher proportion of higher older (by age) Verizon users coincides with a higher proportion of high income earners. I think the chances of Verizon willingly engaging in intense pricing competition to improve the age demographics of users and potentially LTV of its users is low, as that would mean leaving money on the table for its existing customers. This may be why Verizon’s management is not as hesitant to cut prices to the same extent as its competition.

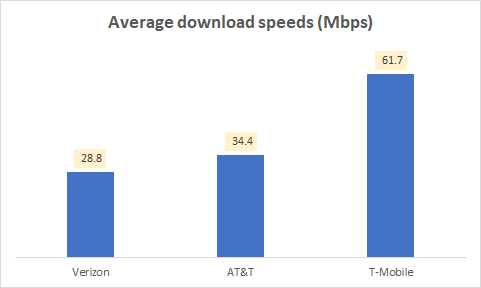

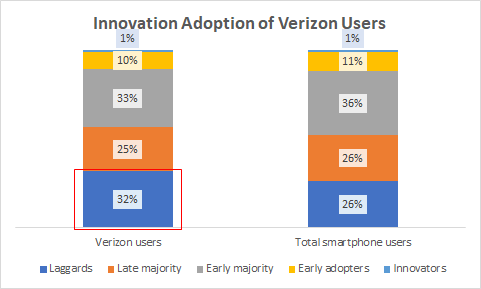

Verizon unlikely to prioritize technology leadership due to higher mix of laggard innovation adopters

Average download speeds (Open Signal, Author’s Analysis)

According to data from Open Signal, Verizon has 16% and 44% lower download speeds compared to its two main competitors – AT&T (T) and T-Mobile (TMUS). This is an indicator of Verizon’s laggard position in the technology curve. Note that under this lens, the capex cut mentioned earlier in the article is another indication of a strategic choice to not prioritize growth.

Innovation Adoption of Verizon Users (Statista, Author’s Analysis)

Moreover, with a higher proportion (32% vs group average of 26%) of users who are laggards in technology adoption, I contend that Verizon lacks the impetus to be a technology leader.

Valuation

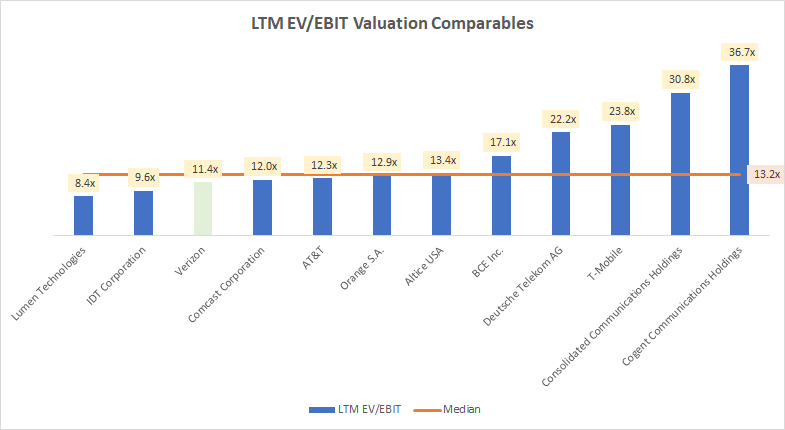

LTM EV/EBIT Comparables (Capital IQ, Author’s Analysis)

Peers set includes Verizon (VZ), Lumen Technologies (LUMN), IDT Corporation (IDT), Comcast Corporation (CMCSA), AT&T (T), Orange S.A. (ORAN) (OTCPK:FNCTF), Altice USA (ATUS), BCE Inc. (BCE) (BCE:CA), Deutsche Telekom AG (OTCQX:DTEGY), T-Mobile (TMUS), Consolidated Communications Holdings (CNSL) and Cogent Communications Holdings (CCOI)

At an 11.4x LTM EV/EBIT, Verizon trades at a discount of 13.3% to the peer-set median multiple of 13.2x. Given the company’s demographic positioning, continued signs of decline in market share and relatively lower incentives for pursuing growth leadership, I believe this discount is warranted.

Takeaway

I think Verizon’s existing customer mix and its characteristics is holding the company back from creating opportunities for market share gain and expansion of customer LTV. Ultimately, this results in a strategic path that does not prioritize growth. Instead, I anticipate a slow bleed in market leadership. With its current strategy, I think Verizon will underperform its peers.

I rate Verizon a ‘hold’, but if I were a shareholder, I would exit this stock in favor of something better, which I will share in another article soon.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.