UiPath: Stable Company With Long-Term Runway And Favorable Tailwinds (NYSE:PATH)

courtneyk

UiPath (NYSE:PATH) is one of the market leaders in Robotic Process Automation (RPA). The company began as a pure play on RPA, but has since evolved into a Business Automation Platform, a one-stop solution for businesses looking to operate at greater efficiency, speed, and responsiveness. While the company is currently experiencing slowing growth due to macroeconomic uncertainties, FX headwinds and conflicts in its key operating areas, its economic moat, strong leadership and sector tailwinds make UiPath a strong long-term pick from current prices.

UiPath Key Metrics

The company just reported its 4Q2023 results. Below are some of their key performance metrics.

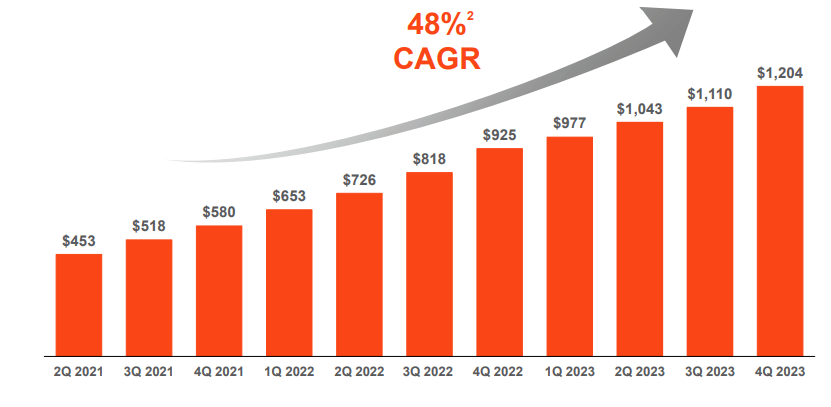

UiPath 4Q2023 Earnings Slides

The company reports ARR, short for Annualized Renewal Run-rate, which is defined as annualized invoiced amounts per solution, and is used as a forward-looking metric in the management of their business. Put simply, ARR is a predictor of UiPath’s recurring annual revenue as the company primarily sells licenses to use their software for a specific term.

ARR has been growing steadily, crossing the 1 billion mark for the first time in 2Q2023, and has since passed 1.2 billion in the latest 4Q reporting.

We also see another key metric, the Dollar-Based Net Retention Rate, which represents the rate of net expansion of UiPath’s ARR from existing customers over the preceding 12 months. Essentially, a number above 100%, means that existing customers are spending more money this year than last year. As it stands, the current rate is 123%.

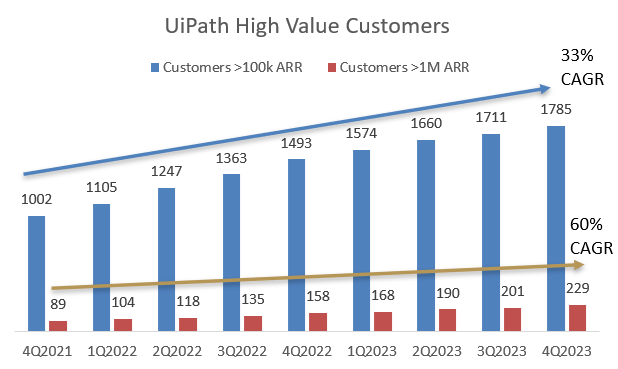

UiPath has also shown strong performance in the acquisition of high value customers, with customers contributing more than 100k and 1 million ARR showing steady increases over the last couple of years. Number of customers total more than 10,000, including members of the Fortune 10, the top Ten largest U.S. public and privately held companies published by Fortune magazine.

Author’s Own from UiPath Financials

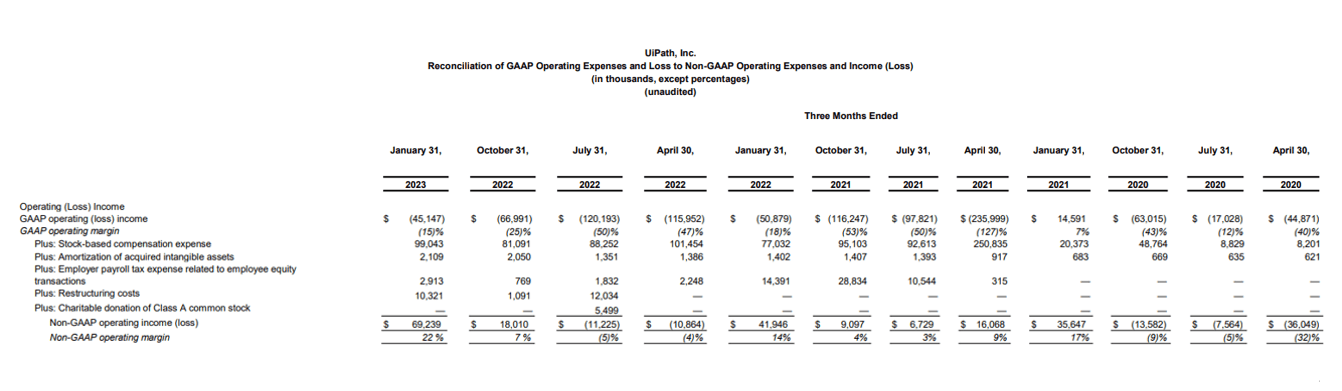

More significantly, the company has taken strides towards profitability with its lowest ever GAAP operating loss since its IPO in April 2021, at the same time achieving its highest ever non-GAAP Operating Margin of 22%. Moreover, guidance for FY2024 expects non-GAAP operating margins to rise further to almost 10%. All this brought cheer to the market as the shares rose after the earnings release.

UiPath FY2023 Supplemental

UiPath is certainly heading in the right direction financially. Qualitatively, these are the reasons why I invest in UiPath.

It has an economic moat

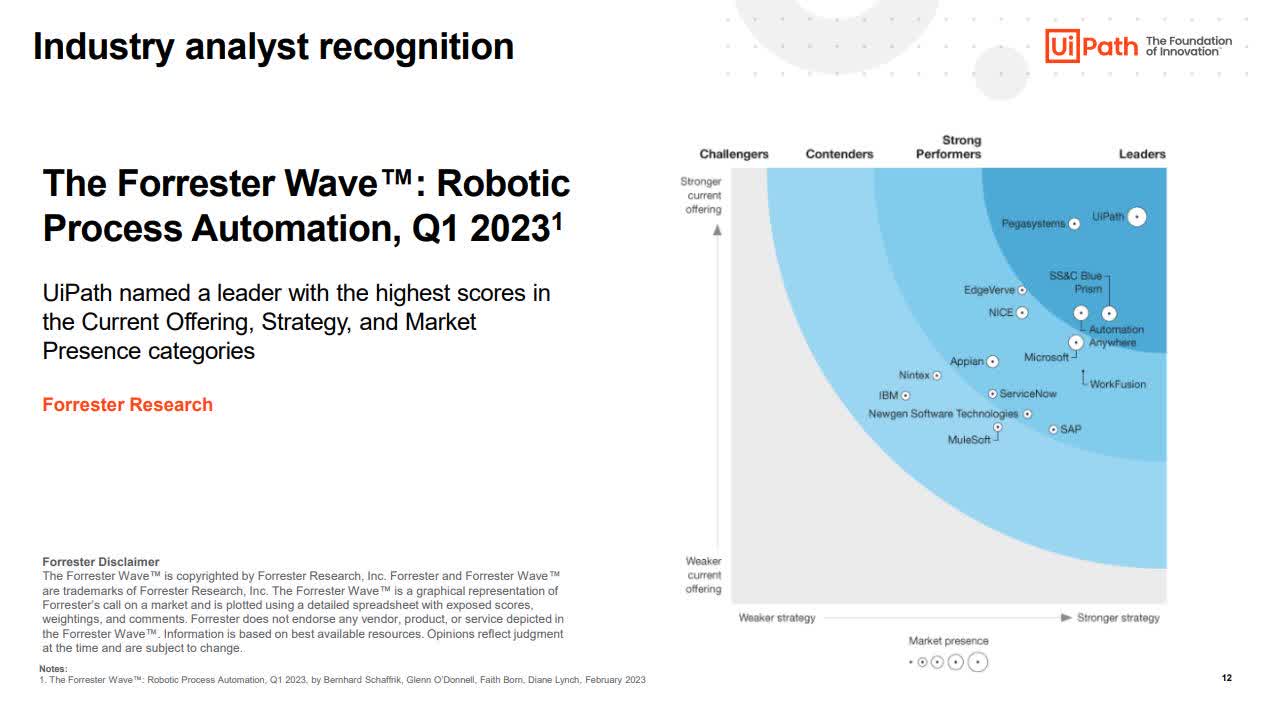

UiPath is a leader in its market and was recently named a leader in RPA by an independent research firm in The Forrester Wave™: Robotic Process Automation, Q1 2023.

UiPath 4Q2023 Earnings Slides

But UiPath wasn’t named as just any leader. Notably, it ranked highest of all 15 firms in each of the three categories assessed: Current Offering, Strategy, and Market Presence.

Additionally, according to the report, UiPath received the highest possible scores in 19 criteria including Vision, Innovation, Governance, Design Environment, Discovery, Intelligent Document Processing (IDP), Content Analytics and Processing, and SaaS and Platform Support.

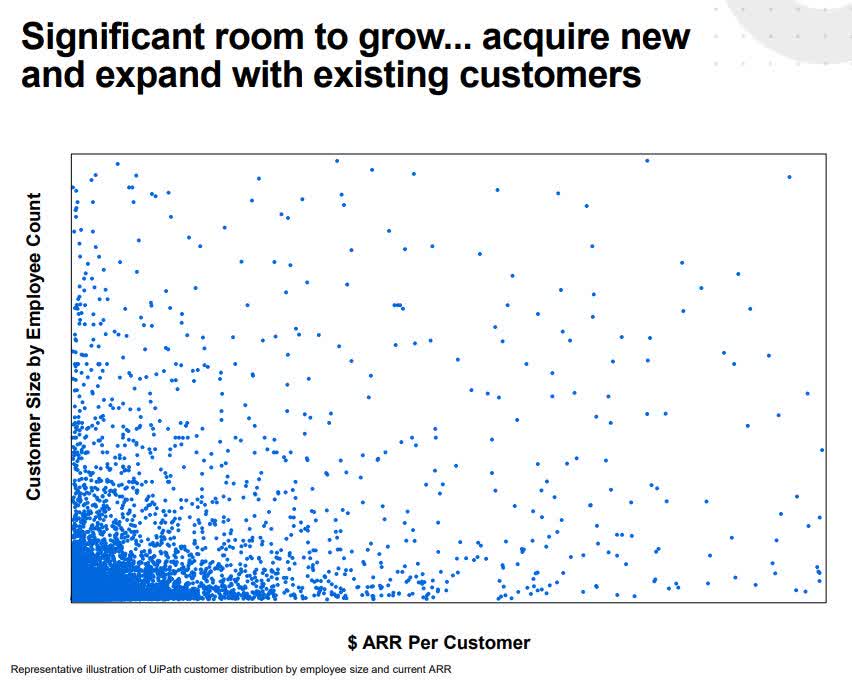

UiPath’s software may take some time to get set up and become accustomed too, but once clients realize its effectiveness, they tend to spend more.

In fact, this was highlighted in UiPath’s listing prospectus which states – “historically, once our platform is deployed our customers have significantly expanded their use of our platform by engaging with our customer success team as well as increasing use and spend across our product categories and pivoting into enterprise agreements for the entire platform.”

UiPath 424B4 Prospectus

This chart illustrates this clearly, with the height of the triangle increasing from left to right.

In the latest SEC filing (10-K FY2023), it also adds that ARR grew to $1,203.8 million from $925.3 million the prior year, with approximately 25% of this growth rate due to new customers and 75% due to existing customers. Along with a high dollar based net retention rate of over 100%, it is evident that UiPath has a sticky service.

In any sector, I only want to invest in the market leader, and it speaks volumes that according to a market share analysis report released in late July 2022 by Gartner, UiPath was the only vendor to grow its market share in 2021, from 28.5% in 2020 to 34.1%. And now, also receiving the highest points for market presence in Forrester’s 1Q2023 report. With large competitors like Salesforce, Microsoft and IBM in the mix, such statistics are very impressive indeed.

High Switching Costs is UiPath’s economic moat. Once a customer gets on board, they’re stuck, and will continue to spend more as they realize the benefits they can gain. It certainly helps that many of these customers are the largest companies in the world, with much more room to increase spending on UiPath’s services.

UiPath Analyst Day Presentation

UiPath is operating in a secular growth industry

Mentioned in the UiPath Investor Day 2022 presentation, tailwinds in the automation market include – customer and partner expectations, massive proliferation of software, tightening regulatory environment, fragmented technology landscape, business optimization, transformation of labor market, macroeconomic headwinds, the need to move faster, and supply chain disruptions.

UiPath Analyst Day Presentation

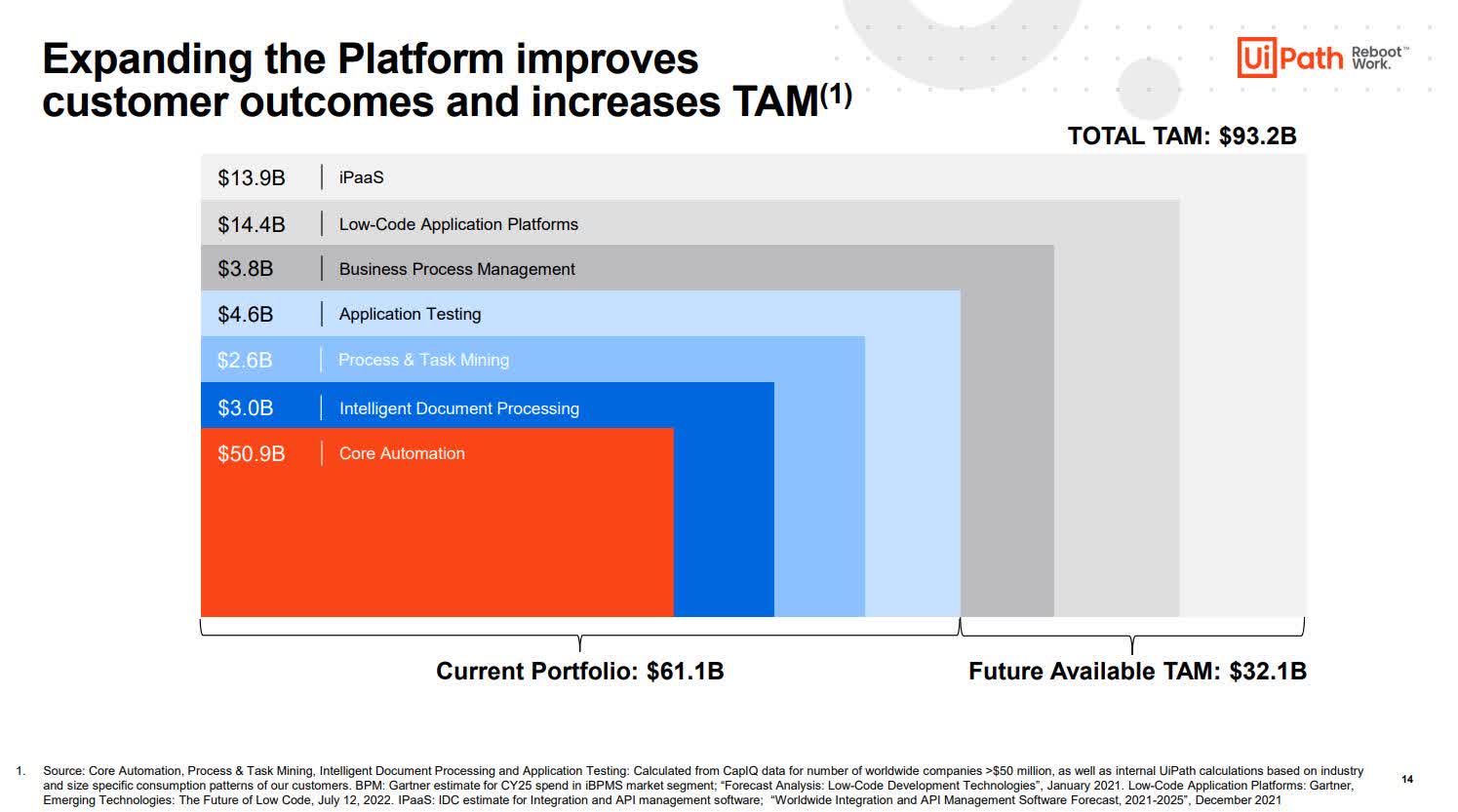

They estimate the potential total addressable market to be 93.2billion. For some context, the current market size of Customer Relationship Management or CRM software, is 63.91 billion in 2022.

While I am not entirely sure how accurate UiPath’s estimates of its Total Addressable Market is, I do agree with the tailwinds they have pointed out for the sector, and beyond that, demographic trends point towards a rapidly ageing world.

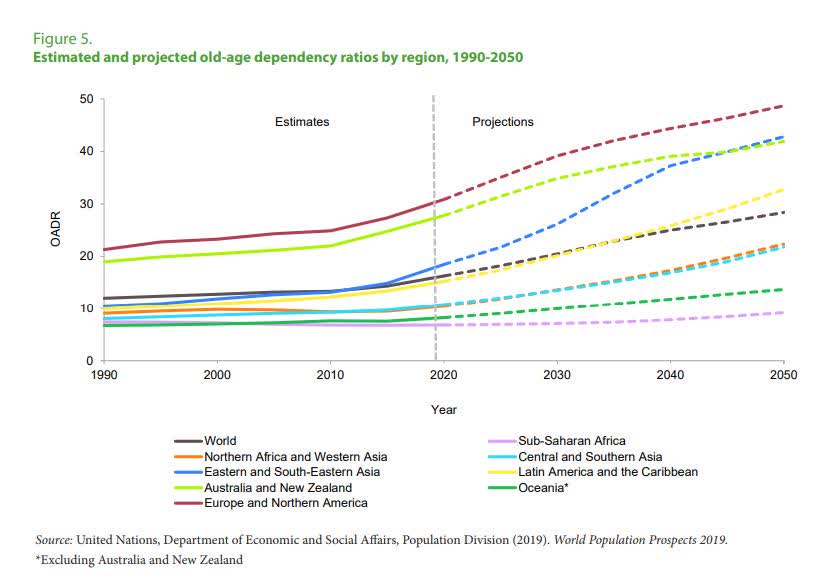

A recent report published by the United Nations in 2022 projects the share of the global population aged 65 years or above to rise from 10 per cent in 2022 to 16 per cent in 2050.

Another chart, also published by the United Nations in a report focused on World Population Ageing, shows this clear trend with a metric OADR, old-age dependency ratio, which is defined as the number of old-age dependents per 100 persons of working age. Globally, this is projected to increase from 16 old aged per 100 working adults, to 28 older persons for every 100 working age persons in 2050. The worst ratios are found in developed nations across Europe, North America, and Asia Pacific.

United Nations, World Population Prospects 2019

With less working adults to support a larger percentage of the population, it’s likely that workload per pax will increase and work will need to be more efficient in order to maintain similar output levels. This is where I foresee automation to play an increasing bigger role to enhance efficiency cover gaps in the workforce in future.

And definitely, UiPath is well positioned to take advantage.

Leadership

UiPath Blog: Daniel Dines

More specifically, UiPath is founder led. CEO Daniel Dines had humble beginnings from Bucharest, Romania. He then had a 5 year stint in Microsoft in the early 2000s before heading back to Romania to start UiPath with just 10 people.

I generally would prefer to invest in founder led companies as they typically worked very hard to build up their companies, are passionate in their work, and have long term visions for their firm. Often with large stakes in their own business, they tend be more careful with operations and treat everything like their own money.

A founder is more likely to take short term pains for the longer term good. That’s unlike a hired CEO whose incentives may lie more in making the business ‘look good’ so he can potentially get a higher bonus at the end of the year.

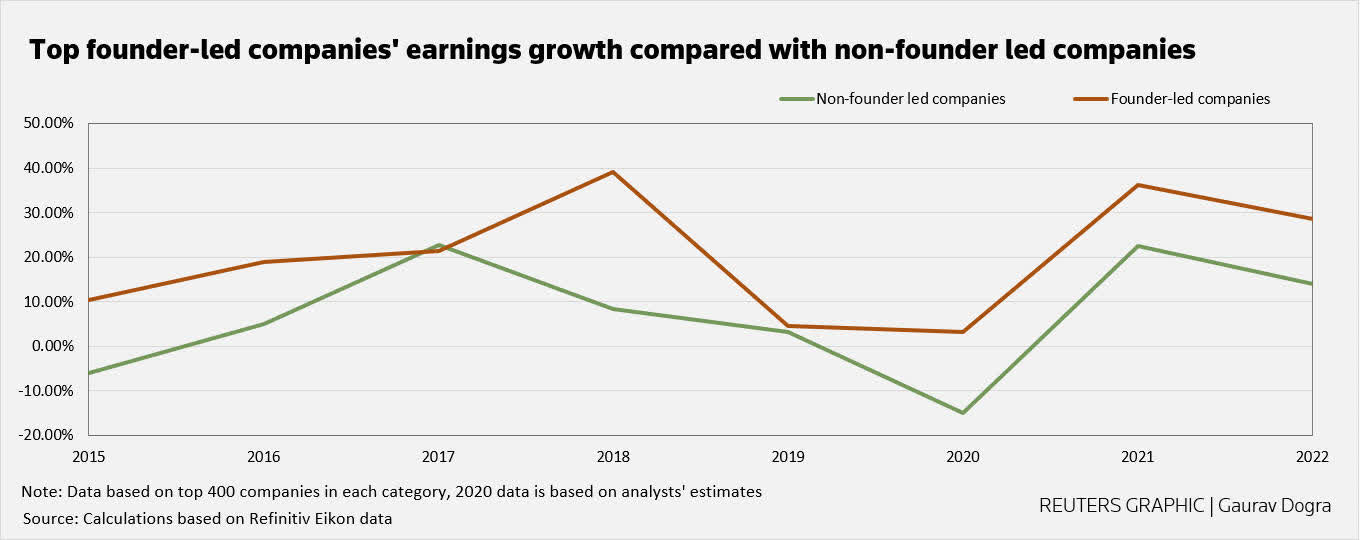

This success is also backed by data, where we see Top founder-led companies’ earnings growth consistently outperforming that of their non-founder led peers.

Refinitiv Eikon Data

At UiPath, Daniel Dines, has almost 20% ownership of the company, and more than 80% of the voting power. This truly is his company, and he has skin in the game.

Additional, co-CEO Rob Enslin has proven to be an astute addition to the team thus far, tapping on his valuable decades of expertise in enterprise software with Google Cloud and SAP. He almost certainly had a big part to play in UiPath’s go-to-market enhancements to focus more on the C-suite, larger customers, to increase deal size over time, while having a strong partner ecosystem for mid to lower segments of the market. The recent departure of Chief Business Officer Chris Weber, after only a year, will further streamline operations, with Rob Enslin assuming leadership of UiPath’s go-to-market function.

UiPath 4Q2023 Earnings Slides

So far, this partnership between the tech focused founder (Daniel Dines), and the business minded co-CEO (Rob Enslin) is bearing fruit. Do also watch some of the videos of them speaking on YouTube. Daniel Dines especially comes across as very sincere, and it’s hard to imagine him as a crook.

Concerns

While the long term thesis of UiPath is strong, there are some concerns which can potentially change my view on the stock.

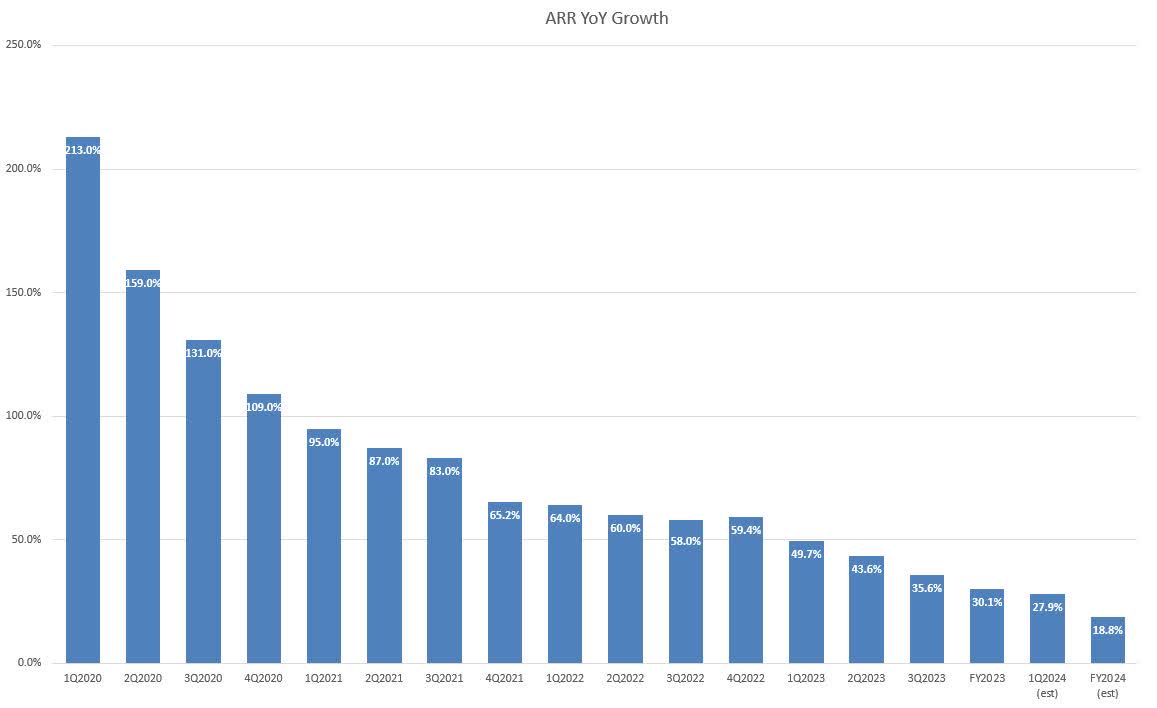

- Growth is slowing

Including FY2024 estimates, the YOY increase in ARR slows to 18.8%. For a supposedly fast growth company, this is a concerning trend. I would hope to see this figure increase, or at least stabilise around 20% yoy over the longer term.

Author’s Own from UiPath Financials

2. Dollar based net retention rate dropping

Another key metric, the Dollar based net retention rate is also dropping. This means existing customers aren’t increasing their spend on UiPath’s services as much in recent years as compared to prior periods.

Some slowdown in spending could be due to the uncertain macroeconomic environment, as well as impact from FX and Russian sanctions, where otherwise, reported figure for the current quarter would be ~129%. Nevertheless, a dollar based net retention rate of above 120%+ is still very good, and I would want to see it ideally being maintained around 120%+.

Author’s Own from UiPath Financials

3. High Stock Based Compensation

This is a topic that has been discussed multiple times, as UiPath’s stock based compensation is more than 30% of its Sales. It merits much discussion, but a recent other article I read on Seeking Alpha analyses it well. In a nutshell, UiPath’s dilution potential from SBC may not be that bad.

Valuation

Seeking Alpha

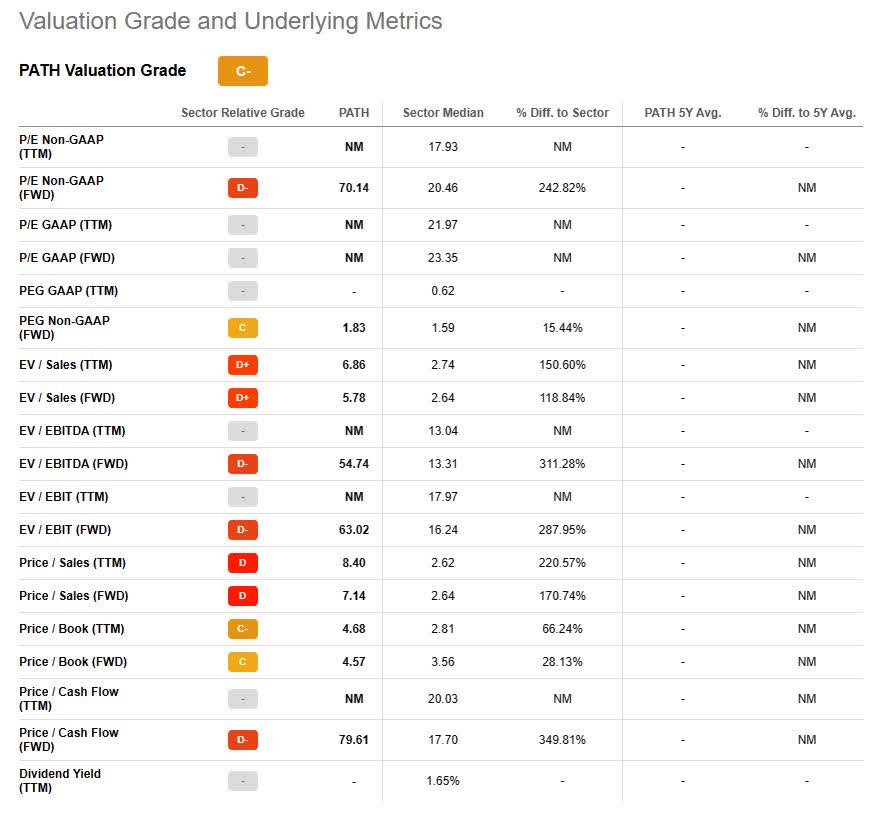

With a Price/Sales (FWD) of 7.14 and a Price/Cash Flow ratio of 79.61, UiPath is most certainly overvalued at the moment, even more so when you take into account the slowing growth rates.

Alternatively, I looked at the scenario should UiPath cut their Sales and Marketing spend. As the company’s software is very strong, with a high dollar based net retention rate, I hypothesized the event that UiPath does not spend on sales and marketing, and instead focuses solely on improving their product and retaining customers simply from being too useful to their clients.

|

FY2023 |

FY2023 (without sales and marketing) |

|

|

Gross Profit |

$ 878,530 |

$ 878,530 |

|

Operating Expenses |

||

|

Sales and Marketing |

$ 701,558 |

$ – |

|

Research & Development |

$ 285,750 |

$ 285,750 |

|

General and Administrative |

$ 239,505 |

$ 239,505 |

|

Total Operating Expenses |

$ 1,226,813 |

$ 525,255 |

|

Operating Loss |

$ -348,283 |

$ 353,275 |

|

Net Loss (Profit) |

$ -328,352 |

$ 373,206 |

|

P/E Ratio at current 9.14b market cap |

24 |

|

|

P/E Ratio at 7b market cap |

19 |

As shown in the table above, based on Fy2023 results and the current market cap of UiPath, the PE ratio is 24. More reasonably, at a trading price of about $12 per share, when UiPath’s valuation was about 7 billion, the P/E multiple would have been 19. The company’s shares traded around that range for long periods of time over the last 6 months and based on my analysis, 19 is a fair long-term P/E ratio and I accumulated my positions in the stock around that range.

Final Words

The environment will continue to remain choppy over the short run for a discretionary service like UiPath. But given the long term trends present, I do envision that automation software will become an essential need for all businesses. And when that time comes, UiPath will potentially become mainstream, and its growth will skyrocket.

In the meantime, the business is stable, with increasing profitability and no debt. I will therefore continue to slowly accumulate my positions in the company.