Time To Increase The Fed’s 2% Inflation Target

Douglas Rissing/iStock via Getty Images

I have written 3 articles since September 2021 explaining how higher U.S. wage inflation is likely to be permanent for the foreseeable future except in times of economic weakness. The links to them are below.

Get Ready For Sustained Wage Inflation (September 2021)

Higher Wage Inflation Is The New Normal (August 2022)

Jay Powell: It’s All About Wage Inflation Now (December 2022)

Demographics and Secular Trends

The reason for higher wage inflation going forward is a number of demographic and secular trends have emerged at the same time leading to a tight labor market for the foreseeable future. These trends are listed below. For much more detail on each please see the second article I linked to above.

1. Slowing population growth

2. Increased early retirements

3. Reduced immigration

4. Lower workforce participation

5. A trend toward onshoring

6. Lower end jobs having higher vacancies

7. Corporate job growth fueled by innovation

8. Higher education levels

Of the 8, the most important is actually number 7. This one has been around a long time in the U.S. but in the past was offset by offshoring, immigration, net births and increased workforce participation. Despite having 4.5% of the world’s population, U.S. corporations have about 50% of the market value of all publicly traded corporations worldwide. They are also involved in well over 50% on the innovations and inventions. Innovations are only increasing. That means more and more demand for labor. But with less offshoring, immigration, workforce participation and more retirements, where will the workers come from to absorb the corporate job growth? AI and robotics are a partial solution, but that is still quite a ways away from meaningful numbers.

The Fed’s Stance

The Fed itself has completely changed its tune on inflation twice in the last 18 months. At first, they said inflation was transitory. Then they said it was out of control and needed rapid rate hikes to contain. Just in the past few months they have changed again. Their concern now is now mostly wage inflation. Chairman Powell’s most recent speech on the economy on November 30, 2022, was almost entirely about why wage inflation is what the Fed is now fighting. In the speech he specifically mentioned 4 of the factors I listed above.

Wage Inflation

There has been an increasing chorus of people saying it’s time for the Fed to stop raising interest rates because overall inflation is declining rapidly. While that is technically correct, what they are missing is wage inflation and services inflation (which is heavily impacted by wage inflation) is very sticky. That means it’s hard to stop once started. If not stopped it can spiral even higher.

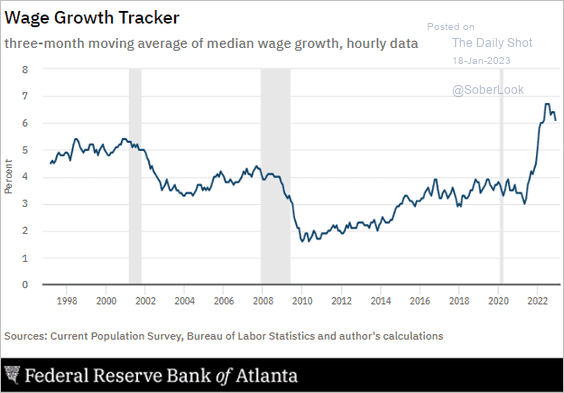

We are nowhere near getting wage inflation back to the 2% inflation target. The Fed’s own chart shown below shows it is only starting to decline. It also shows wage inflation has been tracking up since 2015. That shows what we are faced with now has been building up for at least 7 years.

Federal Reserve of Atlanta

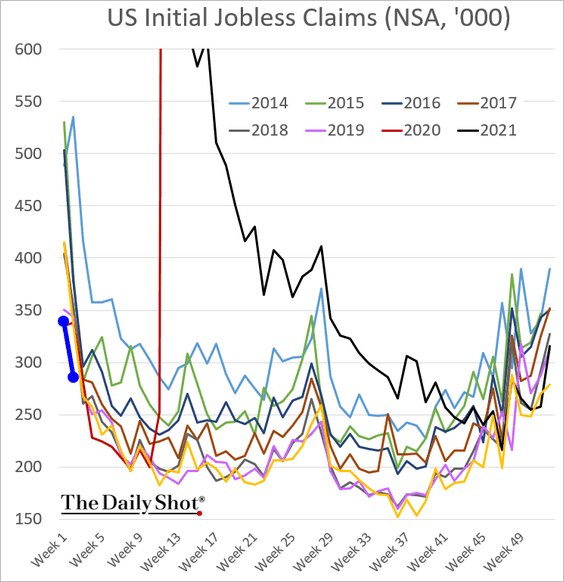

The chart below shows new jobless claims are actually declining right now. That is the wrong direction for the Fed.

The Daily Shot

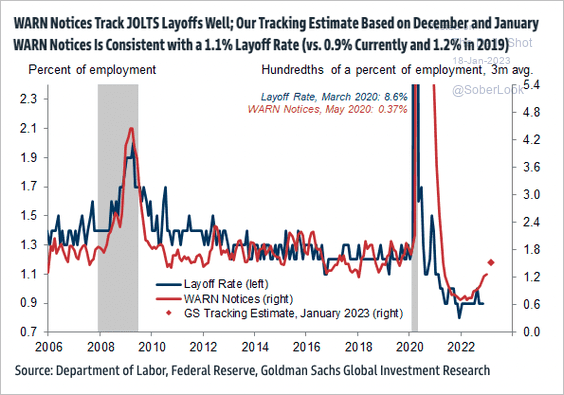

Layoffs are still well below historical norms.

Department of Labor, Federal Reserve, Goldman Sachs

Meanwhile, job openings remain at about 1.7 for every unemployed and available worker. That is still near historically high levels.

Why Increase the Inflation Target?

The Fed is now highly focused on reducing wage inflation. But what if they are fighting the wrong battle? I agree wage inflation does need to come down. But the 2% overall inflation target now appears antiquated for the following reasons.

1. Wage inflation is likely to be higher for the foreseeable future

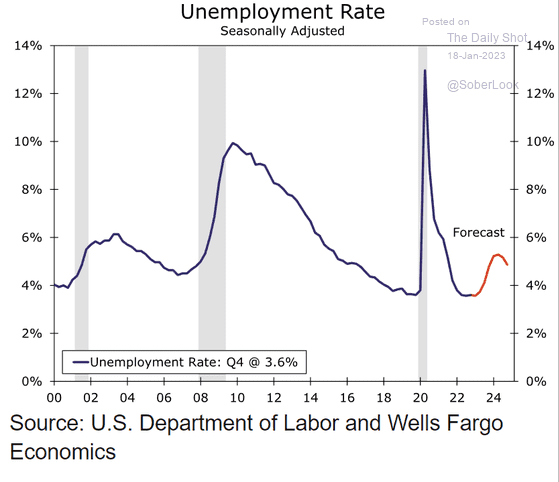

Wage inflation is no longer a short-term problem. It is structural and likely to persist based on the 8 demographic and secular trends listed earlier in this article. You may recall, the unemployment rate was at a historic low of 3.5% just before the pandemic The pandemic hit and it spiked up. But within 2 years went right back to the historically low 3.5% rate as shown in the chart below. That’s an indication of the permanence of our tight jobs market.

U.S. Department of Labor and Wells Fargo

Why would we think, with all the demographic and secular factors out there, that anything different is likely to happen this time? In fact, most forecasts are for the unemployment rate to fall back to a low level relatively quickly once the likely recession we are now facing ends. The chart above is a forecast by Wells Fargo, but others are similar.

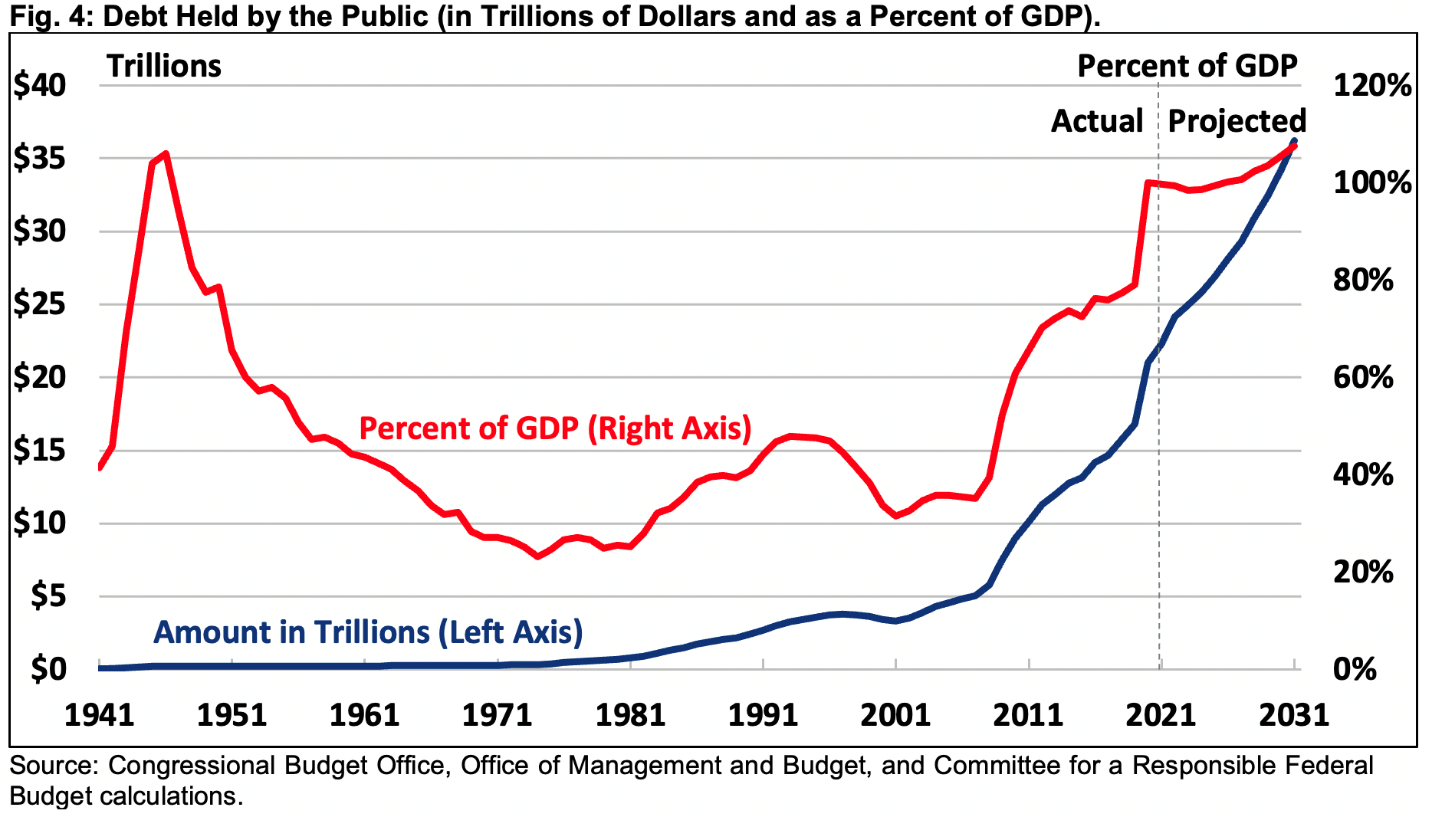

2. We also have a huge government debt problem

Our federal government debt has skyrocketed to levels not seen since World War II as shown below.

Congressional Budget Office, Office of Management and Budget, and Committee for a Responsible Federal Budget

In recent years this surge in debt has been ignored because interest rates and inflation were low. It wasn’t causing any problems. But higher debt is inflationary and higher interest rates are needed to fight inflation. Higher interest rates create an even larger budget deficit which cycles into even higher debt.

Look carefully at the chart above. Notice how the amount of debt has caught up to the ratio of debt to GDP. That was caused by inflation. Back in the late 1970s, when inflation was soaring even higher than now, I recall a Saturday Night Live skit about it. Dan Akroyd played President Carter and his punchline was “inflation is our friend”. It drew a big laugh. While I wouldn’t call Inflation a friend, it actually helps reduce our debt to GDP ratio. It’s not the amount of debt that’s the problem, because it’s all relative. It’s the amount of debt to the GDP which is the cash flow available to service that debt.

3. Higher wage inflation than general inflation helps consumers’ standard of living

There are really two types of inflation, commodities and services. Commodities are things like energy, fuel, food, vehicles, houses, furnishings and clothing. Commodity inflation tends to solve itself through a reversion to the mean. If a commodity gets expensive, more of it gets produced and the increased supply drives down prices. If that doesn’t work, buyers look to cheaper substitutes. Services inflation are different as it is much more impacted by wage inflation. Wages are a much larger component of services costs than for retail, manufacturing, and other portions of the economy. We don’t have the ability to increase our workforce much at all. Substitutes such as AI and robotics are nowhere near able to fill the gap yet.

The point I am getting to is if we allow inflation to be a little higher, wages will benefit more than commodity prices. That helps our work force. What helps our workers helps our economy.

The solution

The Fed has the ability to take inflation down to 2%. But for how long? Demographic and secular trends will likely result in another tight labor market before too long.

Allowing higher wage inflation helps with our public debt levels and reflects the reality of our labor market. That will probably mean higher overall inflation because wages are a part of most other aspects of inflation. My recommendation is wage inflation be allowed to stay in the 3-4% range with overall inflation at 2.5 to 3.0%. This will reduce the growth of debt to GDP ratio over time.

A higher inflation target does not solve the tight labor market problem, it just reflects the reality. To solve it, we will need a combination of more offshoring, immigration, AI and robotics.

The Fed has a history of being reactive, not proactive. To be fair so does all government. This is a chance to be proactive and adjust to a new reality in our labor market and government debt.