Northrim BanCorp Stock: Between Glaciers And Recession (NRIM)

zorazhuang/E+ via Getty Images

Northrim BanCorp (NASDAQ:NRIM) was founded in 1990 and is headquartered in Anchorage, Alaska. This bank has a very small market capitalization, only $219 million, and total assets amount to $2.58 billion.

Northrim BanCorp Q1 2023

In any case, we should not underestimate the importance of this bank, as it is quite renowned in the geographic region in which it operates. In Alaska, Northrim BanCorp is among the top 4 banks with 90% of the deposit market share, so this high concentration allows these banks to have good bargaining power. There is little competition, and the last bank to enter this market was Wells Fargo in 2000 when it purchased National Bank of Alaska.

This atypical situation has both disadvantages and advantages as I will show you in this article.

1st advantage: little competition, higher yields on loans.

The first advantage definitely relates to the little competition that resides within the banking market in Alaska. Not everyone wants to operate in this geographic segment because, as we will see later, there are some disadvantages that act as barriers to entry. So, it is for this reason that to date the top 4 banks, including Northrim BanCorp, exhibit such dominance in this territory.

Consequently, since there is limited choice for customers, Northrim BanCorp’s bargaining power can generate a good yield on loans.

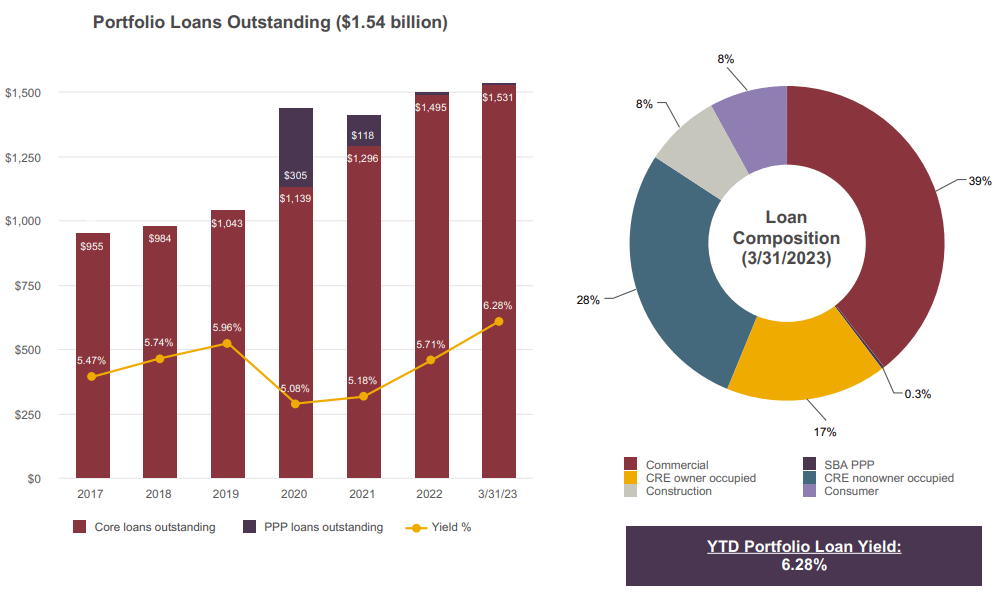

Northrim BanCorp Q1 2023

In 2019 the loan portfolio was $1.04 billion, while today it is $1.53 billion: basically a 50% increase in about 4 years. By the way, for the time being, the growth trend has not yet stopped despite the fact that interest rates have significantly increased since last year. Also, in this picture we can see that the loan yields of this bank have always tended to be quite high. In 2020 and 2021, interest rates were close to 0% but the loan yield was still above 5%.

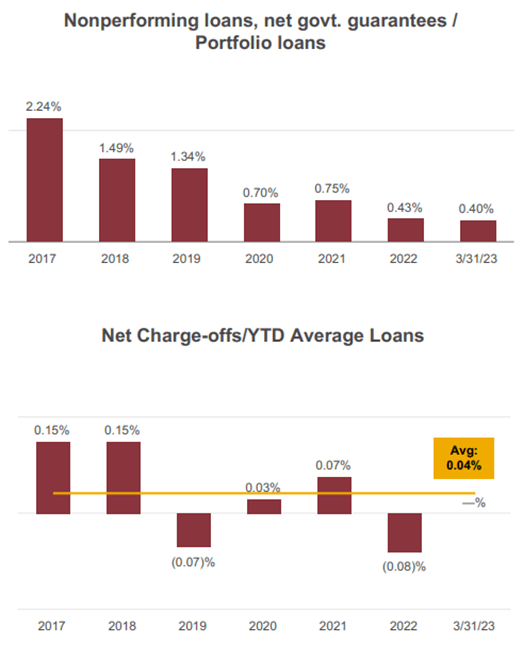

Finally, the credit quality is increasing as shown by the decreasing nonperforming loans.

Northrim BanCorp Q1 2023

The only flaw in my opinion is a low loan beta: compared to 2020, the Fed Funds Rate has increased by 500 basis points, but the current loan yield is only 120 basis points higher than in 2020.

Northrim BanCorp Q1 2023

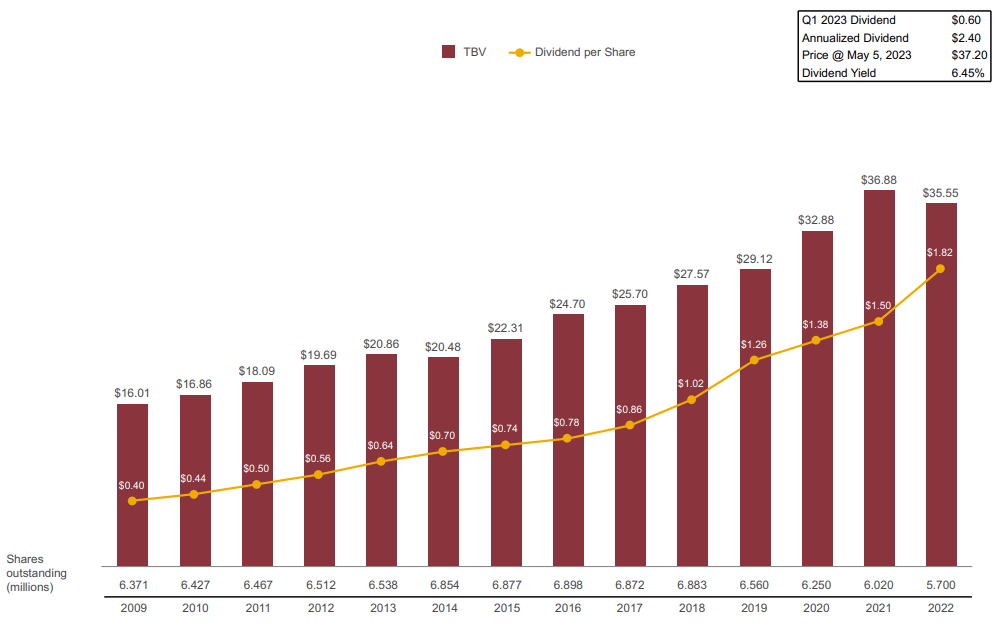

In any case, loan yields have made it possible for the dividend per share to rise steadily, not only because of an increase in the dividend issued, but also because of a strong buyback that began in 2018.

2nd advantage: little competition, deposits remain solid.

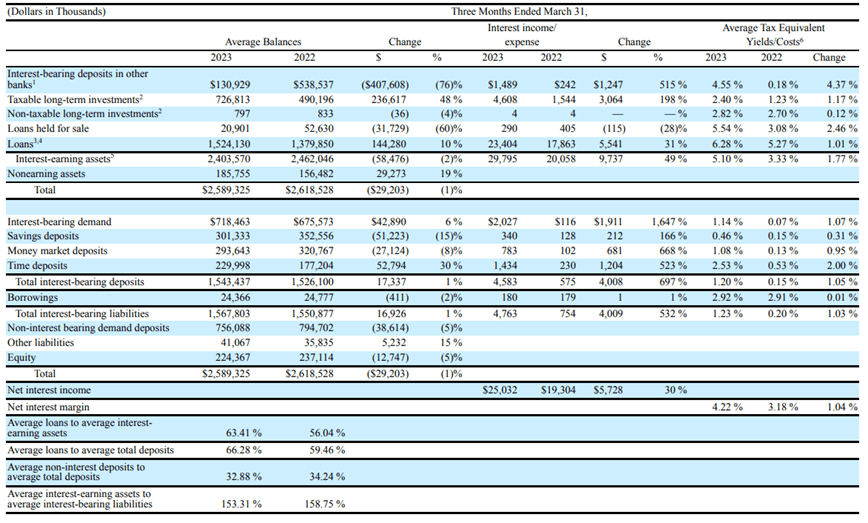

The LDR is 66%, so the bank definitely has more deposits than money lent, so there is no shortage of liquidity to invest. The average balance of total interest-bearing deposits reached $1.54 billion, about 1% more than in 2022. So despite the banking crisis, there is no shortage of deposits. Non-interest-bearing deposits amounted to $756 million on average, down 5% but still accounting for an important share of total deposits: about 33%.

Northrim BanCorp Q1 2023

Considering that we are talking about a miniscule bank with 43% of deposits that are uninsured, I would have expected much worse results after all the problems in the banking sector that arose in Q1.

Northrim BanCorp Q1 2023

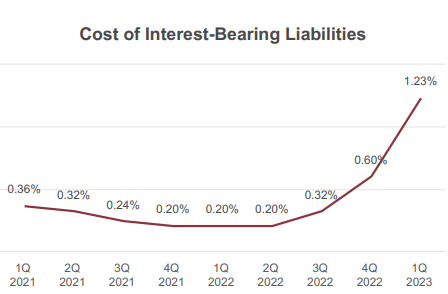

Regarding the cost of interest-bearing liabilities, it is clear that the trend is strongly bullish. Compared to last year, there has been an increase of 103 basis points, but overall I do not consider it such a disastrous result. One has to consider that Northrim BanCorp can also rely on a significant amount of non-interest bearing deposits. The problem is that we do not know how far the cost of interest-bearing liabilities will go. In 3 months there has been an increase of 63 basis points and I have concerns that this trend may continue.

Under current conditions I view this bank’s deposits positively, as the total amount has not been affected too much by the banking crisis and the cost is not excessively high. However, continuing at this rate, deposits may become too expensive and my opinion may change.

1st disadvantage: loan portfolio composition

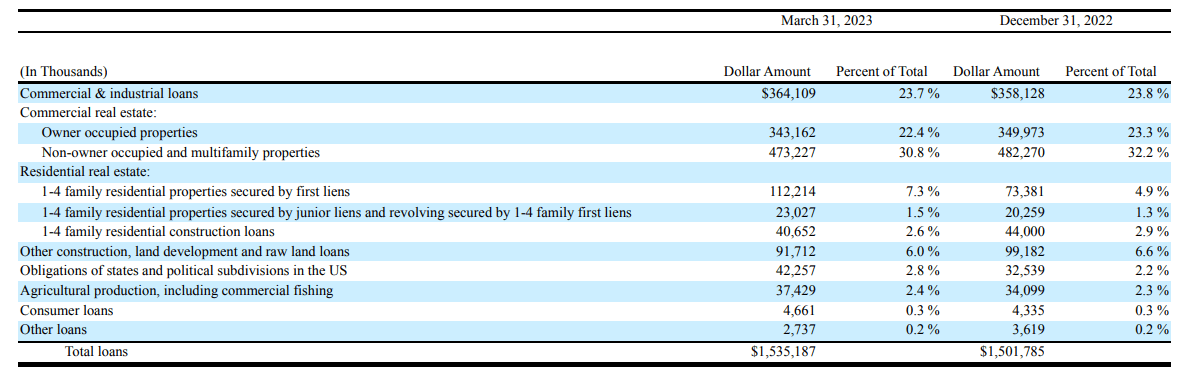

Probably the biggest disadvantage is that Northrim BanCorp, operating only in Alaska, is 100% exposed to local market trends. What is more, a predominant exposure is evident for the commercial real estate segment rather than residential real estate. This may also become an advantage should the local market be expanding, but overall it represents a rather high risk to not have a diversified portfolio.

Northrim BanCorp Q1 2023

The Commercial & Industrial loans and Commercial Real Estate segment have a weight of 78.90% of the entire loan portfolio. In comparison, the Residential Real Estate segment accounts for only 11.40% of the entire portfolio.

So, this bank is not only totally dependent on the local market, and this can become a major problem in the event of a recession, but also has risky exposure. Typically, the residential real estate segment is more resilient in a crisis, yet the bank has minimal exposure. In any case, I do not blame the bank: if local citizens do not apply for a mortgage on their first home there is little they can do.

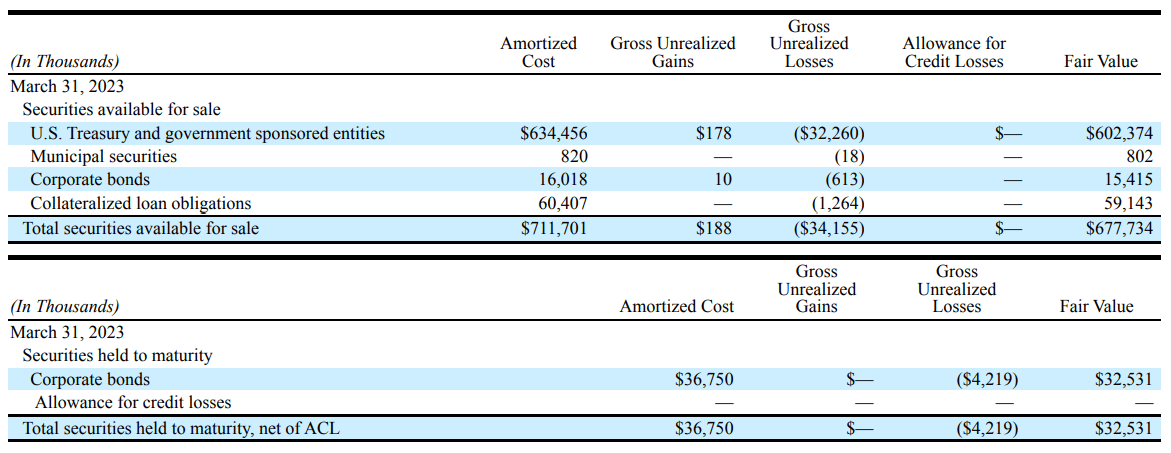

It is probably also for this reason that Northrim BanCorp has a rather high exposure in U.S. Treasuries, which are considered as a kind of complementary investment to the mortgage.

Northrim BanCorp Q1 2023

The fair value of this position is $602.37 million, about 23% of total assets, and will mature within 5 years. So we are not talking about securities with high duration and which can cause significant unrealized losses.

Overall, I agree with the strategy of using U.S. Treasuries as a complementary financial instrument to the loan portfolio, especially to try to reduce the overall risk of the assets. In any case, concerns remain about exposure to the CRE segment, especially in this historical period where everyone expects a recession. The bank’s exposure to such a narrow market does not allow it to diversify enough.

2nd disadvantage: higher operating costs

Operating expenses in Alaska are higher than those of mainland banks, and this is an objective fact. The size of the territory, its morphology, and climatic conditions weigh heavily on operating costs. Fortunately, high yields on loans and cheap deposits manage to mitigate this problem, but it should not be overlooked. I attach 2 concrete examples released by Northrim BanCorp:

- 1,300 miles from Nome to Ketchikan (1,400 miles from New York to Dallas)

- 6 branches and LPOs only accessible by boat or plane

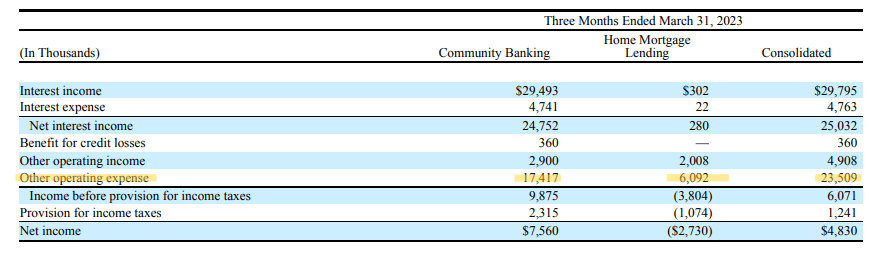

Northrim BanCorp Q1 2023

As can be seen, operating costs are definitely high, and they are not always covered by net interest income. In the case of the Home Mortgage Lending segment, the $280,000 in net interest income is significantly less than the $6.09 million in operating expenses. All this is obviously reflected in EPS as well.

Northrim BanCorp Q1 2023

Conclusion

Northrim BanCorp is an attractive bank because it operates in a market with little competition, but as we have seen this also has disadvantages. Little diversification of the loan portfolio, few mortgage applications, and extraordinary operating costs related to the tortuosity of the area.

Despite this, the bank has been issuing an increasing dividend per share since 2009, and the current dividend yield of 5.20 % could be an opportunity to have a stock in the portfolio that can generate steady and increasing cash flows.

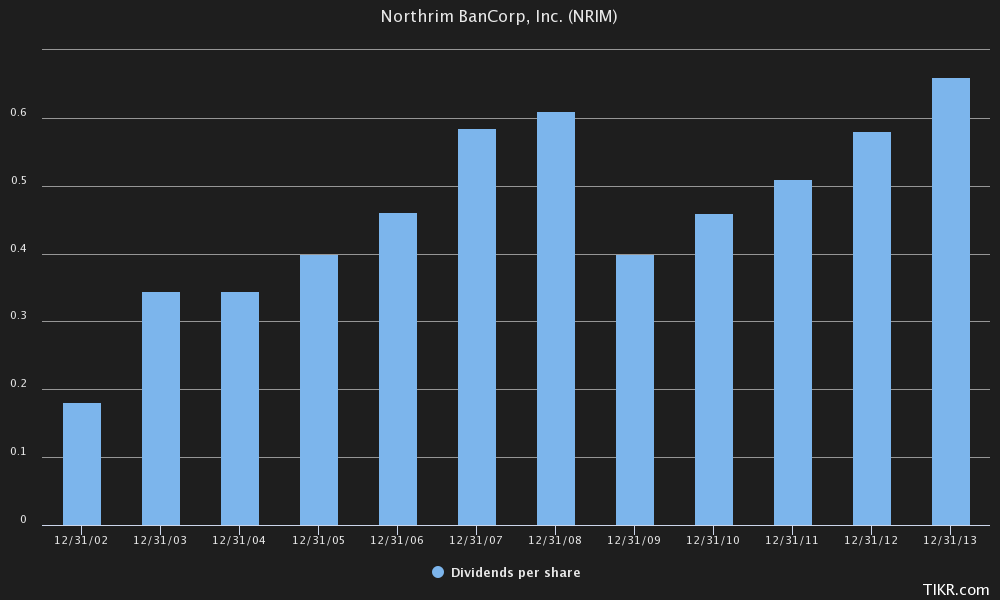

However, not all gold glitters and this dividend may not be so sustainable. In the previous slide where the dividend per share growth was shown, the company indicated that dividends have been growing steadily since 2009. Nothing to object to that, but what happened before 2009?

TIKR Terminal

As we can see, even before the sub-prime financial crisis the dividend per share was rising, but in the moment of maximum distress it was cut. It took five years for it to exceed the 2008 high.

This teaches us that in times of expansion it is easy to increase the dividend per share, but it is when there is a recession that you see which bank was really sound. This happened about 15 years ago, but I think the chances of it happening again are not that low.

After a decade with interest rates close to 0%, in just over a year we find ourselves in a completely different macroeconomic environment and deposit beta is skyrocketing. Of course, yields on assets are also rising, but this means that borrowers are paying more interest and are more distressed than before. NPLs could rise, especially on the commercial side being sensitive to rising taxes. Also, Northrim BanCorp is heavily exposed to it.

So, never assume that past returns can be repeated in the future. Dynamics change and the macroeconomic environment is what makes the most difference.

If you are interested in learning about a regional bank that raised its dividend even during the financial crisis, check out this article on Prosperity Bancshares.