Noble Corporation: Oil Exploration Upside (NYSE:NE)

Ranimiro Lotufo Neto

Macro-economic Overview

Offshore oil appears to be booming again. Following a multi-year hiatus that saw drilling campaigns shelved, projects scrapped, and new builds cancelled, an industrial renaissance driven by high energy prices is rekindling meaningful interest in the industry.

It’s no surprise. Following a global health pandemic that drove energy prices to zero, the industry was decimated. People were shacked up in their homes, industry was halted, and the global economy was put on life support.

Overleveraged offshore oil drillers scrambled to restructure bloated balance sheets with many shutting up shop altogether. Yet only a year or so later, the coupling of a war in Ukraine and debatable US energy policy would provide perfect tailwinds for an industrial rebirth – but a much different one of sorts.

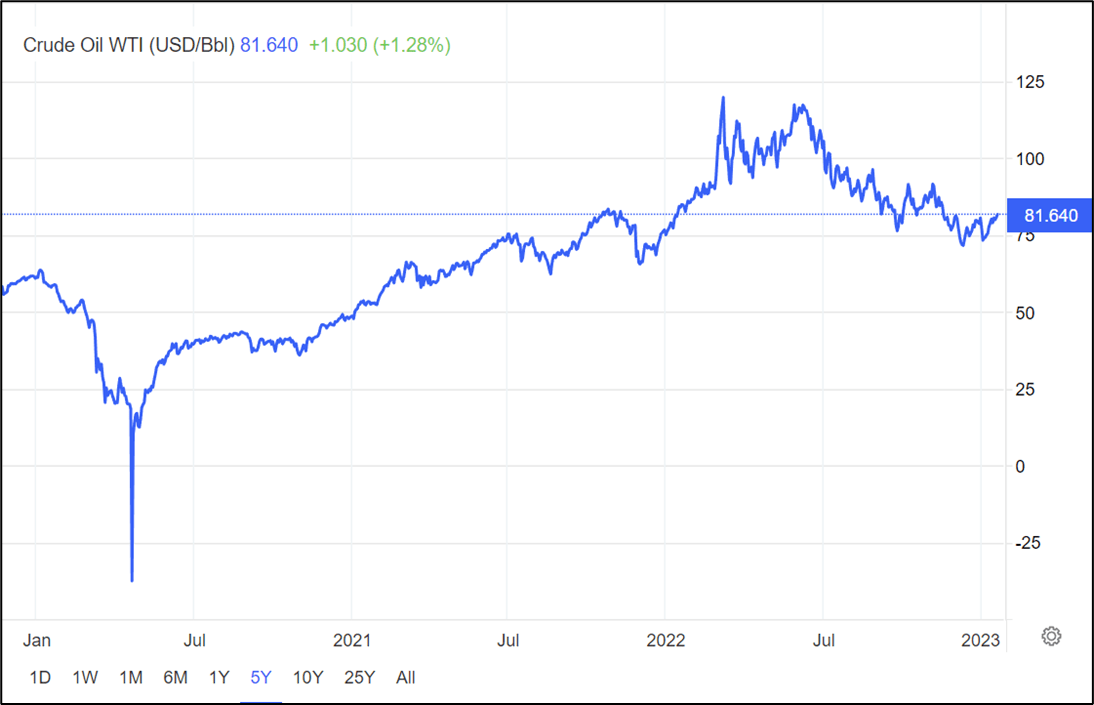

Trading Economics

Energy prices have boomed following the pandemic which saw the market go haywire.

From a proverbial bust to West Texas Intermediate North of $100/bbl, the move to the upside was violent to say the least. But capacity did not follow. Oil & gas companies, burnt already by the shale boom of the 2010s, were taking a much more conservative approach.

Leverage was shunned and only the most select projects with juicy project NPVs were greenlighted. The rest of the cash was returned to investors via distributions. In less than 10 years, the industry had gone from hero to zero. It now appears stardom may well be back on the cards.

Changes in attitudes towards energy have also helped support prices. As supermajors became political punching balls, reluctance to sanction projects gained pace despite a rebound in prices. For the Biden administration, it was un-American to stop drilling.

Yet open courting by the administration of the sustainability industry smacked of irony – how could it possibly drive a narrative beating up big oil, then suddenly kowtow to the industry when all the economic indicators were in the red? Regardless of your view on global energy or politics for that matter, the whole episode was confusing at best.

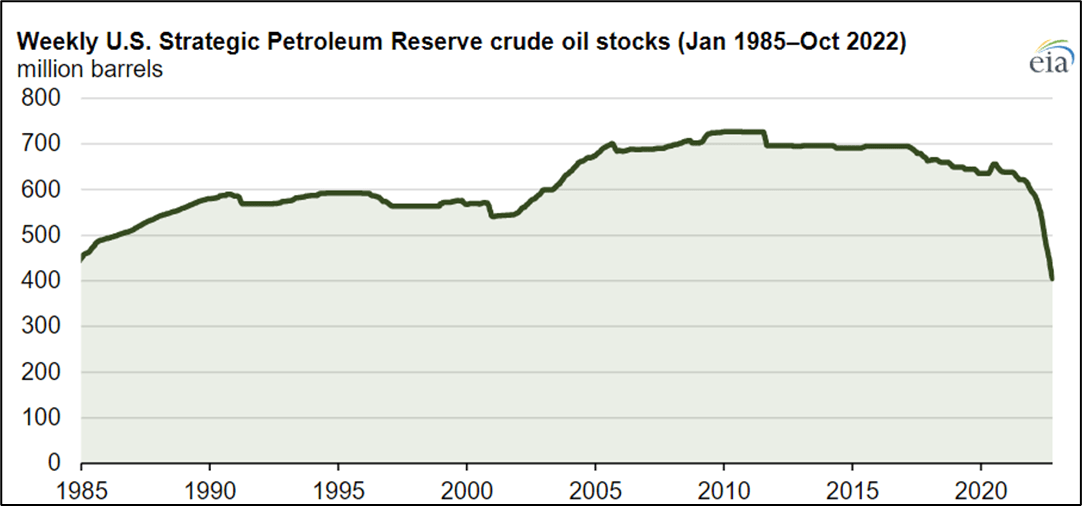

US Energy Information Administration

The Strategic Petroleum Reserve has been depleted by approximately 200M barrels over the past 18 months.

To quell eye-watering inflation driven in part by sky-high energy prices, the present administration drained the strategic petroleum reserve, kicking the can down the road. It has inadvertently set up energy prices for another assault to the upside as dollar strength recedes and the US state becomes a buyer of first order, scrambling to refill the tanks more appropriately used for war-time efforts.

All this paints expectations for global energy, and specifically offshore oil drillers in a positive light. With a global park of 600 offshore units searching the seven seas for black gold, roughly 90% were drilling or under contract to do so at the start of the year. Compare that to five years ago and the number was only about 60%. Little wonder, offshore drillers like Noble Corporation (NYSE:NE) have swagger in their stride.

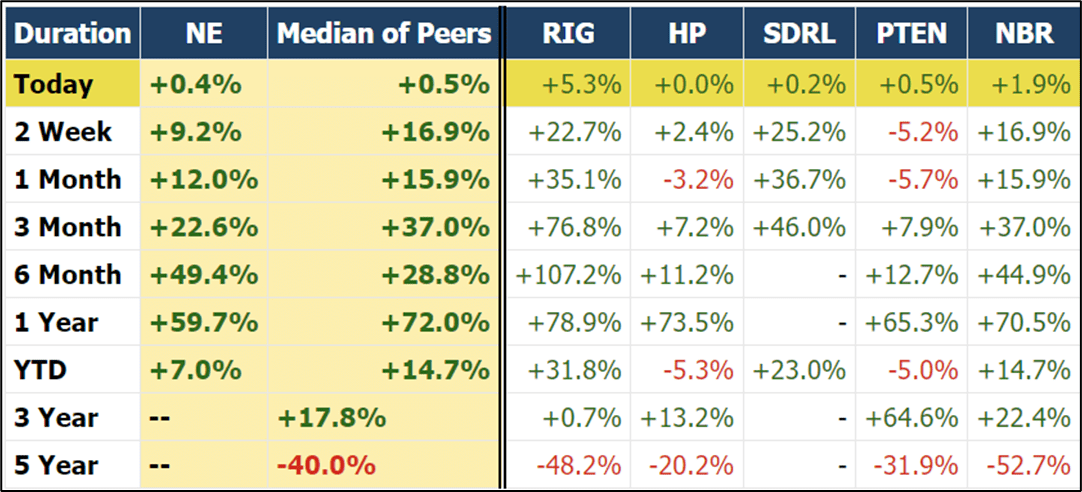

My outlook is bullish for Noble Corporation, along with its peer group including Transocean (RIG), Helmerich & Payne (HP), Patterson-UTI Energy (PTEN), Seadrill (SDRL), and Nabors (NBR).

Market Chameleon

Price action momentum for the offshore oil drillers has been sizable.

Company Introduction

Noble Corporation operates as a drilling contractor for the oil & gas industry worldwide. It provides contract drilling services to global energy players through its fleet of mobile offshore drilling units that include semi-submersibles, drill ships, and jack-ups.

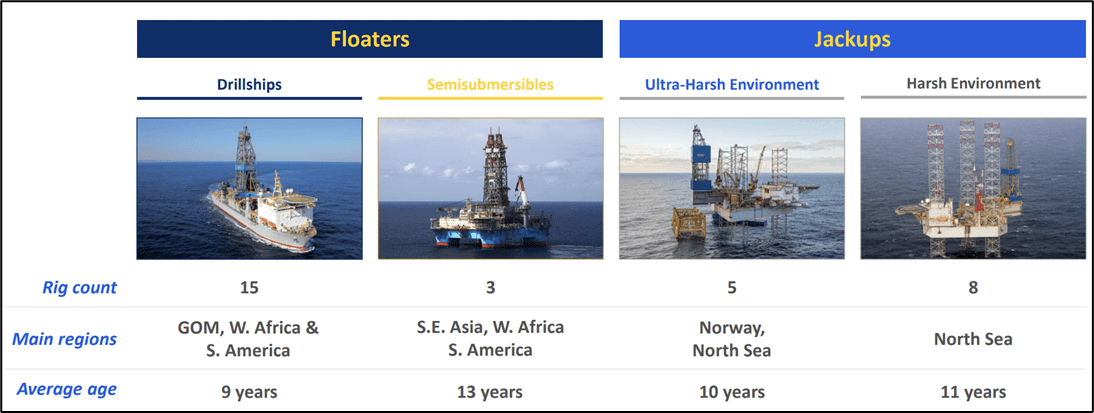

As of November 2022, the combined fleet of Noble plus the Maersk legacy assets comprised of 15 drill ships, 3 semi-submersibles, 5 ultra-harsh jack-ups and 8 harsh jack-ups. That’s telling because a quick look at the fleet of 31 provides some indication of market segments the firm is targeting.

The $5.4B offshore driller has almost a hundred years of history. It’s worth noting that the company is the product of a range of mergers, divestments, carve-outs etc. and has heritage in the US, the United Kingdom, and Scandinavia.

Noble Corporation

The fleet is comparably young, technologically advanced, and strategically positioned across Europe, Asia, Africa & Latin America.

The company recently merged with Maersk Drilling creating further consolidation in the offshore drilling market. The strategic aims were to create a world class offshore driller, boasting a comprehensive fleet of rigs primed to tackle any geography, from harsh but shallow offshore North Sea environments to the deep water pre-salt fields of Brazil.

Thus far, the deal has had regulatory approval, a Noble shareholder vote and a Danish tender offer has progressed positively, creating one of the biggest offshore drilling outfits in the world. With this future marriage, the company touted EBITDA of ~$225M over the last 12 months with 1.9x total debt to EBITDA levels. The combined venture has roughly $4B worth of work in hand.

Noble Corporation

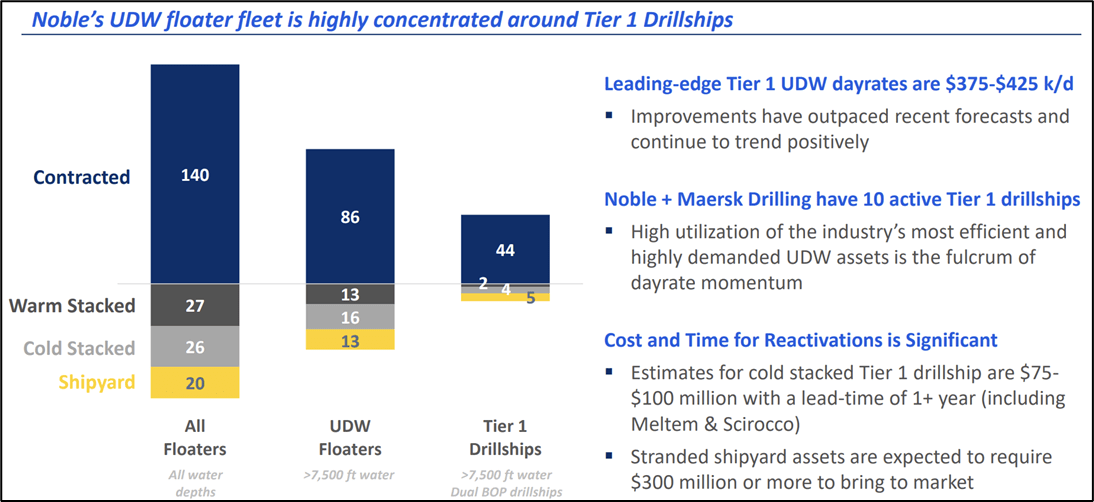

Noble has some of the most technologically advanced UDW floaters – often commanding a premium for their services.

Little is required in reactivation capital for the firm, as opposed to some competitors, as fleet utilization is high (77%) and most units already contracted. This distinguishes the company from rivals who have units cold stacked (parked indefinitely at a port) or warm stacked (moored but ready for immediate deployment if required). Redeploying & reactivating units is extremely onerous.

Noble has consistently dominated the ultra-deep water market with the firm consistently awarded a significant share of backlog. That bodes well for the company – deep water drilling has long been dominated by the pre-salt fields of Brazil.

About 30% of the world’s UDW graded units remain scattered off Brazil’s coast with oil newcomers such as Guyana also garnering strategic interest. Petrobras has plans to splash upwards of $70B in drilling campaigns over the next 5 years, with deep water projects making up the lion’s share. In 2023 alone, roughly 40 exploration projects will come online.

Despite renewed interest in the offshore drilling market, contractors remain wary of committing the same errors made roughly 10 years ago – too much balance sheet leverage, spending on costly ultra-class units, and hasty unit reactivation decisions.

Bringing a stacked unit back online can cost up to $100M so lengthy contracts need to justify the decision. Nowadays, contractors such as Noble are looking to have a sizable amount of that money paid upfront in the contract to de-risk the situation. Wise move.

Key Financials

Noble’s numbers reflect both a conservative strategic approach and a revenue rebirth suggesting additional upside to come. LTM revenues were ~ $940M, up from $782M FY 2021. Gross profits swelled accordingly, with the firm posting $226M over the last twelve months and gross margins of 24%.

That is 2x the gross margins posted by the offshore drilling venture in FY2021. Cash & cash equivalents have increased too, with the firm opting to squirrel away money ($422M LTM v $194M FY 2021) reflecting some of the conservatism in the company’s strategic decision making.

But the real standout feature is the reduction in leverage. Once reputed as being an industry over the hilt, Noble has taken an axe to its debt load, from $3.9B FY 2020 to $434M LTM. That is notable, particularly for an industry that was decimated by copious amounts of debt, the global pandemic and a change in the proverbial interest rate tides.

Noble Corporation

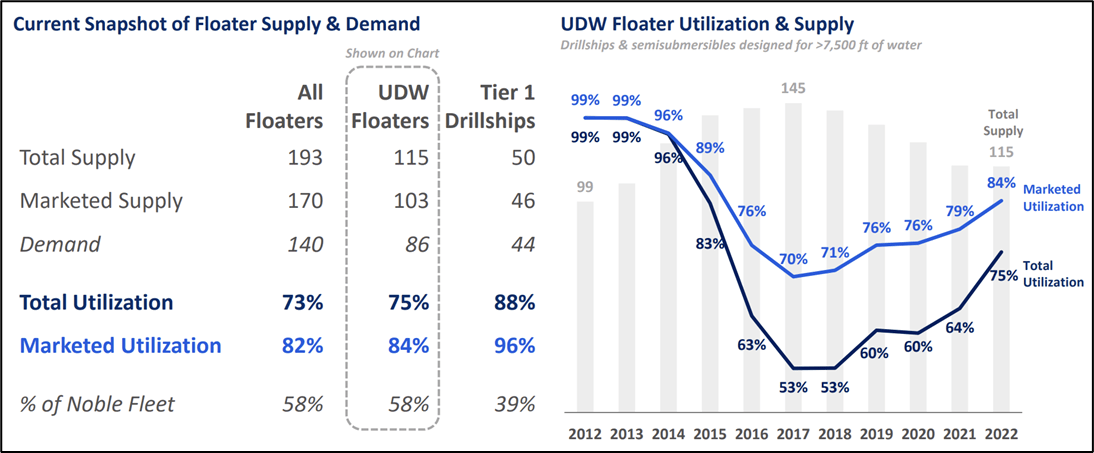

Floater demand is progressively coming back online.

The company has generated $137M in cash flow from operations LTM, yet we are still a ways away from the glory years 2013 to 2015 when the company was regularly posting $1.7B. It does, however, give some idea of upside should we continue to see an oil squeeze.

Risks

While measures have been taken by offshore oil contractors, it’s important to note the risks. The industry has been reputed for its historically egregious amount of leverage that has culminated in industry busts and company bankruptcies.

Conservatism is dominating corporate boardrooms now, but a close eye needs to be kept on both unit reactivations and day rates. Cheap capital meant that large scale shipbuilding flooded the market with new units and pressured day rates. Since then, a lot of units have been taken offline while a notable lag effect existing between demand and added capacity.

Any investor needs to closely scrutinize interest rate movements, the impact on the $US, political and economic stability in Latin America before placing a wager on Noble Corporation, or any other offshore driller.

Key Takeaways

The offshore drilling industry went through a tumultuous bust over the past few years that culminated in company bankruptcies and an industrial reorganization.

Since then, geo-political and macro-economic forces have conspired to push energy to the upside. That’s enough to incentivize super majors to revisit some of their most select offshore projects as a means to bring energy back online.

The offshore drilling industry has hugely benefited from this with Noble, now holding some of the best assets in the industry, primed to reap the benefits. Drill baby, drill.