M/I Homes (MHO): Long-Term Housing Shortage Guarantees Growth

marchmeena29

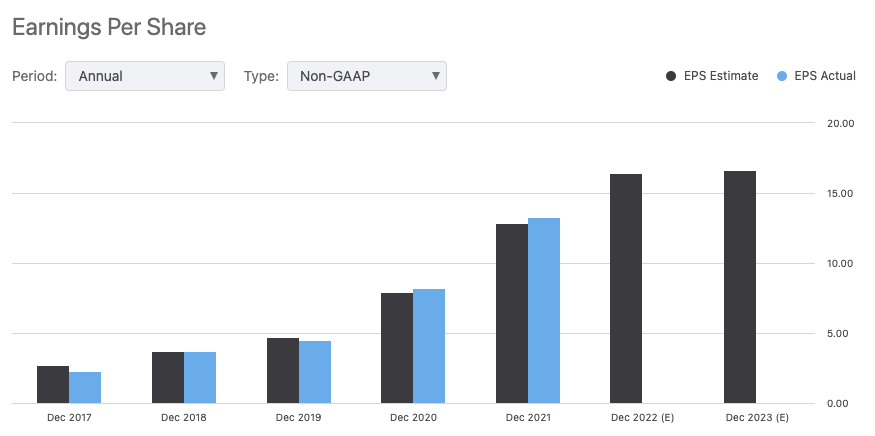

Interest rates have significantly spiked this year, and there is uncertainty about how this will impact the economy. Higher interest rates increase the cost of mortgages and could slow the number of people likely to purchase homes. It has negatively impacted house-building companies on the stock market. One such company is M/I Homes Inc. (MHO), rated as the thirteenth largest home builder in the USA. While MHO has delivered EPS surprises for the last three consecutive quarters, beating EPS expectations by $1.01 to reach $4.79 per share this previous quarter. Simultaneously the stock price has trended downwards year to date by 36.85%. However, one thing we do know is that the demand for housing will not disappear. Statistics show housing shortages in more than 50% of the US metro areas. MHO is an extremely cheap and highly undervalued stock in the industry. Although historically, management has not successfully provided shareholders with good value.

Annual EPS results (SeekingAlpha.com)

The company has had upward trending top and bottom line performance for the last eight consecutive years, and the prediction is that revenue and the number of houses will continue to grow in the coming years. With a one-year target price estimate of $83, more than double the current stock price, and an incredible backlog in sales, I believe there is still a lot of upside potential, and while there is demand uncertainty, this stock is currently undeniably cheap and therefore I would recommend investors take a bullish stance on this company.

Introduction

MHO, previously known as M/I Schottenstein Homes, Inc., is a home-building company with various services founded in 1976 in Columbus, Ohio, by Irving and Melvin Schottenstein. The company builds single-family homes across 16 markets in the United States. It has business in three segments: Northern Homebuilding, Southern Homebuilding and the Financial Services segment, and has built over 140 000 homes. It also provides additional services such as examinations, mortgage solutions, title insurance policies and closing services to home buyers.

The company sells under the M/I Home brand name and targets a wide variety of consumers, from single-family first-time purchasers and young individuals moving up the career ladder to those searching for luxury. In the previous financial year, MHO closed 8,638 houses and generated $3.75 billion.

Financials and Valuation

Although the housing market has felt the impact of the incrementally increasing interest rate, MHO still delivered a solid Q2 performance. The first two quarters have seen a significant reduction in home deliveries, fewer new contracts and an increase in contract cancellations, which investors should be aware of. Homes delivered decreased by 6% to 2,133 homes in Q2 2022. If we look at it over six months, the decrease is even more significant, at 8% year-on-year to 3,956 homes delivered in the first six months. Contracts decreased even further, with a 20% reduction year on year to 2,267 contracts in Q2 2022 and a 19% decrease over the first two quarters of this year to 4,334 new agreements. However, revenue increased year on year by 8% to $1 billion in Q2 2022, and net income increased by 27% to $137 million. The company also still has a backlog of sales valued at $2.7 billion.

The company is financially sound, has no borrowings on its credit facility of $550 million, and has a debt-to-capital ratio of 28% and $189 million in cash. Furthermore, revenue is expected to continue on its upwards growth path over the coming years, irrespective of challenges.

Annual Revenue Growth (SeekingAlpha.com)

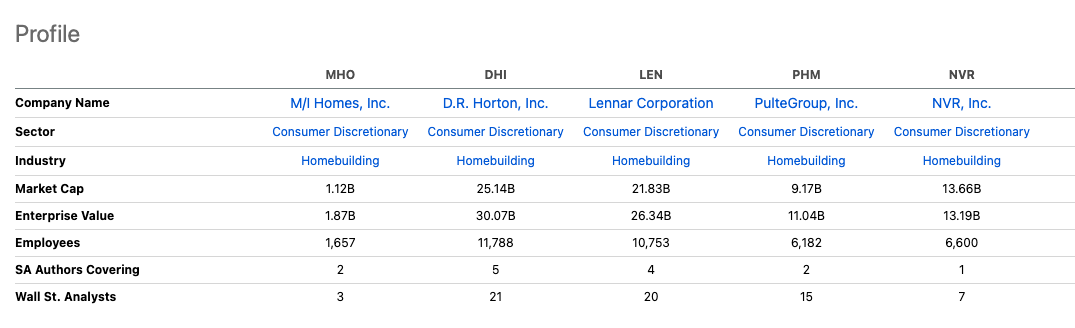

I wanted to compare MHO to the four largest home-building companies in the USA through Seeking Alpha’s Quant rating system to understand better the value this company could deliver to potential investors. As shown in the table below, MHO has a significantly smaller market cap at $1.12 billion compared to its larger peers. We can see that, except for NVR, Inc. (NVR), across the board, these companies are currently worth more than they are selling for.

Peer Valuation (SeekingAlpha.com)

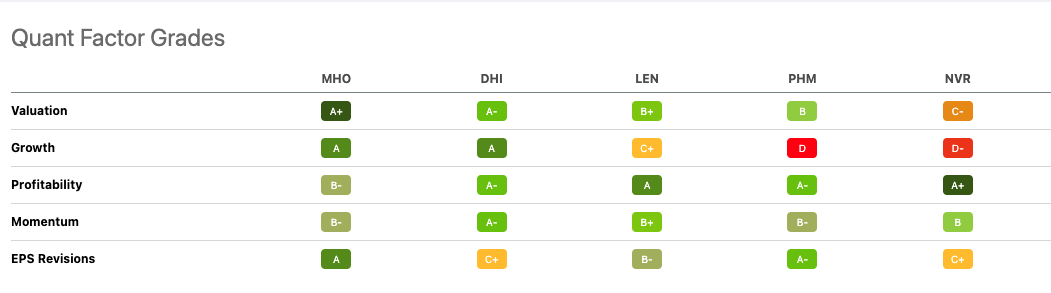

Although MHO does not pay its shareholders dividends, most top-building companies do. It is currently much cheaper than all of its peers, besides PulteGroup, Inc. (PHM), and at the same time, it is showing a firm valuation across Seeking Alpha’s Quant Rating System if we look at the table below.

Quant Factor Grades (SeekingAlpha.com)

If we compare the valuation across these companies, MHO is incredibly undervalued.

Peer Valuation (SeekingAlpha.com)

Risks

The market is not ideal for home buyers, with rising interest rates and inflation. Mortgage rates have increased significantly over the last ten months, and this has already been felt by the company in the reduction of new home contracts signed during the previous six months and an increase in contract cancellations. There is uncertainty as to how long these market conditions will persist.

Final Thoughts

Although we need to be cautious of the market conditions, these are not ideal for home purchasers who are heavily impacted by the surging interest rates and their impact on potential mortgage costs. On the other hand, a significant undersupply of available homes and a demographic still willing to purchase. MHO is positioned in financially affluent communities and is confident in its fundamentals, has low debt levels, and has an incredibly high sales backlog and diverse offerings to succeed in these less-than-ideal economic times. We can see much more potential by comparing MHO to its top-league peers. With a much lower market cap, it is currently undervalued and has much more upside potential. For this reason, I believe that investors may want to take a bullish stance on this company.