Lumentum Holdings: Good Long-Term Potential But Near-Term Is Uncertain (NASDAQ:LITE)

Fertnig

Overview

Despite challenges such as weakened demand and supply limitations, Lumentum (NASDAQ:LITE) exceeded earnings expectations by implementing cost discipline and leveraging synergies from acquisitions. However, the company faces broad-based demand weakness, including reduced demand for datacom modules and 3D sensing, as well as moderate demand for commercial lasers. The Telecom segment is the only area with strong demand, but the revenue outlook is constrained by supply limitations. In particular to the Telecom segment, I have my concern on LITE market position in the value chain. As a component supplier in the value chain, LITE faces greater risk due to its customers’ inventory positions, which can amplify the impact of even slight changes in demand from Telcos and lead to inventory digestion at multiple levels of the value chain. This would easily translate to margin compression on both the gross and EBIT levels.

Altogether, I believe that various factors mentioned above have resulted in management projecting that FY23 revenue will likely align more closely with the low-end of the earlier issued full-year guide. The issue with the guidance, I believe, is that management is assuming that Telecom revenues will improve in F4Q due to an ease in supply constraints. I have my concerns on this as I see increased risks stemming from potential macroeconomic pressures that may lead to conservative spending plans from Telcos and Cloud customers in relation to DCI investments. But overall, I would say that despite the challenging revenue outlook and elevated risks, I believe management should be able to deliver as guided earnings given my expectation that they will likely to continue implement more cost-cutting measures to meet expectations.

Overall, I am optimistic about LITE’s long-term goals, which, if achieved, will result in substantial upside (as shown below). The near-term goals, however, are uninspiring and mired in a great deal of uncertainty. Investors are likely to be cautious about assigning a higher multiple until they have more information about the severity of potential headwinds in the intermediate future. As such, I prefer to stay on the side lines before investing in LITE stock.

Long-term valuation

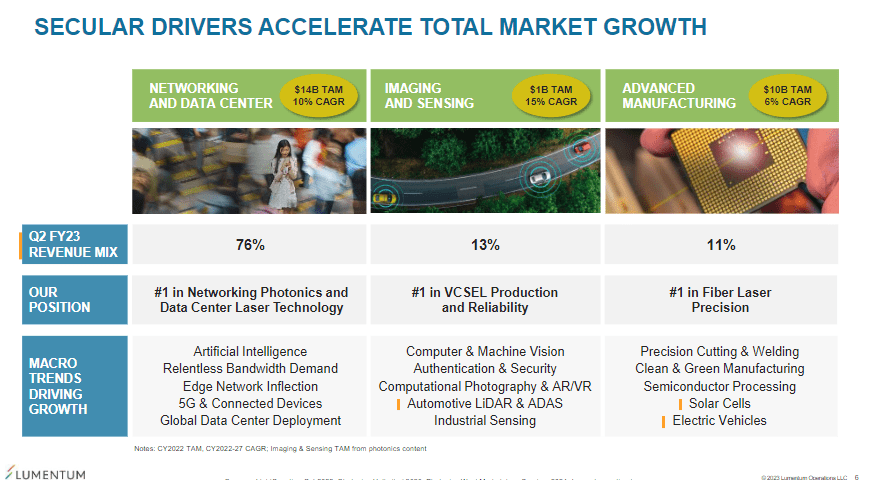

With the latest Investor Day concluded recently, I thought it is interesting to talk about the long-term bull case valuation for LITE. According to presentation, LITE has multiple near-and long-term opportunities to address a $25 billion TAM, inclusive of Networking & Datacenter, Imaging & Sensing, and Advanced Manufacturing markets, which are growing annually between 6% to 15%, positioning the company for robust growth long term. The company also highlighted potential for addressing emerging markets in Image & Sensing, such as in automotive LiDAR and Advanced Manufacturing.

Mar’23 investor day

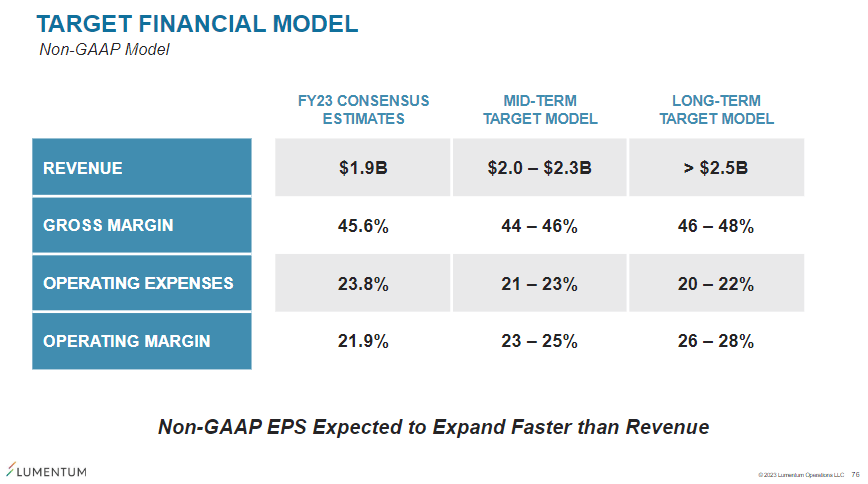

With all the growth opportunities in the backdrop, I believe LITE long-term targets of $2.5 billion in revenue and 26% -28% operating margin in FY26 imply an EBIT of $675 million, which translates to around $8 to $9 of EPS (assuming the same conversion from EBIT to Net income as consensus FY23 estimates). Supposed LITE achieve this, I would expect the market to revalue LITE back to its historical average PE of ~14x. Using $8.50 EPS and 14x forward earnings, that equates to a share price of $119 (more than 2x current share price). That said, the medium-term targets were not as great, but seems reasonable given the uncertainty around the macro.

Mar’23 investor day

Demand and supply situation

Insight into customer backlogs indicates that demand for telecom services remains high, but the rate at which supply is improving remains disappointing. Although Telecom Transport products continue to bear the brunt of supply constraints in comparison to Transmission products, loosening supply for Transport contributed significantly to ROADM revenue growth of 45%. Even though overall supply has improved, supply constraints remain high and decommits have increased in recent times. With the weak supply combined with a weak demand, it has also dampened Datacom’s expectations for FY23. For background, Datacom was expected to recover in 2H23, but is now anticipated to remain weak all the way through FY23. That said, I am not particularly worried on the long-term outlook, given the predicted long-term increase in data consumption. As for 3DS, sales drop was more severe than I anticipated. Weaker demand from the largest customer in the segment contributed to a larger-than-anticipated decrease in 3D Sensing revenue compared to LITE’s own guidance for the quarter. Despite this, the long-term catalyst is found in industrial 3D sensing markets. Management stressed that even though current applications are modest, they have moved beyond the proof of concept stage, with LiDAR-equipped vehicles already hitting the roads in China. By the end of FY24, when LiDAR is standard on most vehicles, these markets are expected to contribute a sizable portion of the company’s total revenue.

Conclusion

While LITE has been able to exceed earnings expectations through cost discipline and leveraging acquisitions, the company faces challenges from weakened demand and supply limitations, particularly in Datacom modules and 3D sensing. The Telecom segment is the only area with strong demand, but the revenue outlook is constrained by supply limitations, and LITE’s market position in the value chain poses risks. Despite these challenges, I believe that management will likely continue to implement cost-cutting measures to meet earnings expectations. Looking at the long-term, LITE has multiple opportunities to address a $25 billion TAM, which positions the company for robust growth in the future. However, in the short term, there is a great deal of uncertainty, and investors may be cautious about assigning a higher multiple until there is more information about potential headwinds. While LITE’s long-term targets imply substantial upside, I prefer to stay on the sidelines before investing in the stock.