EOG Resources Stock: Buy The Dip (NYSE:EOG)

grandriver

EOG Resources (NYSE:EOG) is one of the largest oil and gas companies in the world with a market capitalization of more than $60 billion. The company’s strong assets normally trades at a premium valuation but with its recent 30% drop, we see that as a unique investment opportunity that we recommend taking advantage of.

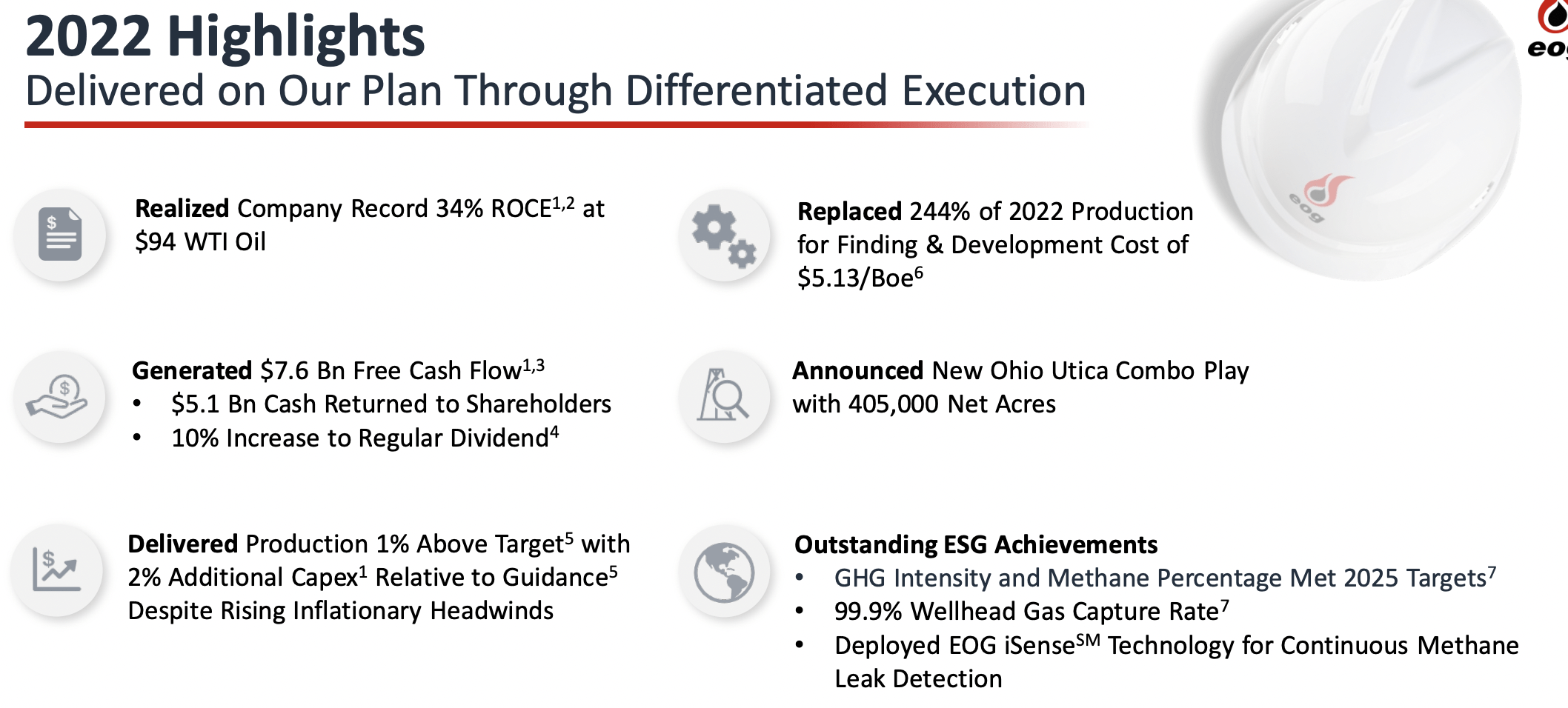

EOG Resources 2022 Performance

EOG Resources had a strong 2022, highlighting its overall asset strength.

EOG Resources Investor Presentation

EOG Resources generated a massive 34% ROCE at $94 WTI. $7.6 billion in FCF resulted in $5.1 billion being returned to shareholders through repurchases and special dividends, along with a 10% increase in regular dividends. The company delivered production 1% above targets with 2% additional capex.

Most importantly the company replaced 244% of its production with an F&D cost at a mere $5.13 / barrel. The company’s new Ohio Utica Combo play has 405 thousand acres. The company had a blowout year, clearly highlighting the incredibly strong upside that’s available in the company’s business when crude prices average higher.

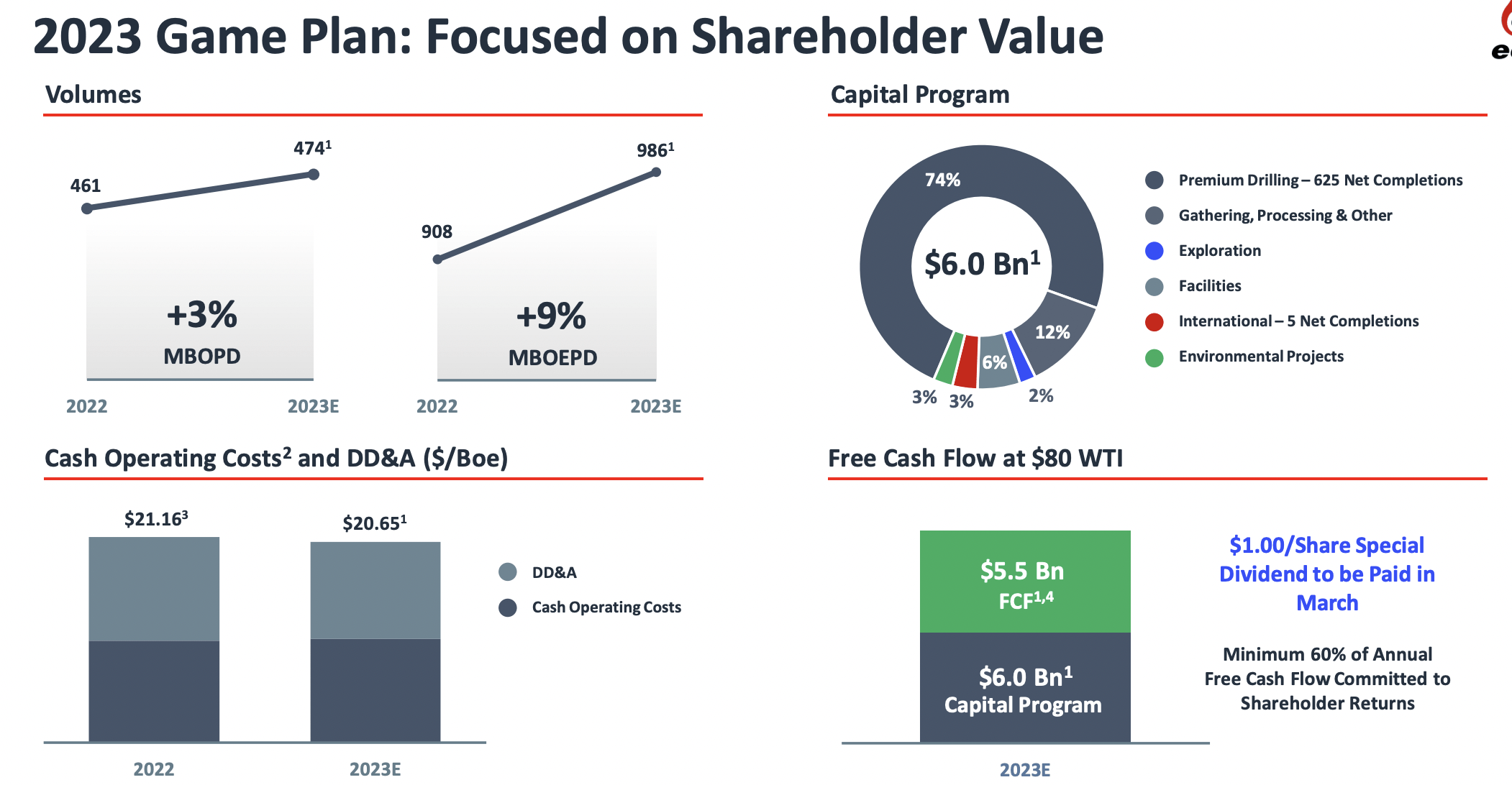

EOG Resources 2023 Plan

EOG Resources has a strong plan in 2023, although it could be heavily affected by lower oil prices.

EOG Resources Investor Presentation

The company’s 2023 game plan assumes $80 WTI and right now that’s looking like a toss-up. China reopening could add substantial demand, however, an inability for the FED to achieve a soft landing could also hurt prices substantially. We truly see it as a toss-up to see where oil prices finish for the calendar year.

However, the company’s numbers are strong. With a large $6 billion capital program, it expects cash operating costs + DD&A to be a hair lower than $20.65 / barrel. That’s impressive in an inflationary environment. The company expects production to increase by a massive 9% in MBOEPD, approaching 1 million barrels / day.

That means that should oil prices drop further, the company has room to decrease capital spending with neutral production.

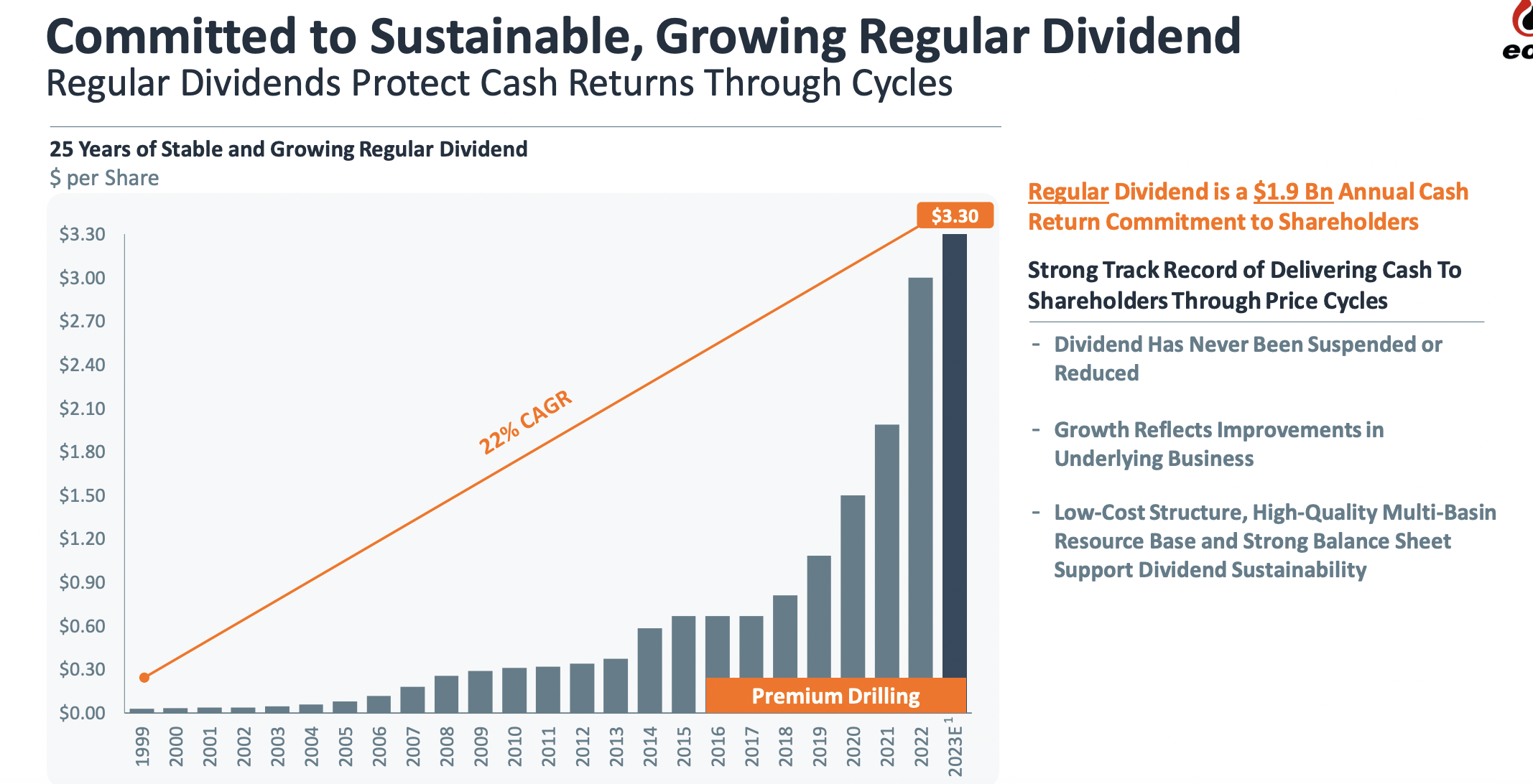

EOG Resources Dividend

The company remains committed to both its dividend and overall shareholder returns.

EOG Resources Investor Presentation

The company’s dividend has grown by 22% annualized as the company has rapidly increased its focus on premium drilling. The current base dividend is 3.1%, however, the company has augmented it substantially with special dividends as part of its return plan. The company has a strong track record of increases during the downturn and we expect that to continue.

At the same time the company has a $5 billion buyback authorization which we’d like to see it take advantage of if share prices drop further. The company’s total special dividends to date have been $5.1 billion, which is more than 8% of special dividends.

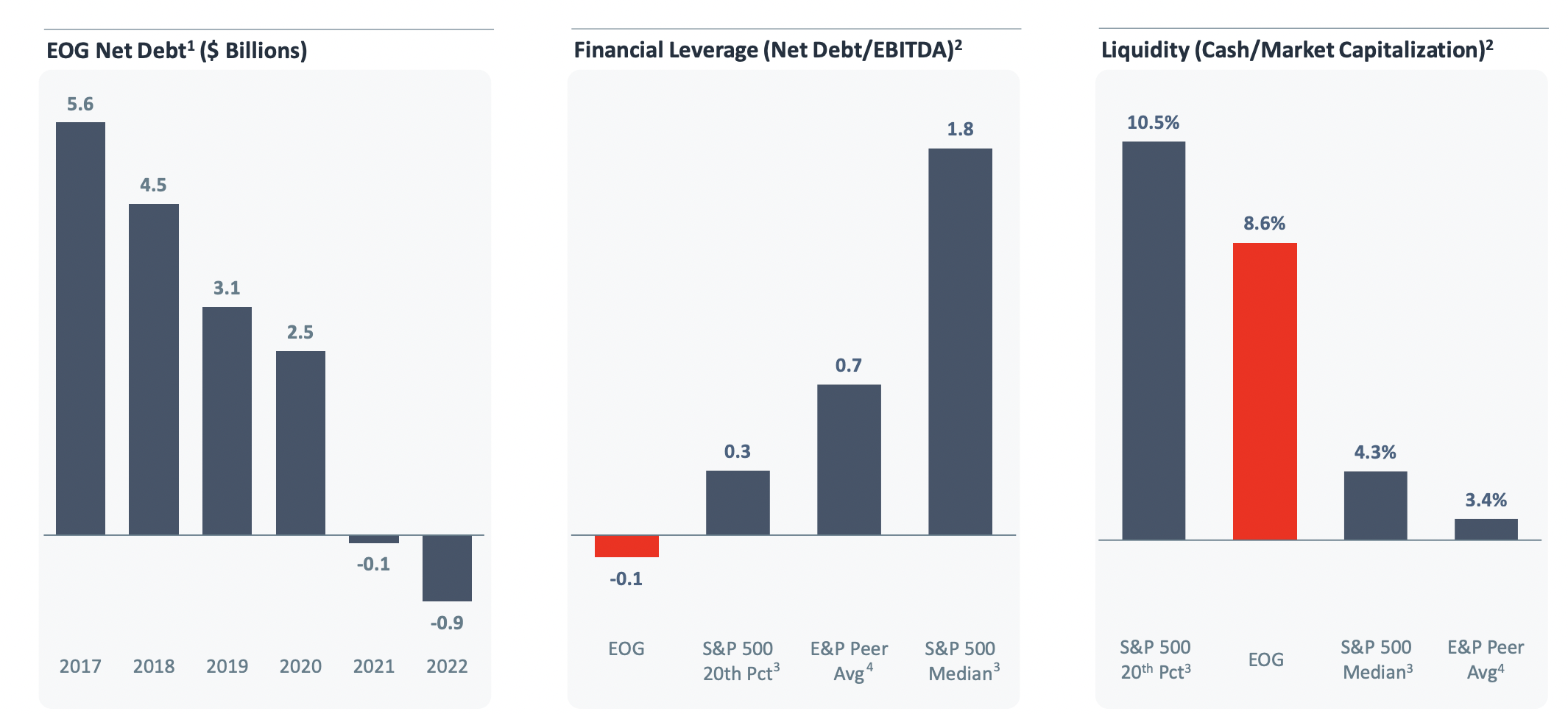

EOG Resources Debt

The company’s balance sheet and debt will enable continued shareholder returns.

EOG Resources Investor Presentation

The company has one of the strongest balance sheets in the industry. It has -$0.9 billion in net debt (i.e. a net cash position) something that highlights not only the strength of its balance sheet but gives it one of the strongest balance sheets in the industry. The company has strong liquidity that means it can opportunistically use cash when available to drive increased returns.

In fact, should the downturn increase further, we’d like to see the company look at some opportunistic acquisitions to support its portfolio.

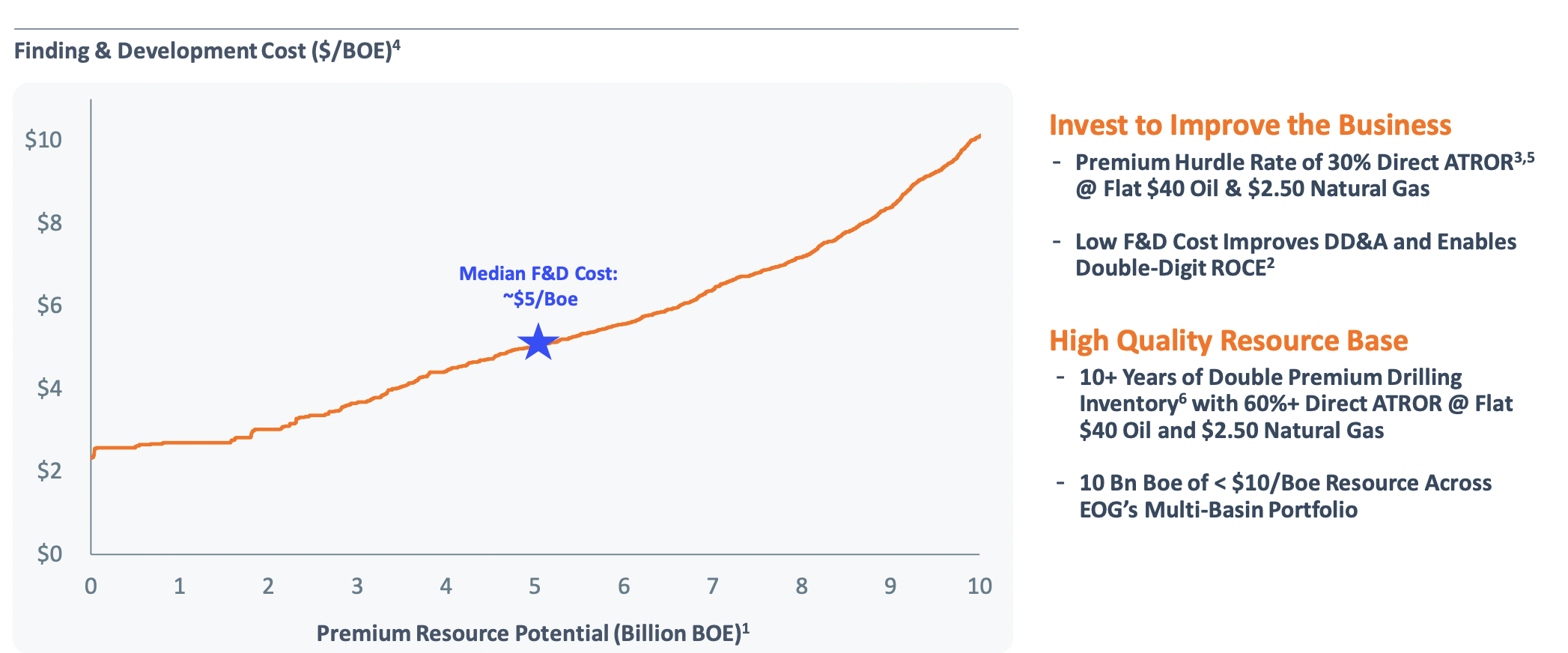

EOG Resources Growth and Margins

EOG Resources is focused on aggressively finding new assets with a low breakeven.

EOG Resources Investor Presentation

The company’s median F&D cost of a mere $5/barrel is incredibly strong. The company has a strong hurdle of 30% ATROR at $40 oil / $2.5 natural gas. The company’s new focus on premium drilling has been maintainable through strong reserve replacements and the current inventory is 10+ years of what the company calls its double premium drilling wells.

The company sees 10 billion of potential <$10/barrel resources across its multi-basin portfolio, equivalent to almost 30-years of production. We expect the company to continue expanding its reserves.

Our View

EOG Resources is a premium company that needs higher prices and a higher valuation to justify its share price.

EOG Resources Investor Presentation

The company has a $62 billion valuation which is actually a fairly strong valuation. The company generated $7.6 billion in FCF in 2022, but that’s easy when you’re realizing a price of $94 WTI. At $80 WTI, the company’s forecast is for $5.5 billion in FCF just after a $6 billion capital program, which represents a 9% FCF yield.

For perspective, current WTI prices are $70 / barrel. There’s a lot of weakness in the economy that could result in prices dropping further, lowering the company’s cash flow into mid single-digits. Still, there’s something to be said about the company’s incredibly strong assets and low breakeven positioning that it has.

Thesis Risk

The largest risk to the thesis is crude oil prices. Prices are already $10 / barrel before the company’s plan for $80 WTI. The company’s hefty $6 billion capital plan, expected to result in almost 10% production growth, means its remaining FCF is much more susceptible to a price downturn. However, with no net debt it can weather a lot.

Conclusion

EOG Resources is a premium company trading at a premium valuation. The company has no net debt and it’s planning to spend $6 billion in capital spending for 2023 to increase its oil equivalent production by almost 10%. However, that use of capital spending means that the company’s remaining FCF is more susceptible to crude oil prices.

The company has a core dividend of just over 3% that it can comfortably afford. Its utilized special dividends and share repurchases in the past and we expect the company will do that as well. However, with major potential volatility going into the end of year, the company is susceptible to what prices do. Regardless, it’s a strong company with strong financials, and as a result, we recommend investing.