Electrolux: 2022 Was Tough And 2023 Won’t Be Better (OTCMKTS:ELUXF)

Scott Olson/Getty Images News

Introduction

It’s been almost two years since I last discussed Electrolux (OTCPK:ELUXF) (OTCPK:ELUXY), one of the largest producers of domestic appliances and the company’s share price has lost about half its value in that time frame. Not exactly what I was expecting so now the company has published its FY 2022 results I wanted to have a closer look at what caused the net loss in 2022 and how the company expects to do better going forward.

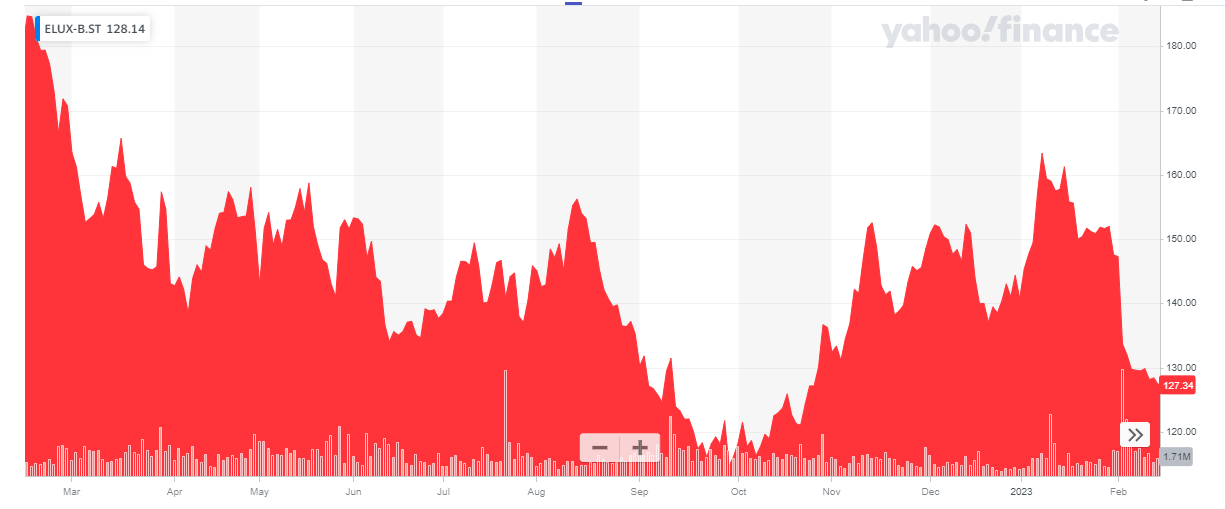

Yahoo Finance

There are two share classes of Electrolux, and I will focus on the B-shares which are trading in Stockholm with ELUX-B as their ticker symbol. The average daily volume is around 1.7M shares per day. The only difference between an A share and a B share is the voting rights. An A share has one full vote, a B share only has 1/10th of a vote. For pure investment purposes, the B-shares are the easiest class to trade. I will use the SEK as base currency throughout this article and where applicable, I will refer to the B-shares as I’m more interested in the best economic value rather than obtaining voting power.

As Electrolux has been buying back shares, its share count has dropped to roughly 270 million shares.

2022 is over, and Electrolux performed poorly

There’s no need to sugarcoat anything: 2022 was a weak year for Electrolux. The company acknowledges the same thing with the title of its Q4 report: ‘Weak finish to a challenging year’.

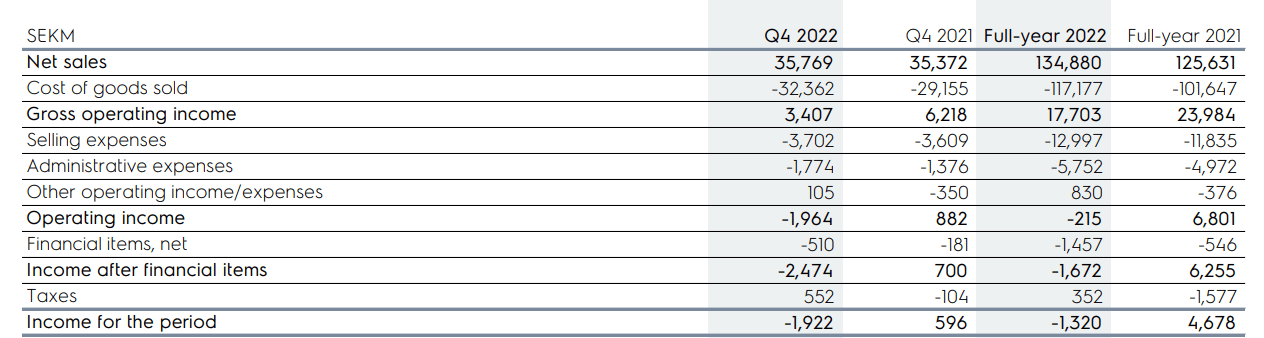

During the final quarter of 2022, Electrolux reported a pretty stable revenue of just over 35B SEK but its sales growth and organic growth rate came in negative (adjusted for FX changes). This happened hand in hand with an increase in operating costs (mainly in the North American division) and this caused an operating loss of just over 600M SEK (excluding non-recurring items). This forced Electrolux to have a closer look at its production chain and the company will focus on cost reduction programs while it will also keep a closer eye on inventory management to make sure it doesn’t produce substantially more than it can sell. The company did well on that front in the final quarter of the year as inventory levels decreased towards the end of the year.

Electrolux Investor Relations

The weak performance is clearly visible in the fourth quarter of the year. The gross operating income fell to just 3.4B SEK, and as this still excludes the SG&A expenses, the operating loss was almost 2B SEK.

Electrolux Investor Relations

The bottom line shows a net loss of 1.9B SEK in the fourth quarter and this obviously had a negative impact on the full-year result as well: Electrolux reported a net loss of 1.32B SEK.

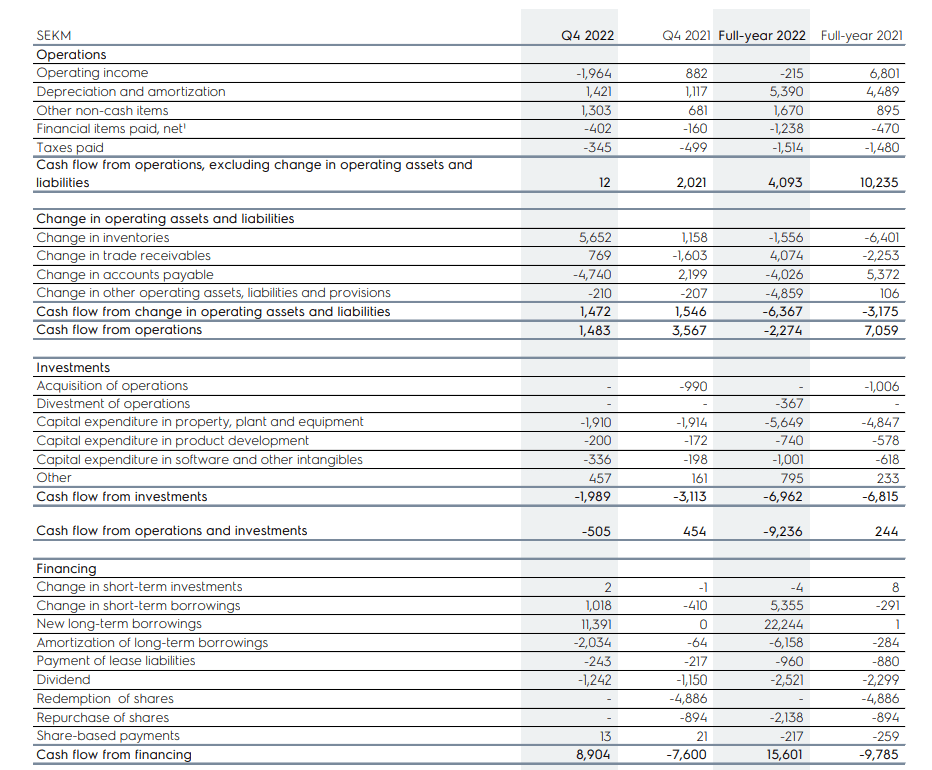

Unfortunately, the cash flow result wasn’t much better. The total operating cash flow in the fourth quarter (before changes in the working capital) was just 12M SEK (this includes about 345M SEK in cash taxes paid, although no taxes were due based on the pre-tax result). But even if we would add that back to the equation and subsequently deduct the 243M SEK in lease payments, the adjusted operating cash flow was still just 114M SEK.

Electrolux Investor Relations

A negligible result, especially when you see the total capex exceeded 2.4B SEK in the final quarter of the year, so Electrolux was definitely free cash flow negative.

Looking at the full-year result, the adjusted operating cash flow was just over 4.6B SEK, but as Electrolux spent about 7.4B SEK on capex (including the 1B SEK spent on intangibles), the company didn’t generate any free cash flow at all.

Fortunately, the balance sheet can easily handle that. As of the end of December, Electrolux had 17.6B SEK in cash, 28.7B SEK in long-term debt and 8.4B SEK in short term debt for a total net debt of 19.5B SEK. As the EBITDA was pretty disappointing in 2022 (with just around 4.2B SEK in EBITDA excluding lease amortizations), the debt ratio appears to be very high, but that’s no immediate reason to be concerned as the EBITDA was much lower than usual (the FY 2021 EBITDA excluding lease amortizations was in excess of 10B SEK).

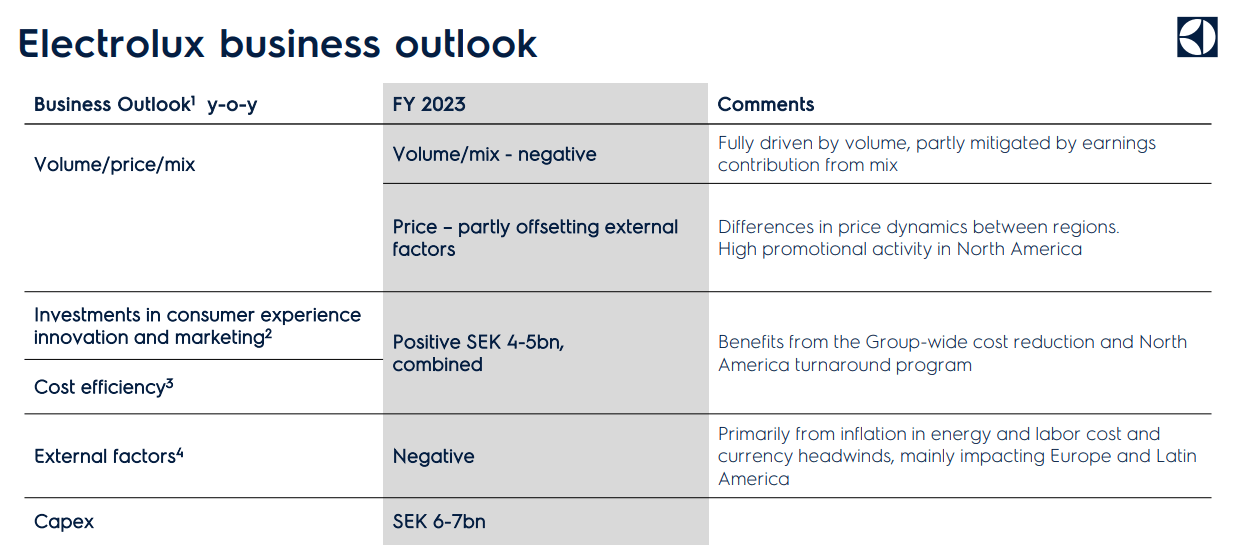

What can we expect in 2023?

2023 isn’t immediately shaping up to get substantially better than 2022. The consumer sentiment remains challenging as the inflation is reducing the consumer confidence levels. Additionally, the housing market will likely be pretty weak this year due to the high interest rates, and this will also weigh on Electrolux’s performance.

On its conference call, Electrolux expects the demand for its appliances in 2023 to decrease in Europe and the Americas while the Asian, Middle East and African regions will likely stabilize. Electrolux is hoping for an uptick in the demand for its appliances from the second half of this year on, as inflation rates are going down.

Electrolux Investor Relations

There’s also not a whole lot Electrolux can do to hike prices. If the demand is already expected to decrease, hiking prices too aggressively may further erode demand. As such, Electrolux does not expect to be in a position to fully offset the impact of inflation and higher operating expenses by price hikes in 2023. An additional complicating factor is that although the prices of raw materials are going down, Electrolux is still working through the raw materials it ordered last year at higher prices and this will continue to weigh on the margins.

Investment thesis

2022 was a very tough year and it doesn’t sound like we should expect a substantial improvement in 2023. Electrolux seems to expect the demand to pick up again in the second half of the year, but that also implies H1 will be pretty weak again so perhaps we shouldn’t expect too much from Electrolux this year.

I do hope the company can get its act together and perhaps there will be a new opportunity to buy the shares during this year, ahead of an anticipated improvement in 2024. Electrolux will not pay a dividend based on its FY 2022 results so there is no urgent need to initiate a long position. Whirlpool (WHR) has posted a more upbeat outlook for 2023 with an anticipated $800M free cash flow and an EPS of $16-18 per share. As far as exposure to domestic appliances go, Whirlpool seems to be in a better position than Electrolux these days.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.