Crestwood Equity Partners: Get A Solid 10.3% Yield On The Drop (NYSE:CEQP)

zorazhuang

Units of Crestwood Equity Partners (NYSE:CEQP) currently supply dividend investors with a 10.3% dividend yield that is well covered by the midstream company’s distributable cash flow. Crestwood Equity Partners delivered a strong earnings sheet for the fourth-quarter in February and the company has submitted a capital budget that indicates that the distribution has room to grow. Due to the recent drop in the unit price of Crestwood Equity Partners, I am adding to my position because the distribution is safe, in my opinion, and has potential to grow in the mid-single digits in FY 2023! Read our previous coverage on CEQP here.

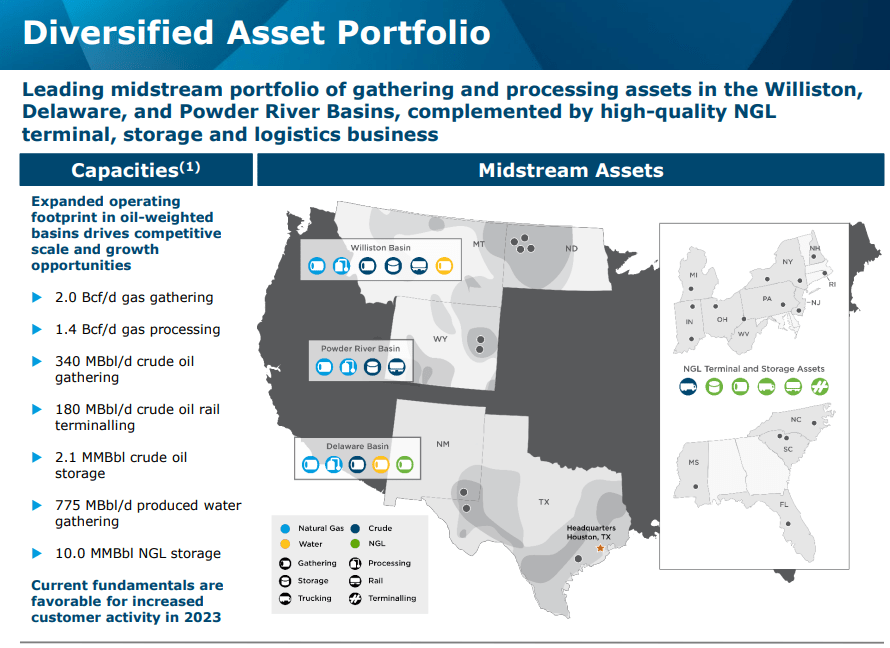

Asset base and fee-based revenue structure

Crestwood Equity Partners is a growing midstream company with investments in the Willison, Delaware and Powder Basins and chiefly offers natural gas gathering and processing services to its customer base. The midstream firm also offers terminalling and storage services to its producer clients and plays a critical role in bringing energy products to markets across the US. The most attractive aspect of an investment in Crestwood Equity Partners is that the company generates predictable distributable cash flow from its midstream transportation assets.

Source: Crestwood Equity

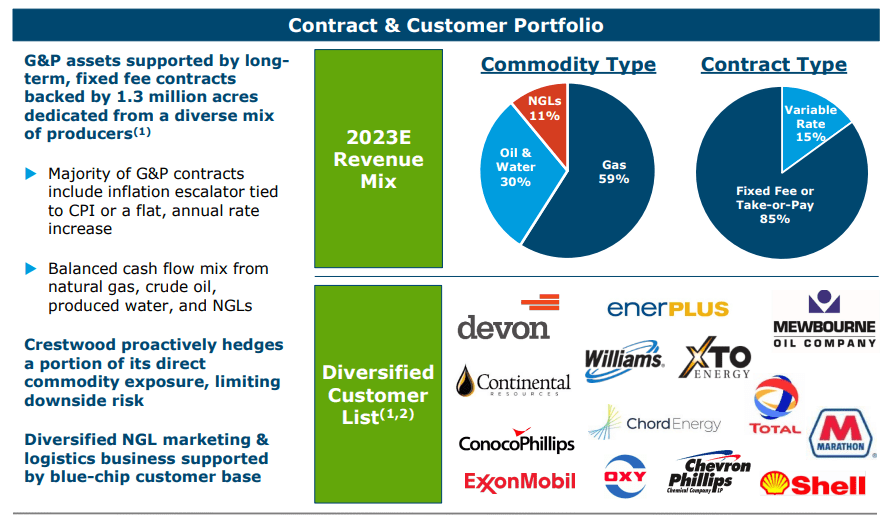

The reason I like Crestwood Equity Partners is because the company’s operations are largely based on predetermined fees which gives CEQP resilience in a market that very often sees large changes in market prices for energy products. As opposed to producers, midstream firms like Crestwood Equity Partners get paid a fixed fee for their transportation, storage and terminalling services which greatly limits exposure to the volatility of energy market prices. Crestwood Equity Partners expects to generate an 85% fee share in 2023 which gives the midstream firm very predictable revenues and cash flows.

Source: Crestwood Equity

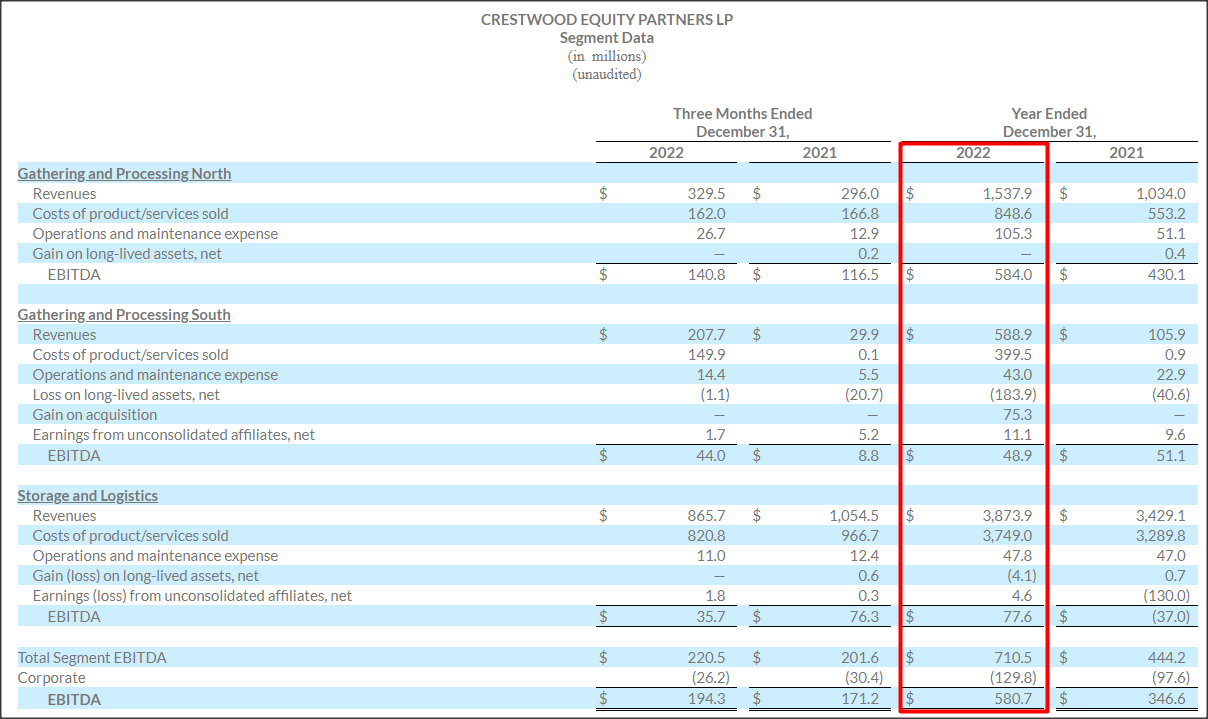

FY 2022 EBITDA and DCF-based coverage

Crestwood Equity Partners generated $580.7M in EBITDA in FY 2022, showing 68% year over year growth, largely because of strong growth in the company’s Gathering and Processing North segment which includes a combined 641 MMcf/d natural gas gathering capacity related to the Williston Basin (Montana/Dakota) and the Powder Basin (Wyoming). The Gathering and Processing North segment contributes the majority of Crestwood Equity Partners’ EBITDA and also receives the majority of the company’s CapEx budget.

Source: Crestwood Equity

Crestwood Equity Partners’ adjusted EBITDA was $762.1M in FY 2022, showing a 27% increase year over year due to growth investments paying off chiefly in the Delaware and Willison Basins. The firm’s total distributable cash flow in FY 2022 was $466.6M which translates to a distribution coverage ratio of 1.8 X which was in accordance with the company’s guidance of a distribution coverage range of 1.8-2.0 X.

Outlook for FY 2023

Crestwood Equity Partners presented its guidance for FY 2023 in February which sees adjusted EBITDA of $780-860M and growth investments in the amount of $135M to $155M. More than half of Crestwood Equity Partner’s CapEx (55%) will go to the company’s Gathering and Processing North segment in FY 2023. Crestwood Equity Partner’s Gathering and Processing North segment is expected to generate the majority of FY 2023 adjusted EBITDA of $570-620M which translates to an EBITDA share of 72-73%. The adjusted EBITDA outlook for FY 2023 also implies up to 13% year over year growth.

Source: Crestwood Equity

The most important guidance metric for FY 2023 was CEQP’s expected distribution coverage ratio because it allows investors to evaluate the possibility of a major distribution increase. Crestwood Equity Partner said that it expects its distributable cash flow to be between $430M and 510M and distribution coverage is expected at 1.6-1.8 X.

Potential for distribution growth due to high DCF-based coverage ratio

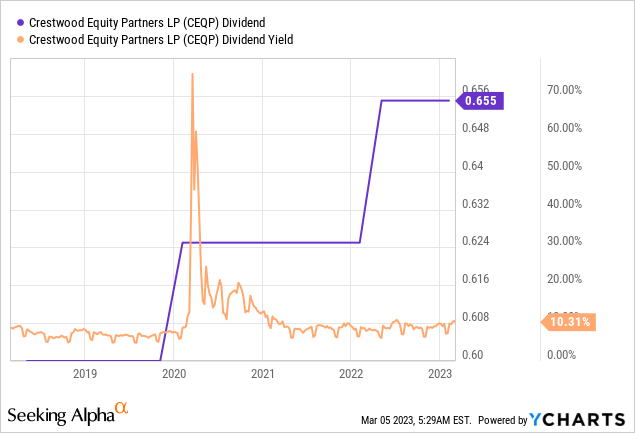

Crestwood Equity Partners raised its distribution 5% in FY 2022 and with a projected DCF-based coverage ratio of at least 1.6 X this year, I believe the midstream company could grow its distribution in the mid-single digits in FY 2023. The midstream firm’s units currently yield 10.3% and management has been constructive regarding distribution rate increases in the past.

CEQP’s valuation vs. rivals

I believe there is an opportunity to take advantage of the CEQP unit price drop that has occurred lately. Based off of Crestwood Equity Partners’ outlook for FY 2023, the midstream firm’s units are valued at 5.7 X FY 2023 distributable cash flow. Units are also valued at an EV/EBITDA ratio of 7.7 X which makes CEQP both attractively valued on a distributable cash flow and EBITDA basis. Other companies in the midstream segment — such as Enterprise Products Partners (EPD) or Kinder Morgan (KMI) — all trade at significantly higher EV/EBITDA multipliers, but are also significantly larger in size than CEQP.

Risks with Crestwood Equity Partners

Crestwood Equity Partners is a midstream business with extensive investments in the fossil fuel industry (natural gas) which has become a target of the US government. Regulatory agencies are trying to incentivize the use of green energy sources and disincentivize the use of fossil fuels which could affect CEQP’s growth and distribution potential. Crestwood Equity Partners is dependent on growth investments in the Williston, Delaware and Powder River Basins and limits place on the company’s expansion are likely going to result in slowing cash flow growth and potentially weaker distribution coverage going forward.

Final thoughts

I am buying the drop in the units of Crestwood Equity Partners because the company is well managed and more than earns its dividend with distributable cash flow… which is the prime requirement for me to buy a midstream investment for yield. Crestwood Equity Partners had a distribution coverage ratio of 1.8 X in FY 2022 and the projection for FY 2023 (1.6-1.8x) implies that the distribution will continue to grow. Since CEQP is cheaply valued based off of DCF and EBITDA, and supplies a dividend yield in excess of 10%, I believe Crestwood Equity Partners is worth the risk!