China Policy Key For Iron Ore Outlook

Çağla Köhserli/iStock via Getty Images

By Warren Patterson, Head of Commodities Strategy

China’s covid lockdowns and recessionary risks hit iron ore

Iron ore prices have fallen significantly from their year-to-date high of US$171/t seen back in March to as low as $108/t recently. China’s attempts to squash outbreaks of Covid-19 have seen fairly tough restrictions, which have not been supportive of demand. In addition, there are growing concerns over the macro-outlook. Soaring inflation is seeing central banks, particularly the US Federal Reserve having to take a more aggressive approach to monetary tightening. The concern is that the Fed will struggle to rein in inflation without pushing the US economy into recession. Ultimately though the iron ore outlook is going to largely depend on how China approaches any further Covid outbreaks through the year as well as the scale of stimulus we see the government unleashing.

China steel output lags but there’s room to recover

Chinese steel output has been under pressure for much of the year. The start of 2022 saw output cuts in some regions during the winter Olympics weigh on national output, whilst in more recent months Covid lockdowns have weighed further on both steel demand and supply. According to government data, cumulative crude steel production over the first five months of the year totaled a little more than 435mt, down 8% year on year.

China’s state planner has made it clear that it wants crude steel production capped at below 2021 levels, which on the surface sounds bearish for iron ore. However, given the lower steel output seen so far this year, it does leave mills with room to increase output, whilst still keeping output below 2021 levels. China produced 560mt between June and December last year. And assuming that the full year 2022 output at most matches last year’s levels, this leaves the potential for up to 600mt of production over the remainder of the year, almost a 7% increase year-on-year.

However, whether the demand is there really depends on the steps that China takes to try to hit its growth target of 5.5% for 2022. China’s zero-Covid policy means this target will be extremely difficult to achieve. China has already announced stimulus measures to try and help growth, which would include a boost in infrastructure spending. Infrastructure projects are generally metals-intensive and so should be supportive of steel demand.

The industry also has a considerable amount of steel inventories to eat into. The latest data from the China Iron & Steel Association shows that inventories at major steel mills stand at 20.5mt, up almost 82% since the start of the year and 30.8% higher year-on-year. Bloated inventories have weighed on domestic steel prices, which has seen margins shrink. Therefore, the industry will need to draw this stock down to more normal levels before we can see a meaningful recovery in margins.

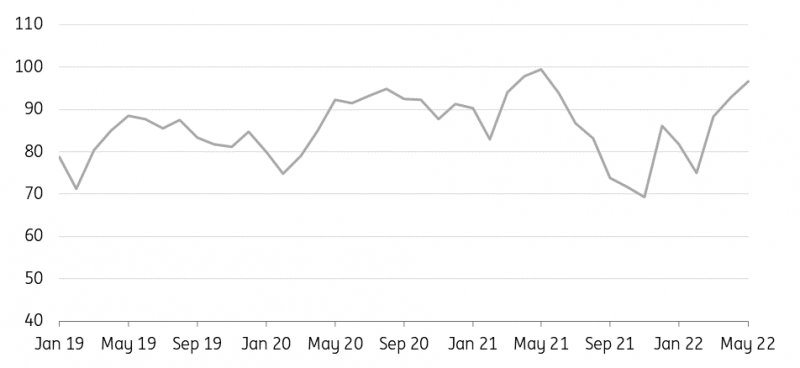

China monthly crude steel output (m tonnes)

WSA, ING Research

China iron ore imports lagging

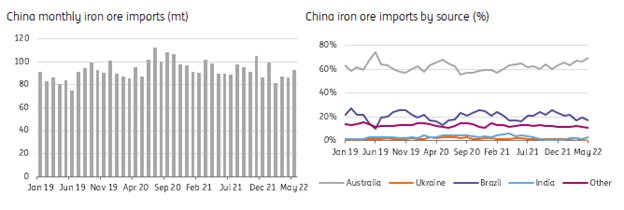

It is no surprise that with lower steel output from China iron ore imports have also been under pressure so far this year. The latest trade data shows that cumulative imports over the first five months of the year totaled almost 447mt, down around 5% year on year. Naturally, if there is an upside in steel output over the second half of this year, we would expect to see stronger import demand for iron ore. Port inventories have been drawn down quite considerably over the last few months. The latest data from SteelHome shows that port inventories stand at around 124mt, down from a little more than 160mt earlier this year. Stocks are at their lowest levels in a year, and below the five-year average of close to 130mt for this stage of the year. These lower stocks and the more recent pressure we have seen on iron ore prices could attract some Chinese buying interest.

Looking at the origins of Chinese iron ore imports, Australia remains the largest source of supply by a mile, with about 69% of imports originating from Australia in May. In fact, Australia’s share of total Chinese imports has grown a fair amount over the last couple of years, when you consider that Australian supply made up 56% of total imports in August 2020. This suggests that the Australian iron ore industry has been largely unaffected by the deterioration in relations between China and Australia. Although, the Chinese government is reportedly looking to centralise procurement of iron ore, with the hope it gives buyers more bargaining power with producers in the future.

China iron ore imports slow

NBS, ING Research

It’s not just China where steel output is under pressure

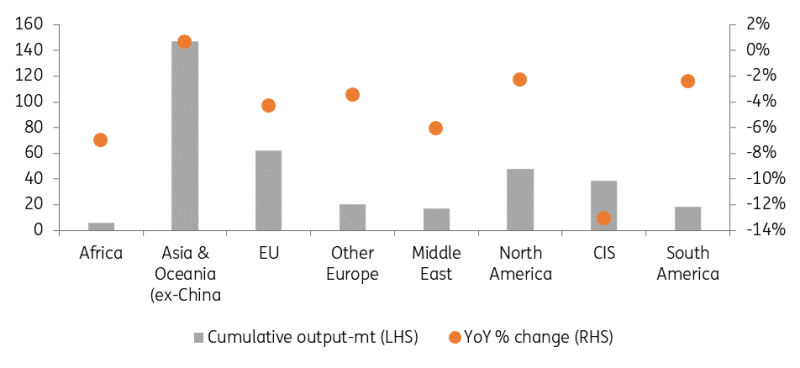

Ex-China steel output has also struggled this year. The latest data from the World Steel Association shows that cumulative ex-China output totaled around 357mt over the first five months of the year, down a little more than 3% year on year.

Declines were led by the CIS where year-to-date production is down more than 13% year-on-year, and unsurprisingly this is largely a result of the ongoing Russia-Ukraine war. European output has also been under pressure this year, with higher energy prices leading to some cuts. In addition, weaker downstream demand, particularly from the auto industry, has not helped.

India is the standout when it comes to steel production, with it managing to grow whilst production has fallen elsewhere around the world. This growth from India has meant that cumulative ex-China Asian steel output managed marginal year-on-year growth over the January-May period.

Expectations of slowing economic growth, and the growing risk of recession, are clearly not great for global steel demand. The World Steel Association had previously assumed that steel demand growth would be rather tepid this year, growing at just 0.4% year-on-year, before growing by 2.2% in 2023. Clearly, given the gloomier macro-outlook, there could still be a downside to these numbers.

Ex-China cumulative crude steel production by region (Jan-May)

WSA, ING Research

Australian iron ore supply to edge higher

Australia is in the process of ramping up supply from a number of new projects, of which the largest is BHP’s (BHP) 80mtpa South Flank mine which started operations in 2021. This follows the startup of Fortescue’s (OTCQX:FSUMF) (OTCQX:FSUGY) 30mtpa Eliwana mine which commenced operations in late 2020 and has ramped up output since. For this year, Rio’s (OTCPK:RTPPF) (OTCPK:RTNTF) 43mtpa Gudai Darri mine started operations in June, while Fortescue was meant to start operations at its 22mtpa Iron Bridge mine this year, but the start date of this has been pushed into 1Q23. These new projects, along with some expansion projects, should mean good supply growth from Australia this year and next.

However, so far this year production has disappointed with labour constraints related to Covid-19 impacting operations. This is reflected in export numbers, with exports over the first four months of the year up just 0.5% year-on-year. Although, weaker Chinese demand will also be a factor in these export numbers.

Brazilian shipments suffer this year

Brazil has struggled to see iron ore shipments return to levels prior to the Brumadinho dam disaster in January 2019. In 2021, total Brazilian iron exports totaled 358mt, still down from the almost 371mt exported in 2018. And it would appear that exports in 2022 are going to struggle as well, with cumulative exports over the first five months of the year totaling a little over 122mt, down 8% year-on-year. In fact, February saw Brazil exporting the lowest volumes since February 2014. Weaker exports have been a result of disruptions following heavy rainfall earlier in the year.

Despite the disruptions seen this year, Brazilian miner Vale (VALE) continues to maintain its production guidance for 2022 in the range of 320-335mt, compared to the production of almost 316mt last year. Looking further ahead, Vale still aims to reach 400mtpa of annual capacity.

Iron ore prices to ease in the longer term

While we expect iron ore prices to be supported in 2H22 due to expectations of a recovery in China, the longer-term outlook for iron ore is more bearish. On the demand side, it appears that China will continue to cap crude steel output whilst also looking to replace older steel capacity with electric arc furnace capacity in order to help the country meet its decarbonisation goals. Growth in electric arc furnace (EAF) capacity at the expense of basic oxygen furnace (BOF) capacity will be a concern for the medium to long-term outlook for Chinese iron ore demand. It also suggests that we have already seen China’s iron ore imports peak in 2020.

As for the supply picture, we should continue to see the ramping up of supply from new projects in Australia, along with Vale in Brazil continuing to target an annual production capacity of 400mtpa.

More sluggish demand from China, combined with this supply growth, suggests that prices should trend lower in the medium to longer term. As a result, we see 62% Fe fines averaging US$105/t in 2023 and US$90/t in 2024. This is down from US$138/t over 2H22.

Content Disclaimer

This publication has been prepared by ING solely for information purposes, irrespective of a particular user’s means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Editor’s Note: The summary bullets for this article were chosen by Seeking Alpha editors.