Blue Bird Stock: This Rally Looks Like Enough (NASDAQ:BLBD)

jhorrocks/E+ via Getty Images

Blue Bird (NASDAQ:BLBD) is coming out the other side. The school bus manufacturer worked through an exceptionally difficult fiscal 2022 (ending September), during which time the company faced a number of challenges.

Parts shortages significantly delayed production, pushing out deliveries which had to be made at previously-contracted pricing. But commodity and labor inflation meant that pricing didn’t cover costs: Blue Bird posted an Adjusted EBITDA loss of $15 million in fiscal 2022.

That loss, however, did not appear to suggest that the business was losing market share, or that school bus demand was permanently impaired. Blue Bird simply faced a perfect storm of problems, a storm that 18 months ago I argued the company would work through, making BLBD stock a buy.

So far, that story has largely played out. This month’s fiscal Q2 report looked much better, with Blue Bird raising full-year FY23 guidance and expressing optimism going forward. With the cycle now turning in the company’s favor, BLBD has rallied 268% from October lows.

After that monster rally, the question is what comes next. Honestly, it’s not a terribly easy question to answer.

Blue Bird Stock – Backward-Looking Valuation

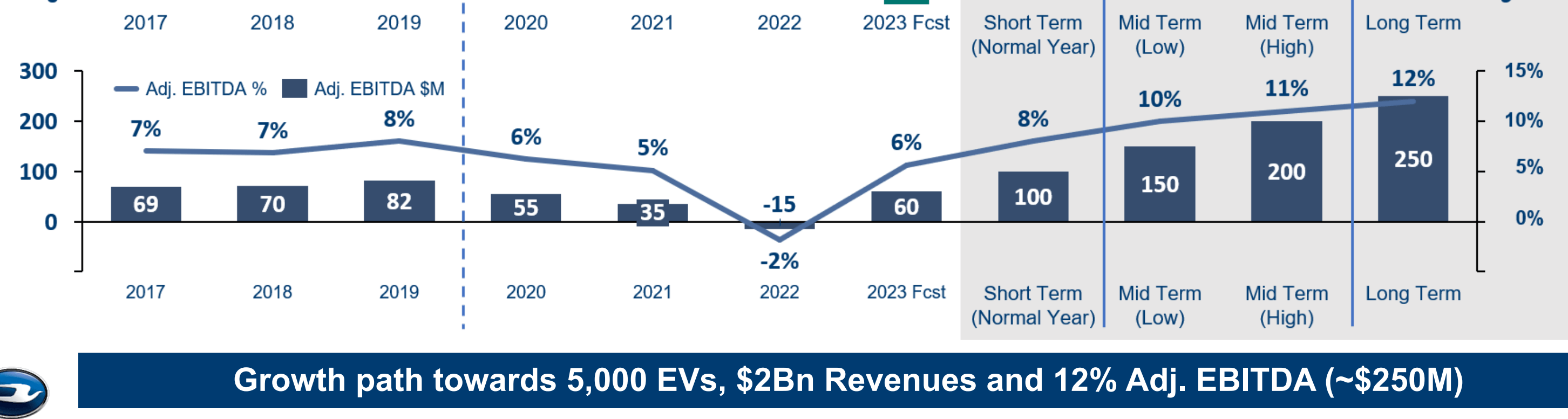

In its most recent investor presentation, Blue Bird itself lays out its historical and projected Adjusted EBITDA. The slide shows just how cyclical this business has been – and shows how much growth Blue Bird expects going forward:

Blue Bird investor presentation, May 2023

The significant variance here alone makes valuing BLBD stock a challenge. Post-Q2, the company has an enterprise value just shy of $1 billion, with a fully-diluted market cap of ~$850 million and net debt of $122 million.

Based on FY23 guidance, for Adjusted EBITDA of $55-$65 million, BLBD trades at about 16x on an EV/EBITDA basis. The P/E multiple is in the range of 50x at that level; based on year-to-date capital expenditures, price to free cash flow a lower, but still high, 35x or so.

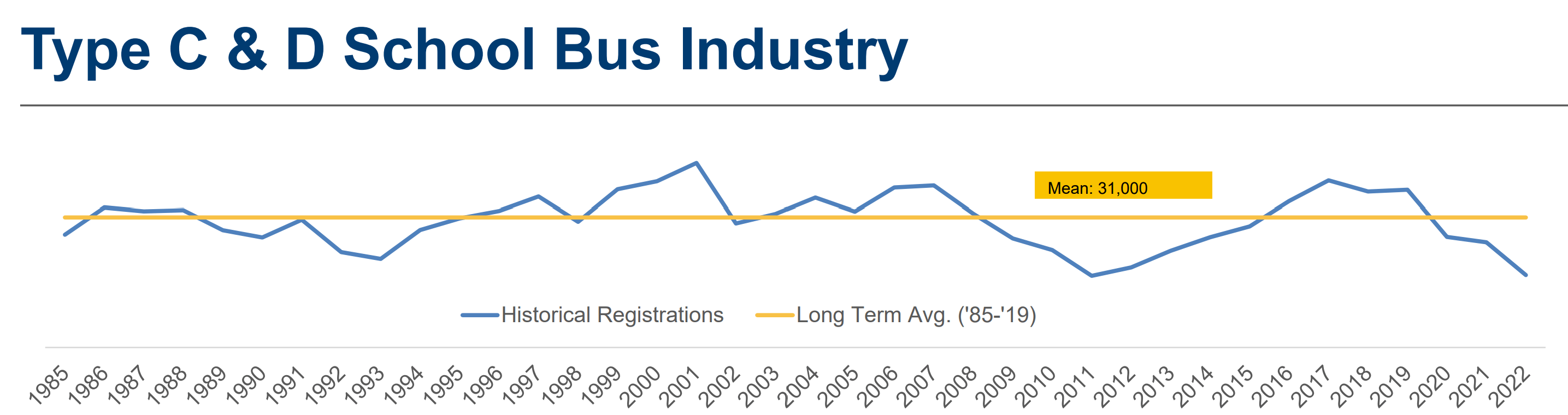

Valuation looking backward too looks rather concerning. Based on average annual Adjusted EBITDA from 2017 to 2019, BLBD trades at ~13x EBITDA and likely a high-20s multiple to normalized free cash flow. It’s worth remembering that those pre-pandemic years actually benefited from not only lower input and labor costs, but a cyclical upswing in demand. During those years, school bus registrations in the U.S. were near the top of a ~35-year range:

Blue Bird investor presentation, May 2023

Indeed, in 2020, I estimated that mid-cycle EBITDA was probably in the range of $55 million to $70 million, a range roughly in line with FY23 guidance. That estimate, too, suggests very real concerns here about valuation. A mid-teen EV/EBITDA multiple and a high-20s/low-30s P/FCF multiple both appear too high for a highly cyclical business with single-digit Adjusted EBITDA margins and normalized free cash flow margins likely below 5%.

The Market Looks Forward

Of course, investors are supposed to look forward, not backwards. And, at least based on management targets, and tailwinds from Blue Bird’s leadership in propane- and electric-powered buses, there’s still some reason for optimism here.

As the first slide above notes, Blue Bird argues that in a “normal year” the company can generate ~$100 million in EBITDA. That figure suggests roughly a 10x EV/EBITDA multiple – a modest premium to pre-pandemic valuation generally in the 9x range. But with growth expected going forward, the mid-term forecast gets to a range of $150 to $200 million, implying a forward multiple in the 5x-7x range. And the long-term target of $250 million suggests a current ~4x multiple – and huge potential upside.

A 9x-10x EBITDA multiple at the high end would lead BLBD to more than triple, assuming free cash flow generated in the interim not only pays off current debt but builds a cash balance as well. (Conversely, Blue Bird could buy back stock, lowering the share count and increasing the per-share valuation in the future.) $250 million in EBITDA likely suggests at least $150 million in free cash flow, which at a high-teens P/FCF multiple again gets market cap to the $2.5 billion range, and too implies 200%-plus gains in the current BLBD stock price.

Breaking Down The Outlook

The massive divergences between expected earnings, and implied valuations, highlights a very important point here. BLBD is not, at the moment, a stock where an investor can simply build a discounted cash flow model and arrive at a reasonable estimate of current valuation.

DCF models always suffer from a healthy dose of the “garbage in, garbage out” problem. In this case, the multi-year outlook for demand is so important to the model that the model itself is close to useless.

That realization in turn gets to the hugely important question here: is management right? There are essentially three ways in which the mid-term target – which suggests EBITDA growth of 150% to 200%-plus – and the long-term target, which implies that profits will more than quadruple, can be hit:

- The overall market for school buses in North America grows;

- Blue Bird takes share within that market, thanks to alternative-fuel models;

- Those alternative-fuel models are more profitable.

It’s worth thinking through each of those potential drivers (no pun intended) to get a better idea of how far this cyclical upswing can go, and what that might mean for Blue Bird stock.

Market Size

If an investor were going to short BLBD – and it’s not yet a popular trade (short interest is barely 2% of shares outstanding) – one core pillar of the bear case would be the argument that overall demand for school buses isn’t actually likely to grow. The multi-year average for bus registrations, currently cited at 31,000, is essentially equal to the figure (30,623) the company cited nine years ago when it agreed to go public by merging with a special purpose acquisition company.

This isn’t a surprise. The school-age population in the U.S. isn’t growing particularly quickly. Blue Bird itself has noted that the school bus fleet in North America is seeing moderately longer useful lives; net/net, the average amount of new buses needed every year isn’t really changing. Cyclical demand – which in normal times usually is correlated with property tax receipts – may ebb and flow, but it seems highly likely that average annual demand should stay relatively constant.

This problem creates a significant reason for caution. Clearly, both management and the market (BLBD is about 5% below its all-time high) are optimistic toward the growth in electric buses, boosted by aggressive subsidies from the U.S. federal government. But one hugely important thing to remember is that electric vehicle demand isn’t additive to the size of the market; electric buses simply are displacing legacy diesel-powered models.

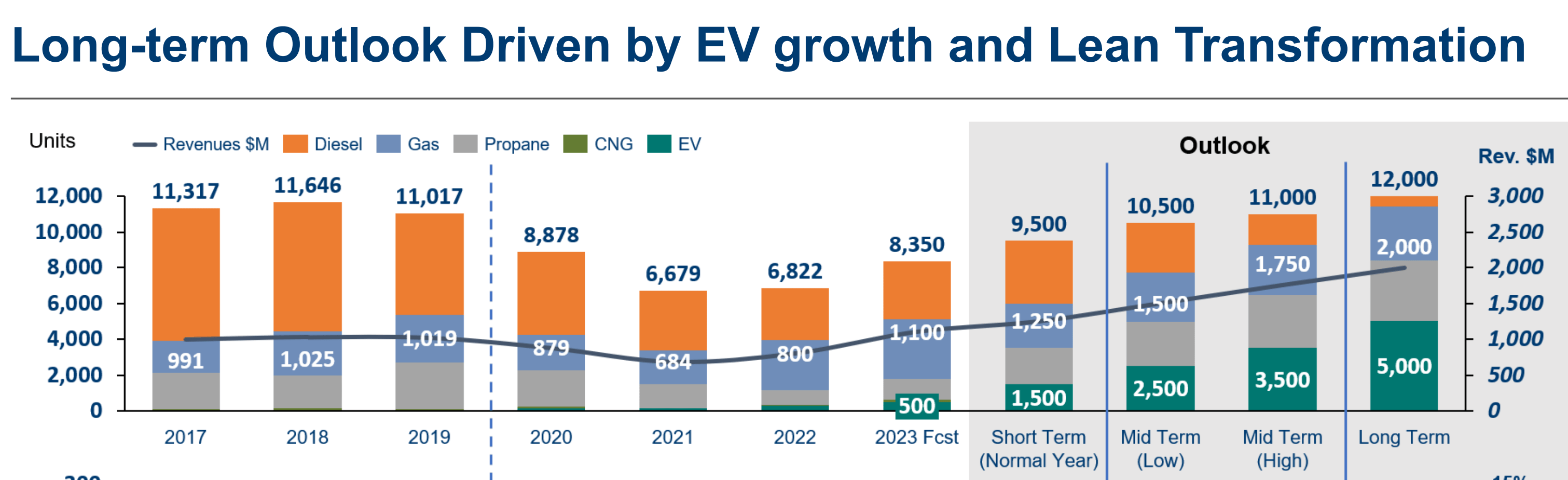

Blue Bird itself agrees. Here’s the top half of the first slide shown above:

Blue Bird investor presentation, May 2023

Blue Bird’s own long-term target of 12,000 vehicles is not terribly higher its 2017-2019 average above 11,000. Again, that figure was at the high end of the cyclical range, and Blue Bird believes it can garner some additional revenue via parts sales and by manufacturing electric-ready chassis for recreational vehicles.

But there’s an interesting contradiction here. Thanks to subsidies, Blue Bird is modeling a sharp increase in demand over the next five years, with unit registrations climbing ~10% annually to nearly 40,000 in 2027.

The question is whether that specific kind of growth will be rewarded by the market. In theory, it shouldn’t be: once subsidies are largely used up and the nationwide fleet renewed (2023-2027 demand is more than one-third of the total existing fleet), growth for the industry and Blue Bird should decline. That in turn suggests that Blue Bird’s profit multiple should shrink in the coming years, ahead of a cyclical peak. Whether the market actually prices BLBD that way, is a source of significant debate.

Market Share

The unit projections from Blue Bird might be considered bullish, however, because they do look potentially conservative. That’s not necessarily true in terms of the market size, but in terms of the market share. The mid-term model, even on the high end, suggests market share closer to 25% than the 30%-plus Blue Bird held from 2017 to 2019.

But there’s not much reason to suggest Blue Bird will lose share. The school bus market overall has essentially a three-and-a-half participants. The legacy ‘Big Three’, for lack of a better term are Blue Bird; IC Bus, which is part of Navistar (now owned by Traton (OTCPK:TRATY)); and Thomas Built Buses, part of Daimler Truck (OTCPK:DTRUY). Lion Electric (LEV), which went public via its own SPAC merger two years ago, has a sliver of the market as well.

Blue Bird has positioned itself as the leader in alternative-powered buses – and that seems to be a factually accurate claim. After Q4 FY22 results, the company said it had more than 850 electric vehicles on the road. IC Bus sold 449 EVs in calendar 2022, according to its annual report, but about 60% of its unit sales are outside the U.S. and Canada. Daimler Truck sold 914 zero-emission vehicles in 2022, but that figure is for the entire business, of which Thomas Built is a small player.

That said, Lion is showing some signs of success. In its Q1 earnings release, Lion said that it had 2,270 electric buses in its order book. That’s not quite the same as backlog: Lion’s order book extends to vehicles projected to be delivered as late as the end of 2026. But for its part, Blue Bird closed its fiscal Q2 (calendar Q1) with “firm order backlog” of over 620 electric vehicles. Again, the two figures aren’t apples to apples, but even if Lion is getting ~600 deliveries a year (as that backlog is worked through over the next 3.5 years), that’s 2% of the overall school bus market, as opposed to simply the electric portion.

If Lion can accelerate its gains, then Blue Bird’s market share might still stay stagnant. That in turn does suggest some upside to the mid-term model: instead of 10.5K-11.0K unit deliveries each year, 30% of a 40K market might get Blue Bird to 12K or higher. That in turn would lead to even higher profit over the next few years – though, again, it’s not clear at what multiple the market will value that profit.

Pricing And Margins

Market size and share factors will play a role. But, overall, the bull case for BLBD stock likely comes down to how profitably it can manufacture its buses. The 100%-plus profit growth Blue Bird itself is modeling relative to the late 2010s average is based on not on unit growth, but increases in profit per unit.

The company expects a rather stunning increase. From 2017 to 2019, Blue Bird’s average price was about $89,000; its average Adjusted EBITDA per bus was about $6,500. The midpoint of the mid-term model range suggests pricing of roughly $150,000, and Adjusted EBITDA per unit of more than $16,000.

The latter metric seems the most important: Blue Bird, in a few years, expects to make 150% more profit on each bus as it did in the last three years of the 2010s. And, again, those three years were relatively strong from a cyclical perspective.

Both the shift to EVs and government subsidies will help, but nearly 60% of the current mix already is alternative-fuel (mostly propane). Input costs are higher. Higher-margin parts revenue may come down given a newer fleet and less-complicated electrified engines.

To be clear, it’s possible Blue Bird indeed posts the per-unit profit expansion it projects. But management targets can’t be trusted blindly. And in an environment with uncertainty around demand, the health of property tax receipts, and competition (possibly on price), that’s all the more true.

BLBD Stock Is Attractive, But Not Compelling

And in that context, the rally from last year’s lows seems like it has incorporated most of the value here. There’s certainly the potential for more gains here, and if Blue Bird hits that out-year target, again, the stock easily can double in a few years. That’s true even if multiples compress as subsidies and EV growth drive overall market growth; it’s obviously more true if, as is possible, those multiples don’t compress.

But a high-single-digit multiple to FY25 EBITDA – even assuming very strong growth the next two years – isn’t terribly attractive from a valuation standpoint. And there are things that can go wrong along the way, even with such substantial support coming from the federal government over the next few years.

That’s particularly true given how reliant the upside is on pricing strength and margin expansion – for a business that historically has generated EBITDA margins well below 10%, and is only guiding for ~5-6% this year. Blue Bird will need to do much better on that front going forward. It’s easier said than done.