Align Technology Overvalued But A Noteworthy Addition To Watchlist (NASDAQ:ALGN)

Olga Demina/iStock via Getty Images

Introduction

Align Technology (NASDAQ:ALGN), a leading U.S. medical device company specializing in orthodontics, is making waves in the industry with its diverse portfolio of products including Invisalign clear aligners, iTero intraoral scanners, and exocad dentistry-dedicated software. In this financial analysis, we will assess why Align Technology’s stock may be considered overvalued and why it remains a noteworthy addition to investors’ watchlists in anticipation of a potential price correction.

Business Model

Align’s business model is divided into two segments: the Clear Aligner line, accounting for 82% of total revenues, and the Imaging System and CAD/CAM Services line, that account for the remaining 18% of total revenues.

The Clear Aligner segment is dedicated to curing malocclusion problems using the Invisalign system, a proprietary technology developed by Align Technology. Invisalign is a brand of clear aligners that differ from traditional braces.

As the name suggests, the best advantage of clear aligners over traditional braces is that they are practically invisible as they are made with plastic polymers and perfectly adapt to the teeth of patients. Overall comfort and hygiene are highly improved when using clear aligners rather than traditional braces.

Another important advantage of clear aligners is that they usually require less time to solve malocclusion problems, however, they may not be super effective with severe malocclusions, whereas traditional braces still result to be more effective.

But an important factor on which we should dwell is the difference in prices of the two solutions, despite having more advantages, Invisalign solutions are not more expensive than traditional braces, they actually have similar prices. Is easy to infer then, that the potential for wide adoption of clear aligners over traditional braces is very likely to happen in the coming years.

Looking at the Imaging System and CAD/CAM Services segment, here Align develops and manufactures intraoral scanners, under the iTero brand, used by dentists to get highly precise digital mouth scans needed to implement Invisalign solutions to cure malocclusions, and a full set of dedicated software that help dentists in their day-to-day operations.

Growth Drivers

Align Technology is a pioneer of the clear aligner industry, beginning its operation more than 25 years ago, and today they certainly have a dominant position in this relatively young and growing industry with 14 million patients that benefited from its solution.

But being the first to arrive is not enough to keep succeeding. Align’s business model and long-term performance are heavily dependent on the investments made in R&D to keep improving and expanding its offers of clear aligners, ancillary services, and products.

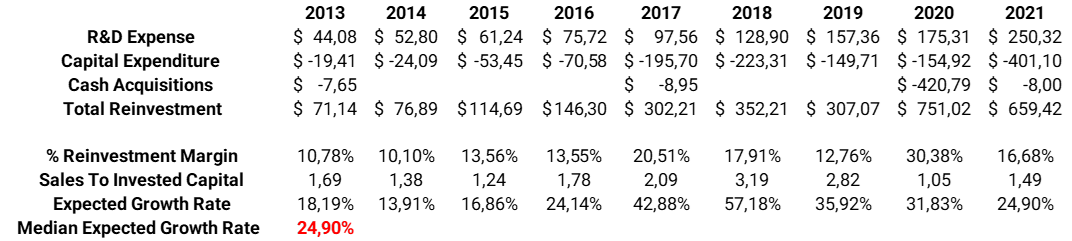

To calculate the expected growth rate for Align’s revenues we can use the investments made in R&D as its main growth driver, followed by capital expenditures needed to keep the manufacturing plants working efficiently, considering that they internally manufacture every clear aligner they sell to dentists. Last but not least, we can consider also acquisitions that are basically, R&D and CapEx on a larger scale.

Knowing how much Align has invested in its growth drivers in the past years, thanks to the reinvestment margin, and knowing how well they invested in the past years, thanks to the sales-to-invested capital ratio, we obtain a median expected growth rate of 24.9% at which we can let the revenues growth when projecting Align’s future performance.

Align Technology’s expected growth rate (Personal Data)

Operating Performance

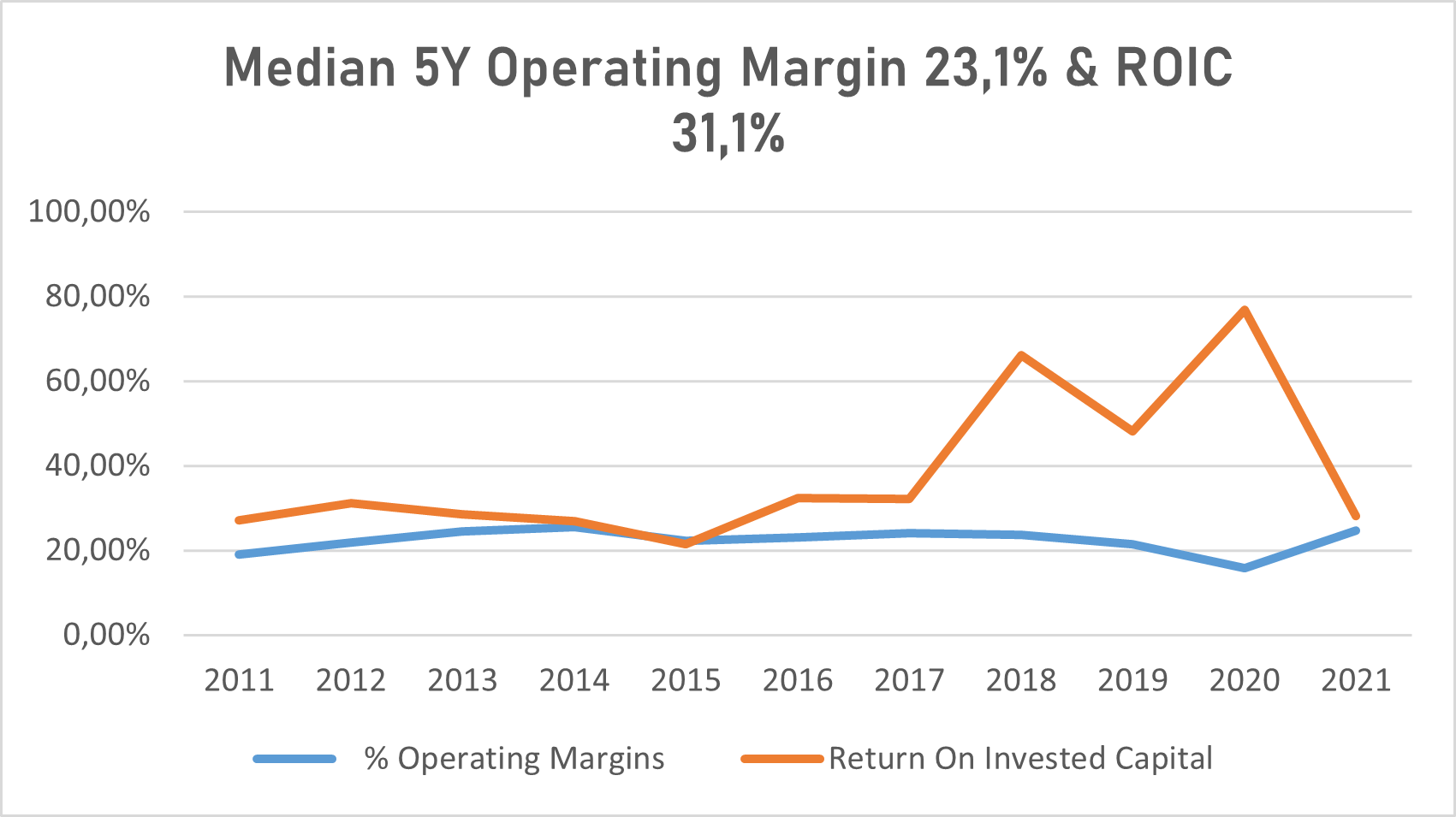

Looking at Align’s past operating performance its business model proved to be highly successful both in terms of growth and profitability. From 2011 to 2021 revenues increased at a CAGR of 23.48% from $479 million in 2011 to $3.9 billion in 2021.

The median operating margin over the ten-year period is 23% while the median return on invested capital (ROIC) is 31%. Double digits growth rate, high efficiency and high profitability translated into a strong cash flow generation with free cash flows to the firm (FCFF) that went from negative -$102 million in 2011 to a solid $598 million in 2021.

Align Technology’s median 5Y operating margin & ROIC (TIKR Terminal)

Regarding 2022, Align published its third-quarter results, and the year’s performances are far from those of the past years. In a deadly mix of unfavourable foreign currency exchange rates and macroeconomic uncertainty, revenues declined more than 12% year over year, of which 6% is due to a stronger dollar that badly affected the conversion of revenues in foreign currency that account for 66% of total sales.

Looking at the past nine months, revenues declined 4% from $2.92 billion in 2021 to $2.83 billion in 2022. The operating income declined 30% year-over-year and badly affected both the operating margin, which declined to 18% from 25% and the ROIC, which declined to 12.76% from 24% compared to last year.

Financially speaking, Align Technology is very stable with a net cash position of $948 million in the most recent quarter, a current ratio of 1.3 and a debt-to-equity ratio of 0.03.

Industry Risk

The market in which Align operates is far from being saturated and among the 500 million estimated potential customers all over the world, the teenage segment represents the best growth opportunity in the coming years. Among the 14 million patients cured by Invisalign so far, only 3.5 million were teens but as reported by the company itself, teenagers represent 75% of the approximately 21 million global cases of malocclusion cured each year, of which 5 million are only in the US.

Align is allocating part of its marketing resources, like special purchase programs for dentists and targeted advertising via the main social media, trying to capitalize on this big chunk of the market left behind.

Projections

I use the discounted cash flow analysis method to value companies. The aim of a DCF analysis is to determine the present value of expected cash flows generated by the company in the future. The first step is to project the growth rate at which revenues will grow in the future. Secondly, we will need to assume the degree of efficiency and profitability at which the company will turn revenues into cash flows.

Efficiency is represented by the operating margin, and profitability by the ROIC. Having the revenue projections and future operating margins, we obtain the EBIT and, after subtracting taxes, we get the net operating profit after taxes. The ROIC is used to determine the reinvestments needed to support future growth, determining how much profit the company generates from every dollar reinvested into the company. Future cash flows are calculated by subtracting the reinvestments from the net operating profit after taxes. The higher the growth rate, the higher the reinvestments needed to support it, hence the lower future cash flows will be.

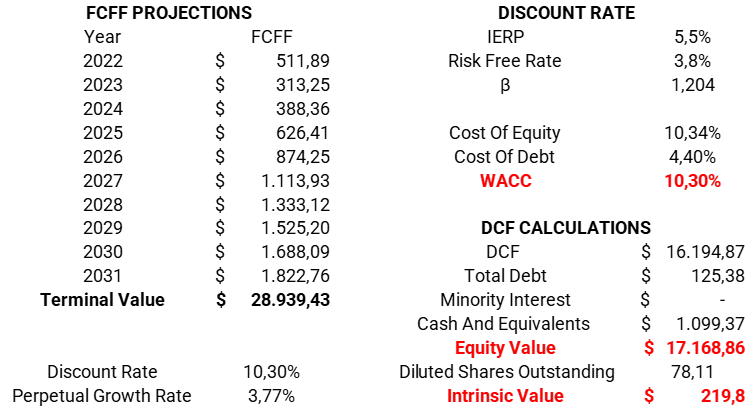

The last step of a DCF analysis is to apply the discount rate to future cash flows, usually calculated using the weighted average cost of capital (WACC).

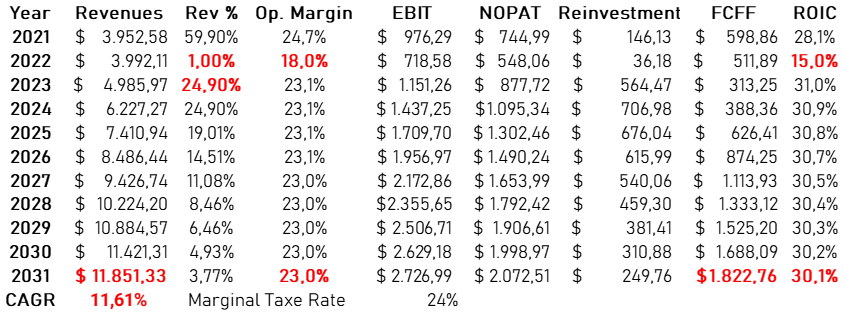

Trying to project Align’s future performance, as regards the end of 2022, looking at what happened so far we can expect revenues to barely grow this year (around 1%), while as regards the operating margin and the ROIC we can expect them to be around 18% and 15% respectively.

In 2023, assuming the macroeconomic uncertainty will slowly disappear we can expect Align to go back to its usual performance. For the revenue growth rate, we can use the expected growth rate of 24.9% that we calculate before and that is based on how much and how well the company has reinvested in its growth drivers.

After 2023, as the company approaches maturity, we can expect revenue growth to start to slow down until reaching the growth rate of the economy in a steady state. So, we can expect revenues to be around $12 billion by 2031, growing at a CAGR of 11.6%.

Moving on to efficiency and profitability we can expect Align to recover both its operating margin and ROIC to their median values, respectively of 23% and 30%, assuming Align will be able to maintain its leading position in the future. With these assumptions we ended up with FCFF expected to be around $1.8 billion by 2031, growing at a CAGR of 11.8%.

Align Technology’s performance projection (Personal Data)

Intrinsic Value

Applying a discount rate of 10.30% calculated using the WACC, we obtain the present value of these cash flows equal to $17.1 billion, which divided by the number of shares outstanding is equal to a share price of $220.

Align Technology’s intrinsic value (Personal Data)

Conclusion

If compared to today’s prices, in my opinion, Align seems to be slightly overvalued. Despite all the macroeconomic issues that Align technology is facing in the short term, its business model is still strong and certainly able to replicate the great performance of the past in the coming years. The market of clear aligners is far from maturity and there is still a lot of room for Align to grow. With all of our assumptions, while Align Technology’s stock is overvalued, it remains a company worth to be held for the long run and a noteworthy addition to investors’ watchlists in anticipation of a potential price correction.